Quarter Ended: March 2026

UltraTech Cement Ltd – Q4 FY26 Results Analysis

NSE

ultracemco

BSE

532538

Revenue growth remains robust driven by scale and demand, but rising costs (power, freight, and raw materials) are limiting margin expansion despite healthy profit growth

key financial highlights

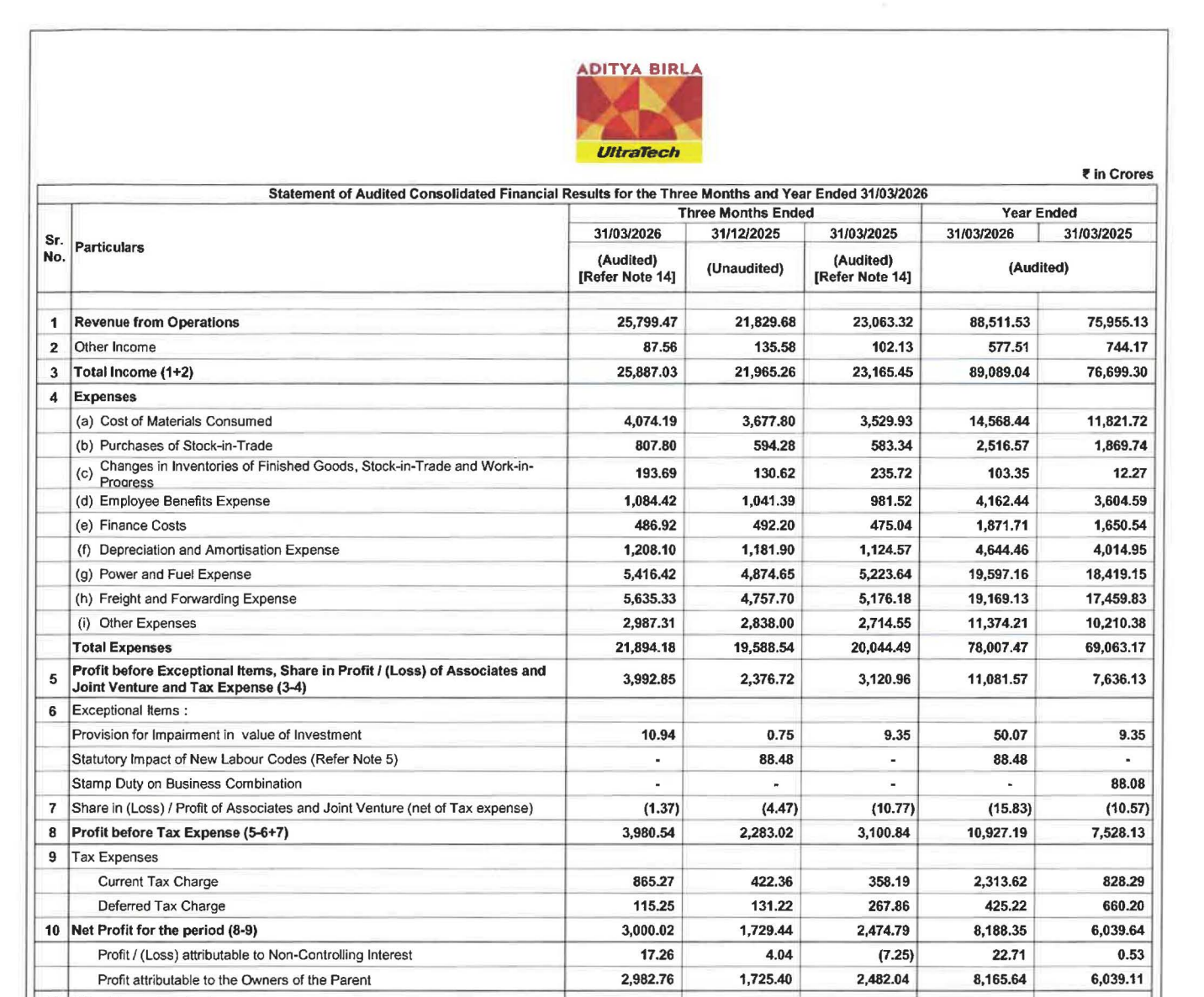

- Revenue from Operations:

- Total Income (Q4 FY26): ₹25,799.47 Cr

- QoQ Change: +18.19%

- YoY Change: +11.86%

- Previous Quarter (Q3 FY26): ₹21,829.68 Cr

- Previous Year (Q4 FY25): ₹23,063.32 Cr

- Total Income (Q4 FY26): ₹25,799.47 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹3,000.02 Cr

- QoQ Change: +73.60%

- YoY Change: +21.05%

- Previous Quarter (Q3 FY26): ₹1,729.44 Cr

- Previous Year (Q4 FY25): ₹2,477.79 Cr

- PAT (Q4 FY26): ₹3,000.02 Cr

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Sharp recovery

Margin Analysis

Key Drivers:

- Increase in power & fuel costs

- Higher freight and forwarding expenses

- Operating leverage from higher volumes

Key Signal: Margins under pressure despite revenue growth, indicating cost inflation impact

Earning quality check

Drivers:

- Strong core operational performance

- Limited exceptional impact in current quarter

- Stable tax structure

Interpretation:

- Earnings are largely operationally driven, indicating healthy business fundamentals

balance sheet Analysis

- Total Assets: ₹1,41,376.05 Cr

- Total Liabilities: ₹60,663.61 Cr (Derived)

Insight:

- Strong asset base with significant capital deployment; leverage remains manageable relative to scale

key risks

- Rising fuel and logistics costs

- Cyclical demand in infrastructure and real estate

- High capex impacting free cash flows

management strategy signals

- Focus Areas:

- Capacity expansion

- Cost optimization (energy efficiency, logistics)

- Market share expansion

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹25,799.47 Crore | +18.19% | +11.86% |

| PBT | ₹3,980.54 Crore | +74.33% | +28.36% |

| PAT | ₹3,000.02 Crore | +73.60% | +21.05% |

UltraTech Cement delivered a strong operational quarter, driven by volume growth and improved profitability. However, margin pressure from rising input and logistics costs remains a concern. Long-term outlook remains positive due to scale and market leadership, but near-term profitability depends on cost control.

Official Exchange Filing: Ultratech Cement Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

85%

NET PROFIT AS % OF REVENUE

11.63%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED