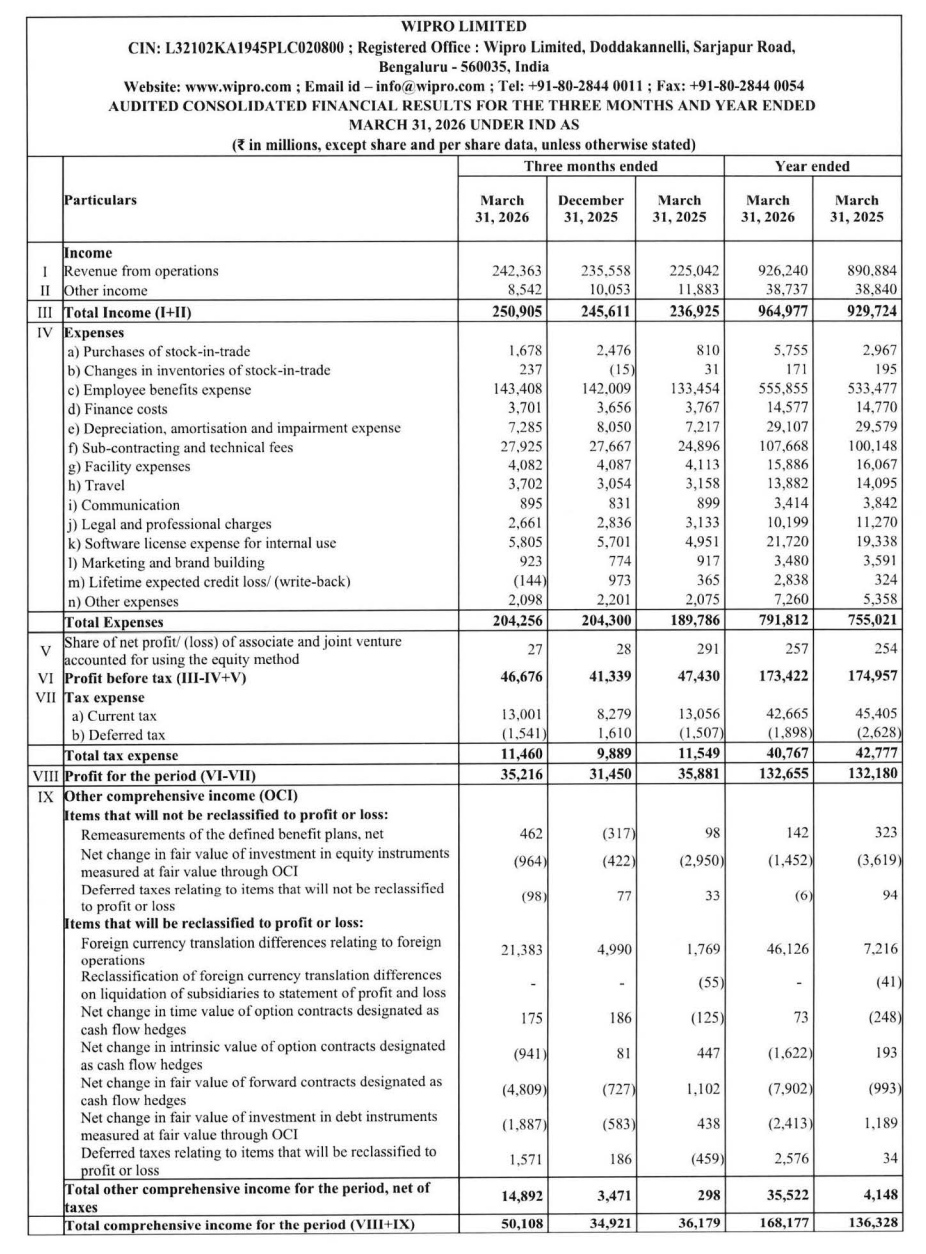

Quarter Ended: March 2026

Wipro Ltd – Q4 FY26 Results Analysis

NSE

wipro

BSE

507685

Wipro delivered modest revenue growth with stable YoY profitability, but QoQ margin pressure indicates operational challenges.

key financial highlights

- Revenue from Operations:

- Q4 FY26 Revenue: ₹2,42,363 million

- QoQ Change: +2.9% (from ₹2,35,558 million)

- YoY Change: +7.7% (from ₹2,25,042 million)

- Moderate growth driven by steady IT services demand

- Profit After Tax (PAT):

- Q4 FY26 PAT: ₹35,216 million

- QoQ Change: +12.0% (from ₹31,450 million)

- YoY Change: -1.9% (from ₹35,881 million)

- Profit improved sequentially but declined slightly YoY due to cost pressures

- QoQ Trend Insight:

- Revenue Trend: Mild Growth

- Profit Trend: Recovery

Margin Analysis

- High employee cost (major expense component)

- Increased subcontracting and tech costs

- Slight improvement in operating efficiency QoQ

Key Signal: Margins are under pressure YoY but stabilizing QoQ

Segment performance

Segment Insight:

- IT services-driven revenue model

- Exposure to global enterprise spending

Characteristics:

- High dependency on client budgets

- Currency sensitivity (USD exposure)

- Cost-heavy workforce model

Earning quality check

Drivers:

- Core operational income driven

- No major exceptional distortions

- Stable cash flow generation

Interpretation: Earnings quality is stable but not high-growth

balance sheet analysis

- Total Assets: ₹1,414,077 million

- Total Liabilities: ₹531,385 million

Indicates: Strong balance sheet with healthy equity base and manageable liabilities

key risks

- Slowdown in global IT spending

- Margin pressure due to wage inflation

- Currency fluctuations

- High competition (TCS, Infosys, Accenture)

management strategy

- Cost optimization

- Digital and cloud services expansion

- Improving deal pipeline

Financial Metrics

| Particular | In ₹ Million | Q.O.Q (%) | Y.O.Y(%) |

|---|---|---|---|

| Total Income | 2,50,905 | 2.2 | 5.9 |

| PBT | 46,676 | 12.9 | -1.6 |

| PAT | 35,216 | 12.0 | -1.9 |

| EPS | 3.34 | 12.0 | -2.0 |

Wipro delivered a stable but uninspiring quarter, with moderate revenue growth and improving QoQ profitability. However, margin pressure and weak YoY profit growth suggest limited near-term upside.

Official Exchange Filing: WIPRO Limited

Quarterly Performance Context

REVENUE ACHIEVMENT

100%

COST OF OPERATIONS

84%

NET PROFIT

15%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED