Tax Demand

Apeejay Surrendra Park Hotels Receives Income Tax Assessment Order of ₹41.07 Crore; Plans to File Appeal

NSE

parkhotels

BSE

544111

Apeejay Surrendra Park Hotels Limited has received an Income Tax Assessment Order from the Income Tax Department relating to Assessment Year (AY) 2024-25, resulting in a tax demand of ₹41.07 crore, including applicable interest. The company intends to challenge the order before the appellate authority and believes the matter is legally sustainable without any material financial or operational impact.

PRICE-SENSITIVE TRIGGER

Event: Receipt of Income Tax Assessment Order from the Income Tax Department.

Type: Tax Demand / Regulatory Order

Impact: Neutral

Immediate Effect: The company has received a tax demand of ₹41.07 crore and is initiating appellate proceedings before the appropriate tax authority.

Key Metrics:

- Tax Demand: ₹41,06,72,530 (including applicable interest)

Highlight:

- The disclosure relates to a tax assessment order and does not contain operational or quarterly financial performance data.

- The company has stated that it does not expect any material financial, operational, or business impact from the order.

What Happened ?

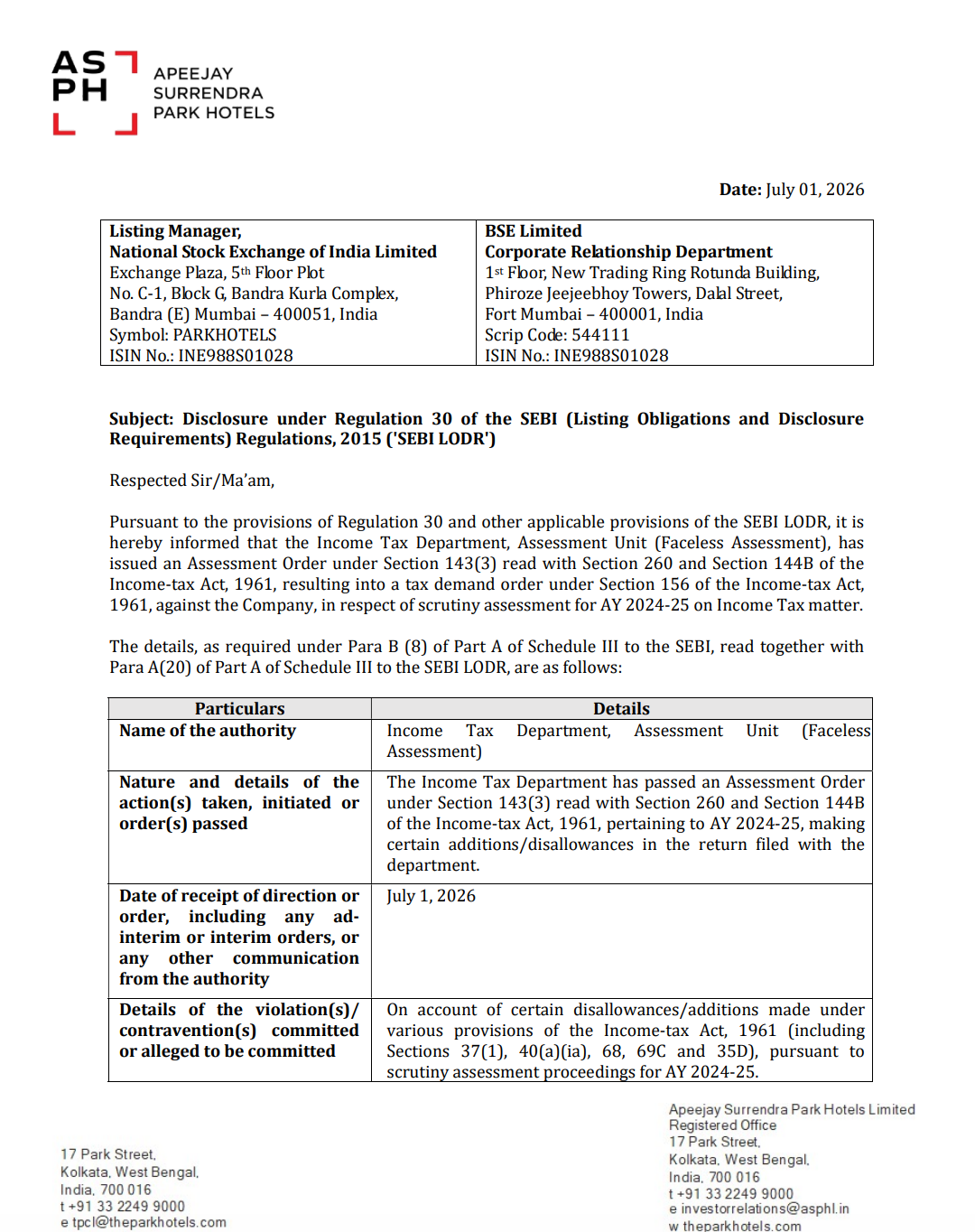

Apeejay Surrendra Park Hotels Limited informed the stock exchanges that it has received an Assessment Order from the Income Tax Department, Assessment Unit (Faceless Assessment) under Sections 143(3) read with Sections 260 and 144B of the Income-tax Act, 1961.

The order pertains to the scrutiny assessment for Assessment Year 2024-25, resulting in a tax demand under Section 156amounting to ₹41.07 crore, including applicable interest.

The company has decided to file an appeal before the appropriate Appellate Forum/National Faceless Appeal Centre (NFAC) within the prescribed timelines.

Key Details

Assessment Order:

- Authority: Income Tax Department, Assessment Unit (Faceless Assessment)

- Assessment Year: AY 2024-25

- Date of Receipt: 1 July 2026

- Order issued under:

- Section 143(3)

- Read with Sections 260 and 144B

- Tax demand raised under Section 156 of the Income-tax Act, 1961

Note:

- The assessment order arose from scrutiny proceedings conducted for AY 2024-25.

Nature of Demand:

- Tax demand raised: ₹41,06,72,530, including applicable interest.

- The order relates to additions/disallowances made during scrutiny assessment.

- The alleged issues involve provisions including:

- Section 37(1)

- Section 40(a)(ia)

- Section 68

- Section 69C

- Section 35D

Note:

- The company has not accepted the assessment findings and intends to pursue legal remedies.

Company Response:

- Appeal will be filed before the appropriate Appellate Forum/National Faceless Appeal Centre (NFAC).

- Management believes it has adequate factual and legal grounds to defend its position.

- The company expects a substantial portion of the demand may not survive during appellate proceedings.

Note:

- The company has stated that further developments will be disclosed in accordance with SEBI Listing Regulations.

Business Impact:

- Management does not expect the assessment order to materially affect:

- Financial performance

- Business operations

- Other operating activities

Note:

- The disclosure indicates that the matter is currently under legal challenge and no operational disruption is anticipated.

Risk Analysis

Summary:

- Although the tax demand is sizeable, the final financial impact remains subject to appellate proceedings. The outcome will depend on judicial review of the disputed tax adjustments.

Key Risks:

- Appeal outcome remains uncertain.

- Potential cash outflow depends on final adjudication.

- Litigation timelines could extend over multiple years.

- Regulatory compliance and disclosure obligations continue until final resolution.

Worst Case:

- If appellate authorities uphold the assessment in full, the company may be required to settle the tax demand together with any additional statutory interest, impacting cash flows.

Risk Level: Medium

Company Commentary

- The company has received a tax assessment order for AY 2024-25.

- Total demand amounts to ₹41.07 crore, including applicable interest.

- Appeal will be filed before the appropriate appellate authority/NFAC.

- Management believes the company has strong legal and factual grounds.

- No material financial, operational or business impact is currently expected.

Official Exchange Filing: Apeejay Surrendra Park Hotels Limited