Quarter Ended: March 2026

Kirloskar Pneumatic Company Ltd – Q4 FY26 Results Analysis

NSE

kirlpnu

BSE

505283

The company delivered a sharp sequential improvement in revenue and profitability driven by compression systems, though YoY profit growth remains moderate due to cost pressures

key financial highlights

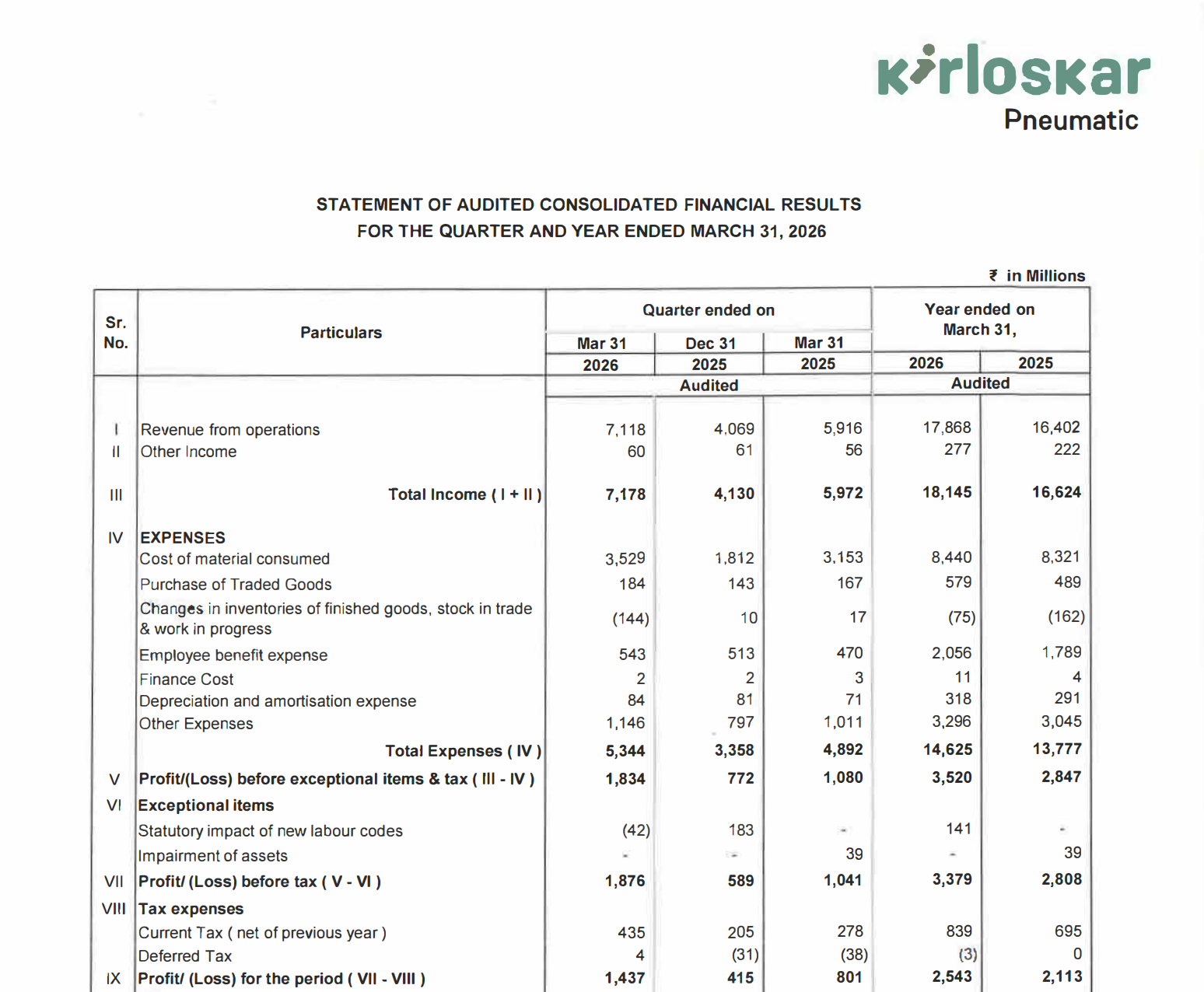

- Revenue from Operations:

- Total Income (Q4 FY26): ₹7,118 million

- QoQ Change: +74.93%

- YoY Change: +20.31%

- Previous Quarter (Q3 FY26): ₹4,069 million

- Previous Year (Q4 FY25): ₹5,916 million

- Total Income (Q4 FY26): ₹7,118 million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹1,437 million

- QoQ Change: +246.51%

- YoY Change: +79.40%

- Previous Quarter (Q3 FY26): ₹415 million

- Previous Year (Q4 FY25): ₹801 million

- PAT (Q4 FY26): ₹1,437 million

- QoQ Performance

- Revenue Trend: Sharp recovery

- Profit Trend: Strong expansion

Margin Analysis

Key Drivers:

- Strong operating leverage from revenue spike

- Controlled cost growth relative to revenue

- Higher contribution from core compression systems

Key Signal: Margins expanded significantly with profit growing faster than revenue

Segment performance

Segment: Compression Systems

- Revenue: ₹6,819 million

Insights:

- Core revenue driver

- Strong QoQ and YoY growth

- High profitability contributor

Segment: Other Segments

- Revenue: ₹299 million

Insights:

- Minor contribution

- Stable performance

Segment insight

Summary:

- Business is highly concentrated in compression systems segment driving both revenue and profitability

Characteristics:

- Core segment dominance

- Industrial demand-driven growth

- Limited diversification

Earning quality check

Drivers:

- Strong operating profit growth

- Limited exceptional items impact

- Contribution from fair value gains

Interpretation:

- Earnings quality is solid, though partially supported by financial instrument gains

balance sheet Analysis

- Total Assets: ₹17,574 million

- Total Liabilities: ₹4,978 million

Insight:

- Strong balance sheet with lower leverage and high equity base

key risks

- Dependence on single dominant segment

- Industrial demand cyclicality

- Exposure to commodity/input costs

management strategy signals

- Focus Areas:

- Expansion in compression systems

- Capital efficiency improvement

- Strengthening order book

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹7,118 Million | +74.93% | +20.31% |

| PBT | ₹1,876 Million | +218.50% | +80.21% |

| PAT | ₹1,437 Million | +246.51% | +79.40% |

Kirloskar Pneumatic delivered a high-impact quarter with strong revenue growth and exceptional profit expansion driven by operating leverage. The business shows strong momentum, though concentration risk and cyclicality remain key factors to monitor.

Official Exchange Filing: Kirloskar Pneumatic Company Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED