Credit Rating Upgrade

JSW Steel Credit Rating Upgraded to CARE AA+ Stable; Stronger Balance Sheet Supports Long-Term Growth

NSE

jswsteel

BSE

500228

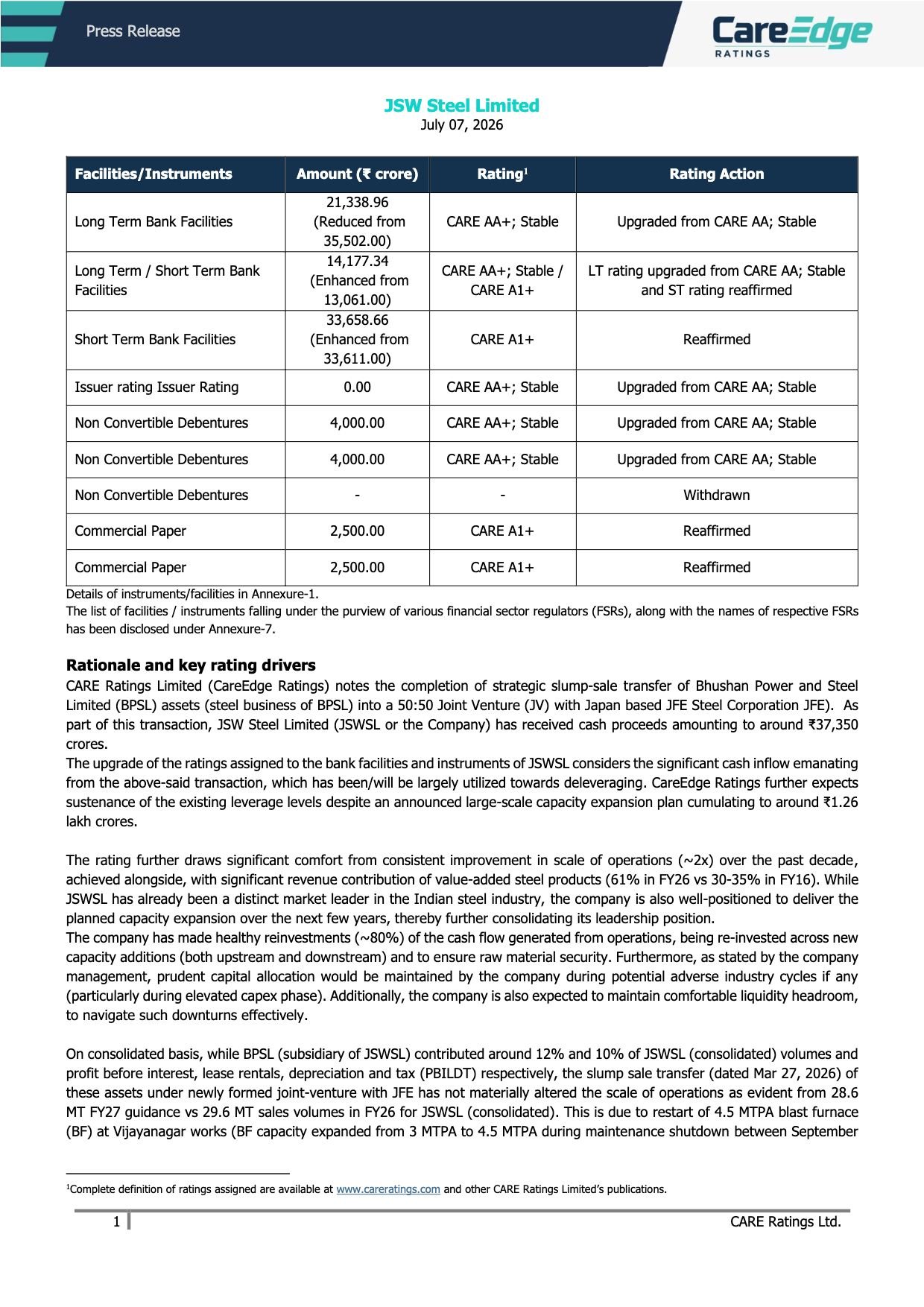

JSW Steel has received an upgrade in its long-term credit ratings from CARE AA (Stable) to CARE AA+ (Stable), while its short-term CARE A1+ ratings have been reaffirmed. The rating agency cited significant deleveraging following the Bhushan Power & Steel (BPSL) transaction, stronger leverage metrics, healthy liquidity, sustained operating performance, and confidence in the company’s ability to execute its long-term expansion plans without materially weakening its financial profile.

PRICE-SENSITIVE TRIGGER

Event: CARE Ratings upgrades JSW Steel’s long-term credit rating.

Type: Credit Rating Upgrade

Impact: Positive

Immediate Effect: The upgrade strengthens JSW Steel’s credit profile across long-term bank facilities, issuer rating, non-convertible debentures, and other long-term borrowings while reaffirming its highest short-term rating (CARE A1+). A stronger credit rating can improve borrowing flexibility and lower financing costs over time.

Financials:

- Revenue: ₹1,85,470 crore (vs ₹1,68,754 crore in FY25)

- EBITDA (PBILDT): ₹29,821 crore (vs ₹22,966 crore)

- PAT: ₹25,508 crore (vs ₹3,491 crore)

- Overall Gearing: Improved to 1.16x from 1.51x

- Interest Coverage: Improved to 3.28x from 2.73x

- Net Debt / PBILDT: Improved to 2.60x from 4.38x

Highlight:

- Significant improvement in leverage and profitability supported CARE’s upgrade to AA+ Stable.

What Happened ?

CARE Ratings upgraded multiple long-term credit facilities of JSW Steel from CARE AA (Stable) to CARE AA+ (Stable) while reaffirming the company’s CARE A1+ short-term ratings.

The upgrade follows the successful completion of the strategic transfer of Bhushan Power & Steel Limited’s steel assets into a 50:50 joint venture with Japan’s JFE Steel Corporation. The transaction generated approximately ₹37,350 crore in cash proceeds, enabling substantial deleveraging of the balance sheet.

CARE believes the company’s improved financial flexibility, stronger operating performance, disciplined capital allocation, and healthy liquidity provide sufficient headroom to execute its planned ₹1.26 lakh crore expansion programme while maintaining comfortable leverage levels.

Key Details

Rating Upgrade Rationale:

- CARE upgraded Long-Term Bank Facilities to CARE AA+ Stable.

- Issuer Rating upgraded to CARE AA+ Stable.

- Non-Convertible Debentures upgraded to CARE AA+ Stable.

- Commercial Paper ratings reaffirmed at CARE A1+.

- Long-term/Short-term combined facilities upgraded to CARE AA+ Stable / CARE A1+.

Business Strengths Supporting the Upgrade:

- Around ₹37,350 crore received from the BPSL transaction significantly strengthened liquidity.

- Net leverage reduced materially following debt repayment.

- Domestic steel capacity continues to expand with multiple projects under execution.

- Value-added steel products contributed approximately 61% of FY26 revenue mix, supporting margin resilience.

- CARE expects domestic steel demand to grow at 7–8% CAGR over the next few years, supporting capacity utilisation.

- Strong liquidity provides flexibility during the company’s ongoing expansion cycle.

Operational Highlights:

- Consolidated sales volume increased from 26.45 MT to 29.58 MT in FY26.

- PBILDT per tonne improved to ₹10,081 from ₹8,683.

- Restart of expanded Vijayanagar blast furnace supports FY27 production.

- Additional growth expected through Dolvi expansion, Odisha project and BMM Ispat integration.

Investor Relevance:

- A higher credit rating enhances lender confidence and reflects improved financial stability. The stronger balance sheet also provides greater flexibility to fund future capital expenditure while preserving financial discipline, an important consideration given the company’s large expansion pipeline.

Risk Analysis

Summary:

- Despite the rating upgrade, CARE highlights that JSW Steel continues to operate in a cyclical industry with sizeable future capital commitments.

Risk Points:

- Planned capital expenditure of approximately ₹1.26 lakh crore over the next 4–5 years.

- Exposure to cyclical steel prices and global demand conditions.

- Foreign exchange risk due to imported coking coal and foreign currency borrowings.

- Commodity price volatility.

- Execution risks associated with large expansion projects.

- Regulatory uncertainty relating to mining taxation.

Worst Case:

- Any significant deterioration in leverage due to debt-funded expansion, project execution delays, weaker cash generation, or adverse industry conditions could put pressure on future credit metrics and ratings.

Risk Level: Medium

Company Commentary

CARE Ratings highlighted the following key strengths behind the upgrade:

- Significant deleveraging following the BPSL transaction.

- Improved profitability and stronger cash generation.

- Comfortable liquidity position.

- Market leadership in the Indian steel industry.

- Confidence that future expansion can be funded while maintaining healthy leverage.

- Stable outlook reflecting expectations of sustained operating performance and continued industry leadership.

Official Exchange Filing: JSW Steel Limited