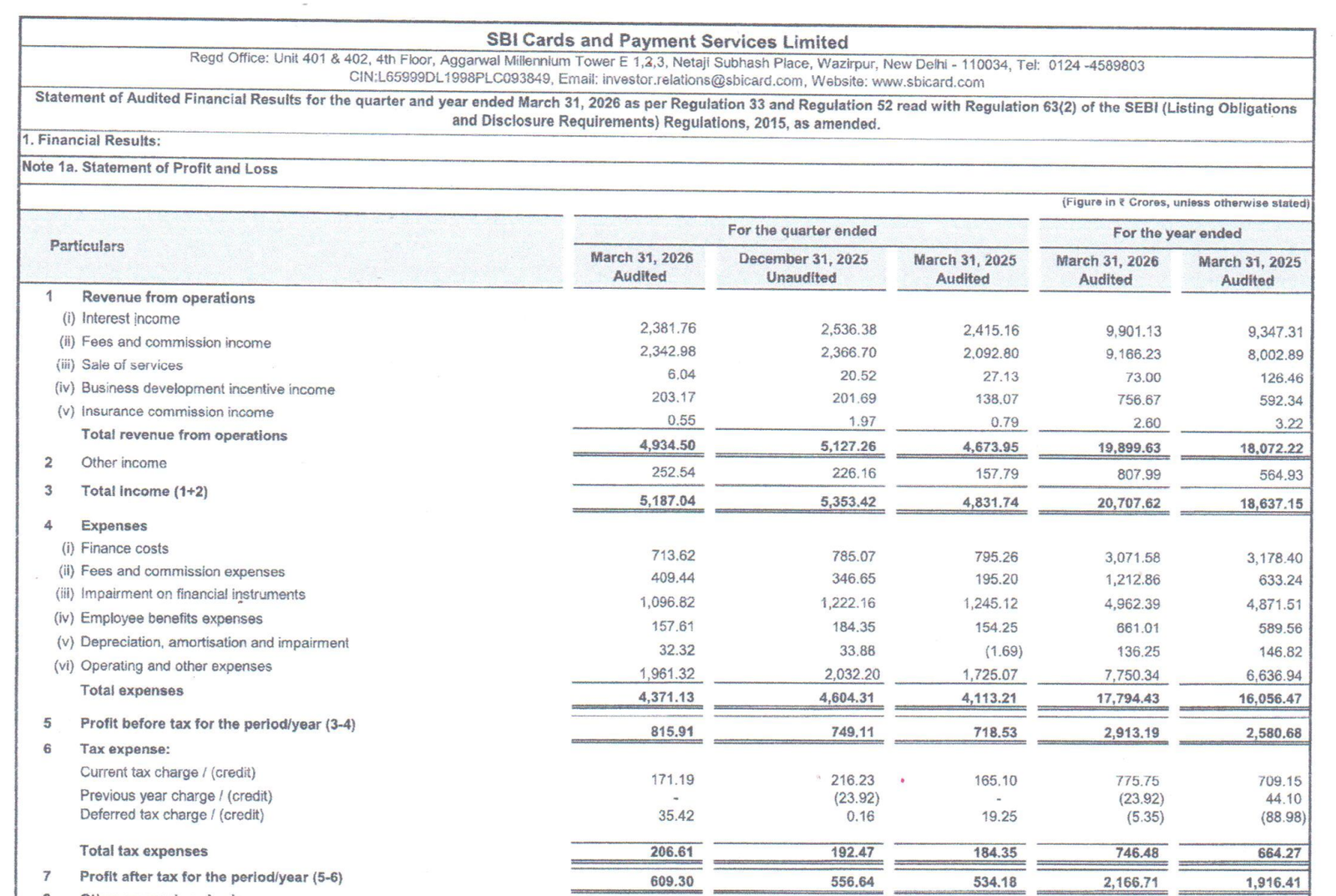

Quarter Ended: March 2026

SBI Cards & Payment Services Ltd – Q4 FY26 Results Analysis

NSE

sbicard

BSE

543066

Revenue and profit growth remain steady, but high credit costs and weak operating cash flow highlight underlying stress in the lending portfolio

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹4,934.50 Cr

- QoQ Change: -3.76%

- YoY Change: +5.57%

- Previous Quarter (Q3 FY26): ₹5,127.26 Cr

- Previous Year (Q4 FY25): ₹4,673.95 Cr

- Total Income (Q4 FY26): ₹4,934.50 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹609.30 Cr

- QoQ Change: +9.46%

- YoY Change: +14.06%

- Previous Quarter (Q3 FY26): ₹556.64 Cr

- Previous Year (Q4 FY25): ₹534.18 Cr

- PAT (Q4 FY26): ₹609.30 Cr

- QoQ Performance

- Revenue Trend: Slight decline

- Profit Trend: Moderate improvement

Margin Analysis

Key Drivers:

- High impairment on financial instruments (credit cost pressure)

- Stable finance costs

- Controlled operating expenses

Key Signal: Margins are stable but under pressure due to elevated credit costs

Segment insight

Summary:

- Business is primarily driven by credit card lending and fee-based income

Characteristics:

- High dependence on unsecured lending

- Fee + interest income mix

- Sensitive to credit cycle

Earning quality check

Drivers:

- Strong interest income growth

- High impairment charges (~₹1,096 Cr quarterly impact)

- Stable fee income

Interpretation:

- Earnings are operationally sound but impacted by elevated credit costs, indicating moderate stress

balance sheet Analysis

- Total Assets: ₹66,327.79 Cr

- Total Liabilities: ₹50,602.29 Cr

Insight:

- Strong asset growth driven by loan book expansion, with high leverage typical of NBFC model

key risks

- Rising NPAs / credit losses

- Weak operating cash flow (₹493 Cr vs negative last year recovery base)

- High dependence on unsecured lending segment

- Interest rate sensitivity

management strategy signals

- Tightening credit underwriting

- Improving collections efficiency

- Expanding card base and spends

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹5,187.04 Crore | -3.11% | +7.35% |

| PBT | ₹815.91 Crore | +8.91% | +13.55% |

| PAT | ₹609.30 Crore | +9.46% | +14.06% |

SBI Cards delivered a stable but cautious quarter, with steady profit growth despite declining revenue QoQ. Elevated credit costs remain a key concern, signaling stress in the unsecured lending cycle. Near-term outlook depends heavily on asset quality normalization

Official Exchange Filing: SBI Cards & Payment Services Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

84%

NET PROFIT AS % OF REVENUE

12.35%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED