Quarter Ended: March 2026

Mahindra Holidays & Resorts India Ltd – Q4 FY26 Results Analysis

NSE

mhril

BSE

533088

Revenue growth remains steady, but profitability is under pressure on a yearly basis due to rising costs and weaker segment performance in HCRO

key financial highlights

- Revenue from Operations:

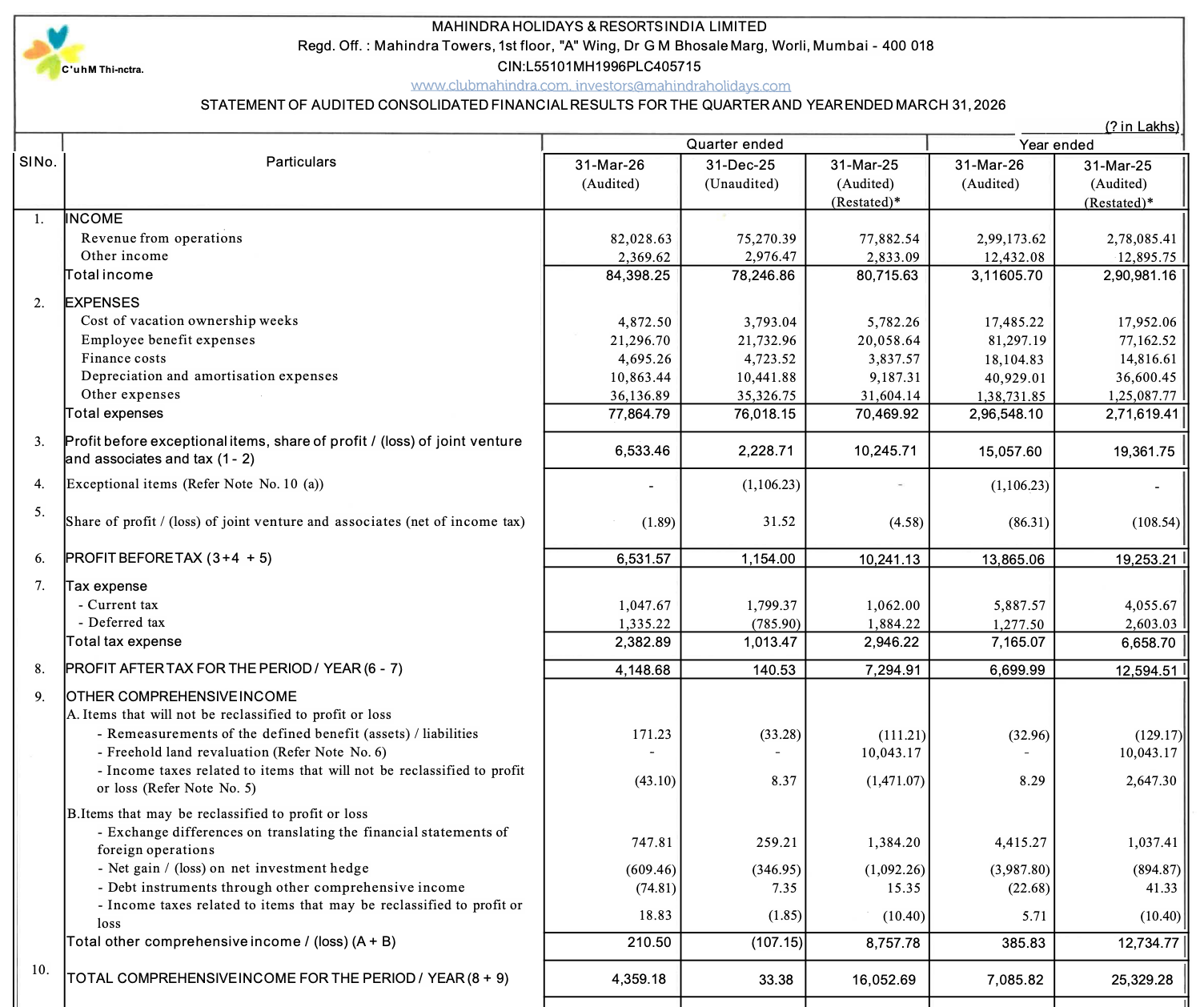

- Total Income (Q4 FY26): ₹84,398.25 Lakhs

- QoQ Change: +7.86%

- YoY Change: +4.56%

- Previous Quarter (Q3 FY26): ₹78,246.86 Lakhs

- Previous Year (Q4 FY25): ₹80,715.63 Lakhs

- Total Income (Q4 FY26): ₹84,398.25 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹4,148.68 Lakhs

- QoQ Change: +2,852.73%

- YoY Change: -43.13%

- Previous Quarter (Q3 FY26): ₹140.53 Lakhs

- Previous Year (Q4 FY25): ₹7,294.91 Lakhs

- PAT (Q4 FY26): ₹4,148.68 Lakhs

- QoQ Performance

- Revenue Trend: Moderate growth

- Profit Trend: Sharp recovery (low base)

Margin Analysis

Key Drivers:

- Rising employee and operating expenses

- Higher depreciation and finance costs

- Weak performance in HCRO segment

Key Signal: Margins compression visible YoY despite revenue growth

Segment performance

Segment: MHRIL (Core Business)

- Revenue: ₹40,675.10 Lakhs

Insights:

- Stable performance

- Core profit contributor

Segment: HCRO (Holiday Club Resorts Oy)

- Revenue: ₹43,723.15 Lakhs

Insights:

- Higher revenue contribution

- Loss-making at PBT level

Segment insight

Summary:

- Growth is supported by both segments, but profitability is impacted by HCRO losses

Characteristics:

- Dual geography exposure

- High fixed cost structure

- Currency and international exposure

Earning quality check

Drivers:

- Core operational earnings

- Minimal exceptional items impact

- High depreciation component

Interpretation:

- Earnings quality is moderate, with structural cost pressures affecting profitability

balance sheet Analysis

- Total Assets: ₹11,38,456.78 Lakhs

- Total Liabilities: ₹10,60,091.39 Lakhs

Insight:

- High liability structure with significant deferred revenue and lease liabilities typical of hospitality model

key risks

- Losses in international (HCRO) segment

- High fixed cost structure

- Demand sensitivity to discretionary spending

- Currency fluctuation impact

management strategy signals

- Improving profitability in HCRO

- Cost optimization

- Membership growth in core business

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹84,398.25 Lakhs | +7.86% | +4.56% |

| PBT | ₹6,531.57 Lakhs | +466.24% | -36.23% |

| PAT | ₹4,148.68 Lakhs | +2852.73% | -43.13% |

Mahindra Holidays delivered a mixed quarter, with strong sequential recovery in profitability but clear YoY margin pressure. The drag from the HCRO segment and rising costs remains a concern. Future performance hinges on margin recovery and turnaround in international operations.

Official Exchange Filing: Mahindra Holidays & Resorts India Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED