Credit Rating Update

Persistent Systems Credit Rating Placed on Rating Watch with Negative Implications by ICRA

NSE

persistent

BSE

533179

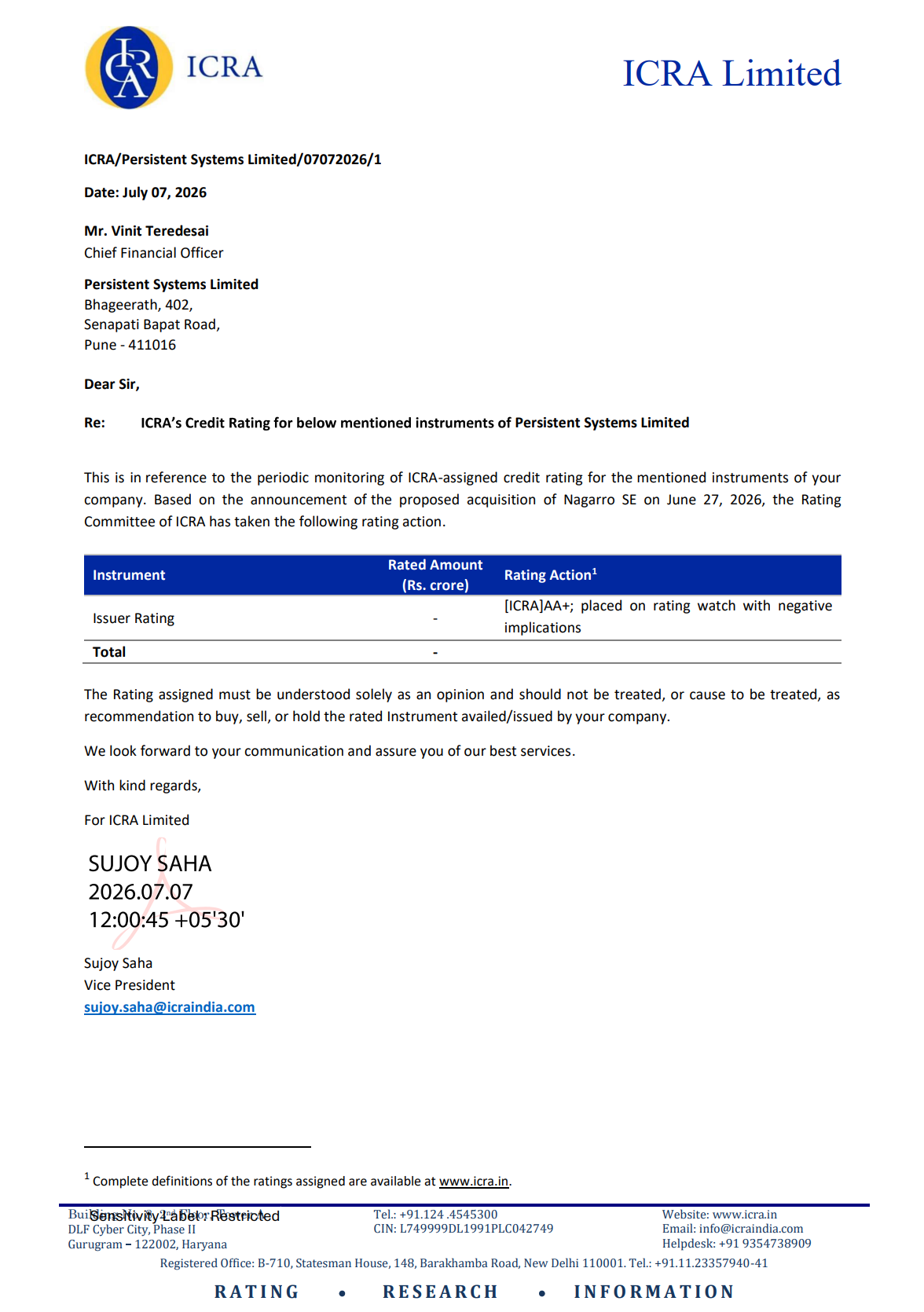

Persistent Systems Limited announced that ICRA Limited has revised its issuer credit rating outlook by placing the existing [ICRA] AA+ rating on Rating Watch with Negative Implications. The revision follows Persistent’s proposed acquisition of Nagarro SE, with ICRA highlighting uncertainties regarding the final acquisition structure, leverage profile, debt funding, and integration process.

PRICE-SENSITIVE TRIGGER

Event: Revision in issuer credit rating by ICRA.

Type: Credit Rating Update

Impact: Negative

Immediate Effect: ICRA has retained the company’s [ICRA] AA+ issuer rating while placing it on Rating Watch with Negative Implications, pending greater clarity on the proposed acquisition of Nagarro SE, funding structure, leverage levels and post-acquisition financial profile.

Financials:

Financial Metrics (FY2026 – Consolidated):

- Revenue: ₹14,748.4 crore (vs ₹11,938.7 crore in FY2025 | +23.5% YoY)

- EBITDA Margin (OPBDIT/OI): 19.0% (vs 16.0% in FY2025 | +300 bps YoY)

- PAT: ₹1,865.1 crore (vs ₹1,400.2 crore in FY2025 | +33.2% YoY)

- PAT Margin: 12.6% (vs 11.7% in FY2025 | +90 bps YoY)

- QoQ Movement: Not disclosed

- YoY Movement:

- Revenue: +23.5%

- PAT: +33.2%

- EBITDA Margin: +300 bps

- Segment Performance: Not separately disclosed.

Rating Action:

- Previous Rating: [ICRA] AA+ (Stable)

- Current Rating: [ICRA] AA+

- Current Outlook: Rating Watch with Negative Implications

- Rating Agency: ICRA Limited

Highlight:

- Although Persistent continues to report strong operating performance and healthy profitability, ICRA has placed the rating on watch due to the expected increase in leverage arising from the debt-funded acquisition of Nagarro SE rather than deterioration in the company’s current operations.

What Happened ?

Persistent Systems informed the exchanges that ICRA has revised its issuer rating outlook after reviewing the company’s proposed acquisition of Germany-based Nagarro SE, announced on June 27, 2026.

The proposed transaction involves the acquisition of a 21% stake through a share purchase agreement and an open offer to acquire a controlling stake, with an eventual objective of reaching 100% ownership, subject to regulatory approvals and minimum acceptance conditions.

ICRA stated that while the acquisition has the potential to materially strengthen Persistent’s business profile, the transaction’s debt-funded nature creates uncertainty regarding leverage, refinancing requirements and future credit metrics. Consequently, the existing AA+ rating has been placed on Rating Watch with Negative Implications until greater clarity emerges on the transaction and its financing.

Key Details

Proposed Acquisition:

- Acquisition target: Nagarro SE, Germany.

- Initial acquisition of 21% stake through a share purchase agreement.

- Open offer priced at EUR 81 per share.

- Target ownership: 100%, subject to regulatory approvals.

- Enterprise valuation implied at approximately EUR 1.27 billion.

- Expected completion: Q4 CY2026 / Q1 CY2027.

Business Impact:

- Combined annual revenue expected to be approximately USD 2.9 billion.

- Employee base expected to increase from over 27,500 to more than 46,000.

- Geographic presence expected to expand from 21 countries to over 40 countries.

- Europe revenue contribution expected to increase from 9% to 22%.

- North America revenue contribution expected to moderate from 81% to 62%.

- Enhanced capabilities in:

- Artificial Intelligence

- Digital Engineering

- Enterprise Resource Planning

- Broader industry diversification including Industrials, Consumer and Public Sector.

Strategic Importance:

ICRA noted that the acquisition significantly enhances Persistent’s strategic scale and geographic diversification. However, because the transaction is proposed to be financed entirely through debt, it is expected to materially increase consolidated leverage and weaken the company’s financial risk profile over the medium term.

The agency stated that the final rating action will depend on:

- Final acquisition structure.

- Debt funding arrangements.

- Integration progress.

- Post-acquisition leverage levels.

- Pace of deleveraging.

Note:

- The rating action reflects uncertainty around the acquisition’s financing and leverage rather than any deterioration in Persistent Systems’ current operating performance.

Risk Analysis

Summary:

- The principal risk arises from the sizeable debt-funded acquisition, which is expected to increase leverage materially and introduce refinancing and integration risks despite the strategic benefits of the transaction.

Key Risks:

- Higher consolidated debt following acquisition.

- Leverage expected to increase materially post transaction.

- Refinancing risk associated with bridge financing.

- Integration execution risk.

- Delay in deleveraging could pressure future credit ratings.

- Transaction remains subject to regulatory approvals and completion conditions.

Worst Case:

- If Persistent completes the acquisition with higher-than-expected leverage or experiences slower integration and deleveraging, ICRA could downgrade the issuer rating after completing its review.

Risk Level: Medium to High

Company Commentary

- Persistent Systems informed investors that ICRA revised the rating outlook in view of the proposed acquisition of Nagarro SE and attached the complete rating rationale received from the agency.

- The company continues to maintain its existing [ICRA] AA+ issuer rating while the acquisition progresses through regulatory approvals and transaction completion.

Official Exchange Filing: Persistent Systems Limited