Earnings Announcement

RBL Bank Reports Strong FY26 Earnings with 18% Profit Growth and Improved Asset Quality

NSE

rblbank

BSE

540065

RBL Bank reported robust FY26 performance with 18% YoY profit growth, strong advances and deposit expansion, and improving asset quality, despite margin compression

PRICE-SENSITIVE TRIGGER

Event: Q4 & FY26 Audited Financial Results

Type: Earnings Announcement

Impact: Positive

Immediate Effect: Strengthens confidence in growth momentum, asset quality improvement, and retail-led expansion strategy

Key Metrics:

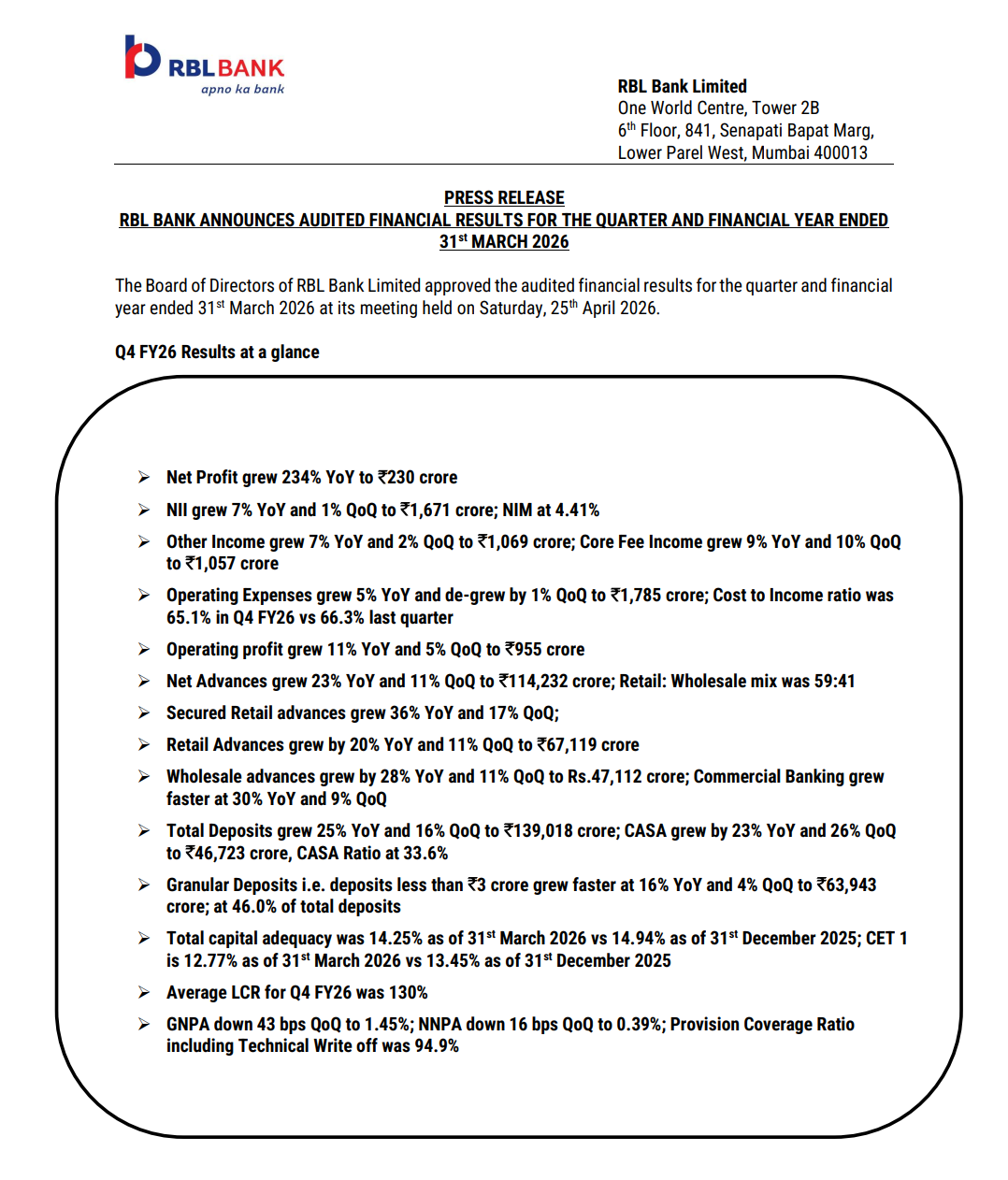

- FY26 Net Profit: ₹822 crore (+18% YoY)

- Q4 Net Profit: ₹230 crore (+234% YoY)

- Net Interest Income (FY26): ₹6,360 crore (-2% YoY)

- Net Interest Margin (FY26): 4.51%

- Operating Profit (FY26): ₹3,299 crore

- Advances: ₹1,14,232 crore (+23% YoY)

- Deposits: ₹1,39,018 crore (+25% YoY)

- GNPA: 1.45% (improved)

- NNPA: 0.39%

Highlight:

- Net Profit growth of 234% YoY in Q4 FY26

What Happened ?

RBL Bank announced its audited financial results for Q4 and FY26, showcasing strong profit growth, accelerated advances and deposits expansion, and notable improvement in asset quality metrics.

key highlights

Operational & Financial Performance:

- Net profit surged 234% YoY in Q4, reflecting operating leverage

- FY26 profit grew 18% YoY to ₹822 crore

- Advances grew 23% YoY, led by retail and secured lending

- Deposits increased 25% YoY with strong CASA growth

- CASA ratio improved to ~33.6%

- Secured retail advances grew 36% YoY

- Asset quality improved with GNPA at 1.45% and NNPA at 0.39%

- Provision Coverage Ratio (incl. write-offs) strong at ~94.9%

- Capital adequacy at 14.25%, ensuring growth support

- Network expanded to 603 branches and 1,942 touchpoints

Note:

- Growth is primarily driven by granular retail strategy and improved liability franchise

Risk Analysis

Key Risks

- NIM declined YoY indicating margin compression

- Cost-to-income ratio elevated at ~68.5%

- Dependence on retail growth sustainability

- Competitive pressure in lending and deposits

- Capital adequacy slightly declined QoQ

Worst Case Scenario

- Sustained margin pressure and rising costs could limit profitability despite balance sheet growth

Risk Level: Medium

Company Commentary

- Focus on disciplined execution and profitable growth

- Strong traction in granular retail advances and deposits

- Continued investment in branch expansion and customer franchise

- Balance sheet remains resilient and well-capitalized

Official Exchange Filing: RBL Bank Limited