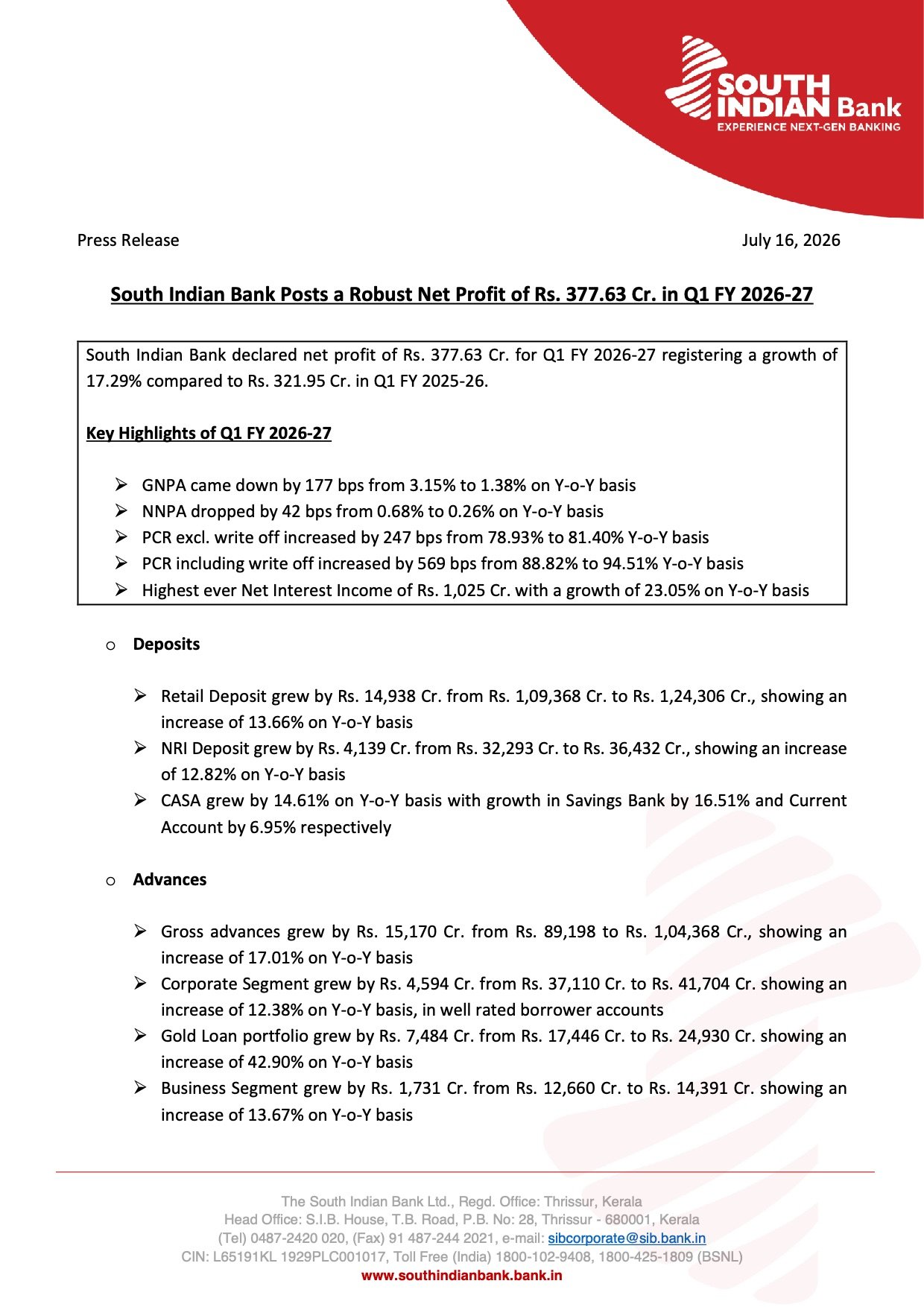

Quarterly Financial Results

South Indian Bank Q1 FY27 Net Profit Rises 17% to ₹377.63 Crore; Asset Quality Improves Sharply

NSE

southbank

BSE

532218

South Indian Bank reported a strong performance for Q1 FY2026-27, with net profit increasing 17.29% YoY to ₹377.63 crore. The bank achieved its highest-ever quarterly Net Interest Income (NII) of ₹1,025 crore, while asset quality improved significantly as Gross NPA declined to 1.38% and Net NPA to 0.26%. Strong growth in advances, retail deposits, CASA, and gold loans supported the quarter’s performance.

PRICE-SENSITIVE TRIGGER

Event: South Indian Bank announced its unaudited financial results for the quarter ended June 30, 2026.

Type: Quarterly Financial Results

Impact: Positive

Immediate Effect: The bank delivered double-digit growth in profitability, strengthened asset quality, achieved record Net Interest Income, and continued healthy expansion across its loan and deposit portfolio.

metrics:

- Net Profit: ₹377.63 crore (+17.29% YoY)

- Profit Before Tax: ₹507 crore (+17.09% YoY)

- Net Interest Income (NII): ₹1,025 crore (+23.05% YoY) (Highest Ever)

- Operating Profit: ₹592 crore (-11.90% YoY)

- Other Income: ₹379 crore (-39.07% YoY)

- Gross Advances: ₹1,04,368 crore (+17.01% YoY)

- Retail Deposits: ₹1,24,306 crore (+13.66% YoY)

- CASA Deposits: ₹41,495 crore (+14.61% YoY)

- CASA Ratio: 32.98% (vs. 32.06% YoY)

- Gross NPA: 1.38% (vs. 3.15%)

- Net NPA: 0.26% (vs. 0.68%)

- Provision Coverage Ratio (Excluding Write-offs): 81.40%

- Provision Coverage Ratio (Including Write-offs): 94.51%

Highlight:

- South Indian Bank posted its highest-ever quarterly Net Interest Income of ₹1,025 crore while net profit rose 17.29% YoY to ₹377.63 crore and Gross NPA improved to 1.38%.

What Happened ?

South Indian Bank delivered a resilient Q1 FY27 performance, driven by strong loan growth, expanding retail liabilities, and a significant improvement in asset quality.

Net Interest Income crossed the ₹1,000 crore mark for the first time, supported by healthy credit expansion and improved deposit mobilisation. The bank also reduced credit costs through lower provisioning while maintaining robust growth across corporate, gold loan, mortgage, and business banking segments.

key details

Business Performance & Asset Quality:

- Highest-ever quarterly Net Interest Income reached ₹1,025 crore, growing 23.05% YoY.

- Gross advances increased 17.01% YoY to ₹1,04,368 crore.

- Retail deposits rose 13.66% YoY to ₹1,24,306 crore.

- CASA deposits grew 14.61% YoY, improving the CASA ratio to 32.98%.

- NRI deposits increased 12.82% YoY to ₹36,432 crore.

- Gold loan portfolio registered strong growth of 42.90% YoY, reaching ₹24,930 crore.

- Mortgage loan portfolio expanded 78.65% YoY to ₹5,856 crore.

- Corporate advances increased 12.38% YoY, primarily through well-rated borrowers.

- Business banking advances grew 13.67% YoY.

- Vehicle loan portfolio expanded 12.63% YoY.

- Gross NPA declined by 177 basis points to 1.38%, while Net NPA reduced by 42 basis points to 0.26%.

- Provision Coverage Ratio improved to 81.40% (excluding write-offs) and 94.51% (including write-offs).

- Approximately 98.81% of large corporate exposure is rated A and above, reflecting a high-quality corporate loan book.

Note:

- Although operating profit and other income declined year-on-year, lower provisioning expenses and higher Net Interest Income supported overall profitability during the quarter. The financial results include the performance of the bank’s wholly owned subsidiary, SIBOSL.

Risk Analysis

Summary:

- The bank reported meaningful improvement in profitability and asset quality; however, sustaining earnings momentum will depend on continued loan growth, deposit mobilisation, and maintaining low credit costs.

Key Risks:

- Operating profit declined despite higher net profit due to lower other income.

- Other income contracted significantly during the quarter.

- Sustaining current asset quality improvements remains important as credit expands.

- Margin performance may remain sensitive to changes in interest rate cycles.

Worst Case:

- A slowdown in credit demand, pressure on margins, or deterioration in asset quality could impact future profitability and provisioning requirements.

Risk Level: Medium

Company Commentary

- Management reiterated its focus on sustained profitability, superior asset quality, and a resilient loan portfolio.

- The bank continues strengthening its organisational structure while leveraging digital technology to improve business execution.

- Growth during the quarter was driven by quality asset acquisition across Corporate Lending, Auto Loans, and Gold Loans.

- The bank reaffirmed its strategy of “Profitability through Quality Credit Growth”, emphasising the onboarding of low-risk borrowers to maintain a balanced credit portfolio.

Official Exchange Filing: South Indian Bank Limited