Quarterly Earnings

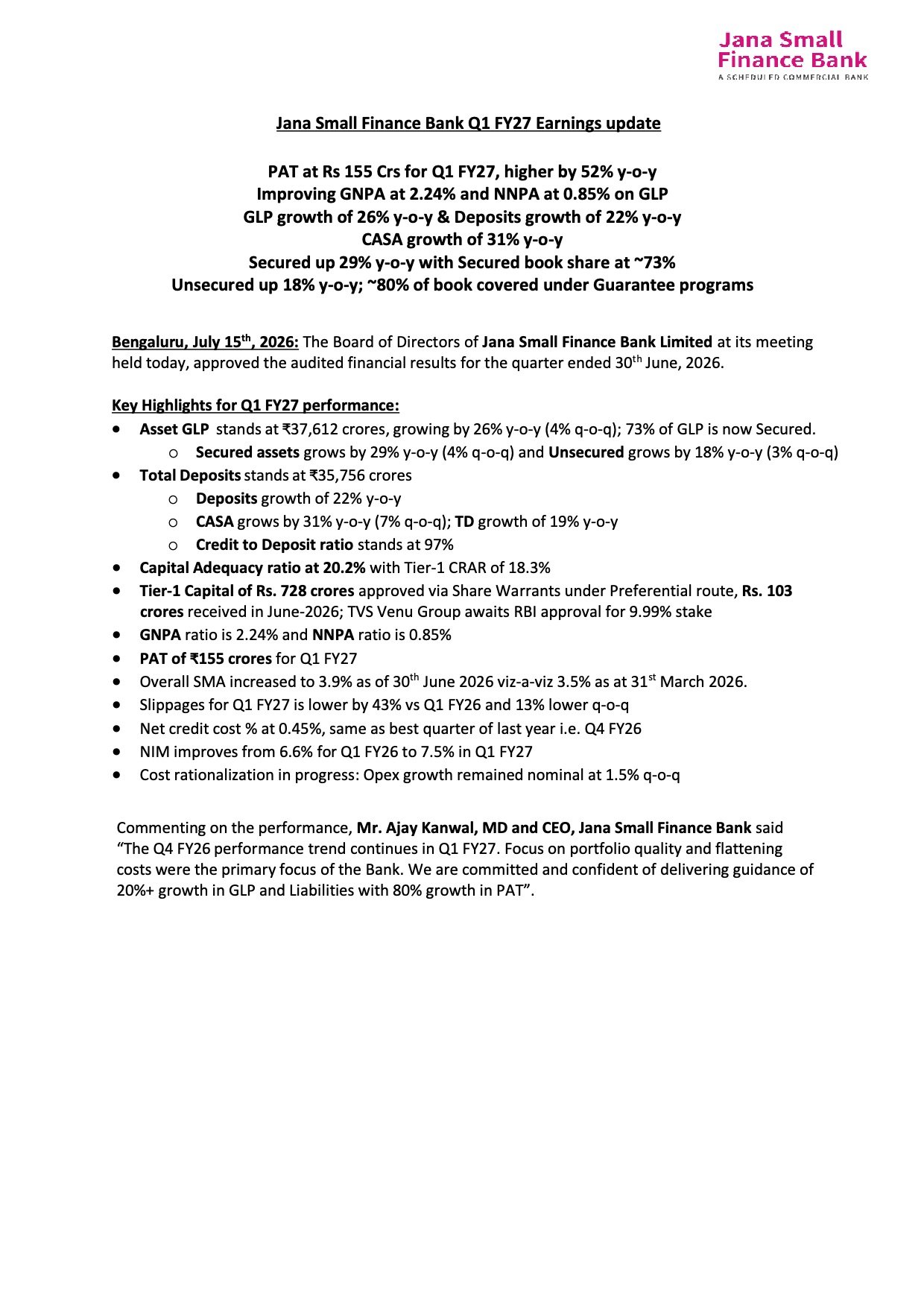

Jana Small Finance Bank Reports 52% YoY Growth in Q1 FY27 PAT to ₹155 Crore

NSE

jsfb

BSE

544118

Jana Small Finance Bank reported a strong Q1 FY27 performance with Profit After Tax (PAT) rising 52% year-on-year to ₹155 crore. The bank continued to improve its asset quality, expanded its secured loan portfolio, maintained healthy deposit growth, and witnessed higher Net Interest Margin (NIM), reflecting improving profitability and operational stability.

PRICE-SENSITIVE TRIGGER

Event: Q1 FY27 Financial Results Announcement

Type: Quarterly Earnings

Impact: Positive

Immediate Effect:

- The bank delivered robust earnings growth supported by higher lending, improved asset quality, stronger deposits, expanding secured loan mix, and improved margins while reiterating its growth guidance for FY27.

Financials:

Key Metrics:

- Interest Income: ₹1,515 crore (+22.1% YoY, +4.8% QoQ)

- Net Interest Income (NII): ₹782 crore (+33.4% YoY, +6.3% QoQ)

- Operating Income: ₹1,009 crore (+18.4% YoY, +0.8% QoQ)

- Operating Margin: ₹333 crore (+15.2% YoY, marginally lower QoQ)

- Profit Before Tax: ₹155 crore (+52% YoY, +10.7% QoQ)

- Profit After Tax (PAT): ₹155 crore (+52% YoY, +10.7% QoQ)

- Net Interest Margin (NIM): 7.5% (vs 6.6% YoY; 7.2% QoQ)

- Cost-to-Income Ratio: 67.0%

- Return on Assets (RoA): 1.4%

- Return on Equity (RoE): 13.6%

- Capital Adequacy Ratio: 20.2%

- Gross NPA: 2.24%

- Net NPA: 0.85%

- Gross Loan Portfolio (GLP): ₹37,612 crore (+26% YoY, +4% QoQ)

- Total Deposits: ₹35,756 crore (+22% YoY)

- CASA Deposits: +31% YoY, CASA ratio improved to 19.2%.

- Secured Loan Portfolio: Approximately 73% of GLP, growing 29% YoY.

- Unsecured Portfolio: Grew 18% YoY with nearly 80% covered under guarantee programmes.

Highlight:

- PAT increased 52% YoY to ₹155 crore while GNPA improved to 2.24% and NIM expanded to 7.5%, indicating stronger profitability alongside improving asset quality.

What Happened ?

Jana Small Finance Bank announced its financial results for the quarter ended 30 June 2026, reporting broad-based improvement across profitability, lending, deposits and asset quality.

The bank expanded its Gross Loan Portfolio by 26% year-on-year while maintaining a strategic shift toward secured lending, which now constitutes nearly three-fourths of the overall portfolio. Deposit mobilisation remained healthy with strong CASA growth, supporting funding stability.

Profitability improved through higher Net Interest Income and expanding Net Interest Margin, while lower slippages and stable credit costs reflected continued focus on portfolio quality.

key details

Business Growth:

- Gross Loan Portfolio reached ₹37,612 crore, growing 26% YoY.

- Secured assets increased 29% YoY and now contribute approximately 73% of the loan book.

- Unsecured assets grew 18% YoY with significant guarantee coverage.

- Credit-to-Deposit ratio remained healthy at 97%.

Deposit Franchise:

- Total deposits increased to ₹35,756 crore, registering 22% YoY growth.

- CASA deposits grew 31% YoY.

- Term deposits recorded 19% YoY growth.

- CASA ratio improved to 19.2%, strengthening the bank’s low-cost funding base.

Asset Quality:

- Gross NPA improved to 2.24%.

- Net NPA declined to 0.85%.

- Slippages reduced 43% compared with Q1 FY26 and 13% sequentially.

- Net credit cost remained at 0.45%, matching the best quarterly performance achieved in Q4 FY26.

- SMA stood at 3.9% compared with 3.5% in the previous quarter, indicating a slight increase in early stress accounts.

Capital Position:

- Capital Adequacy Ratio remained strong at 20.2%.

- Tier-I Capital Ratio stood at 18.3%.

- The Board approved ₹728 crore Tier-I capital through preferential share warrants.

- ₹103 crore was received during June 2026, while investment by TVS Venu Group remains subject to RBI approval.

Operating Performance:

- Net Interest Margin improved to 7.5% from 6.6% in Q1 FY26.

- Operating expenses increased only 1.5% QoQ due to ongoing cost rationalisation.

- Operating income crossed ₹1,000 crore for the quarter, supported by stronger lending activity and higher interest income.

Risk Analysis

Summary:

- The overall earnings profile remains strong; however, investors should continue monitoring asset quality indicators, capital deployment and regulatory approvals related to the proposed equity infusion.

Key Risks:

- SMA ratio increased from 3.5% to 3.9%.

- Capital infusion from TVS Venu Group remains subject to RBI approval.

- Maintaining asset quality while sustaining rapid loan growth will remain important.

- Banking sector profitability remains sensitive to credit costs and interest-rate movements.

Worst Case:

- If early-stage stressed assets translate into higher NPAs or capital infusion is delayed, profitability and future growth momentum could moderate.

Risk Level: Medium

Company Commentary

Managing Director & CEO Ajay Kanwal stated that the positive operating trend witnessed during Q4 FY26 continued into Q1 FY27, with portfolio quality improvement and cost discipline remaining the bank’s primary focus.

Management reaffirmed its confidence in achieving:

- More than 20% growth in Gross Loan Portfolio.

- More than 20% growth in liabilities.

- Approximately 80% growth in PAT for FY27.

Official Exchange Filing: Jana Small Finance Bank Limited