Earnings Update

Websol Energy Q4FY26 Revenue Surges 132% YoY to ₹401 Cr; PAT Jumps 158%

NSE

webelsolar

BSE

517498

Websol Energy System Ltd reported a strong Q4FY26 performance with 132% YoY revenue growth and 158% YoY PAT growth, driven by capacity expansion, improved utilization, and operating efficiency

PRICE-SENSITIVE TRIGGER

Event: Q4 & FY26 Financial Results Announcement

Type: Earnings Update

Impact: Positive

Immediate Effect: Signals strong earning momentum and improved profitability

Key Metrics:

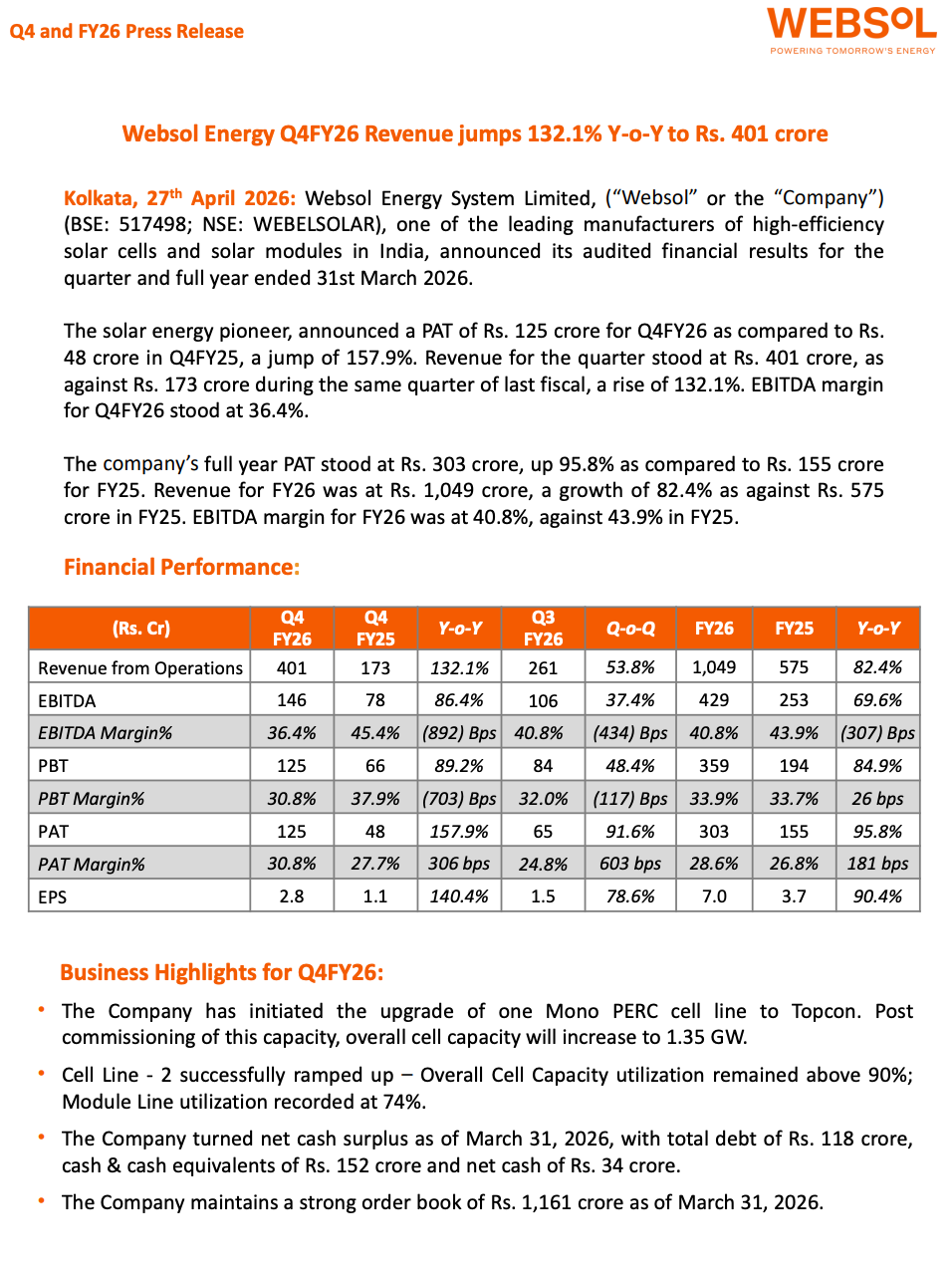

- Q4 Revenue: ₹401 Cr (↑132.1% YoY)

- Q4 PAT: ₹125 Cr (↑157.9% YoY)

- FY26 Revenue: ₹1,049 Cr (↑82.4% YoY)

- FY26 PAT: ₹303 Cr (↑95.8% YoY)

- Q4 EBITDA Margin: 36.4%

- FY26 EBITDA Margin: 40.8%

Highlight:

- PAT growth of ~158% YoY in Q4FY26

What Happened ?

Websol Energy announced robust quarterly and annual financial results, supported by:

- Capacity ramp-up (Cell Line-2 commissioning)

- Strong operating leverage

- Improved cost discipline and utilization

key highlights

Quarterly Performance (Q4FY26):

- Revenue: ₹401 Cr vs ₹173 Cr YoY

- EBITDA: ₹146 Cr vs ₹78 Cr YoY

- PAT: ₹125 Cr vs ₹48 Cr YoY

- EPS: ₹2.8 vs ₹1.1 YoY

Full-Year Performance (FY26):

- Revenue: ₹1,049 Cr vs ₹575 Cr YoY

- EBITDA: ₹429 Cr vs ₹253 Cr YoY

- PAT: ₹303 Cr vs ₹155 Cr YoY

- EPS: ₹7.0 vs ₹3.7 YoY

Operational Highlights:

- Cell Line-2 successfully commissioned

- Cell capacity to increase to 1.35 GW

- Capacity utilization:

- Cells: >90%

- Modules: ~74%

- Net cash position achieved:

- Cash: ₹152 Cr

- Debt: ₹118 Cr

- Strong order book: ₹1,161 Cr

Strategic Developments:

- Upgrade of Mono PERC line to Topcon technology

- Progress toward 2 GW integrated facility

- Focus on backward integration

Note:

- Clear transition from expansion phase → scale + efficiency phase

Risk Analysis

Key Risks

- EBITDA margin compression (YoY decline in Q4)

- Solar industry pricing volatility

- Dependence on policy support (PLI, ALMM)

- Execution risk in capacity expansion

Worst Case Scenario

- Sharp decline in module pricing impacts margins despite volume growth

Risk Level: Medium

Company Commentary

- FY26 marked a landmark year with commissioning of Cell Line-2

- Capacity expansion strengthens core business and future growth

- Upgrade to Topcon technology to enhance efficiency

- Focus on working capital discipline and cost optimization

- Strong revenue, profitability, and cash flow performance achieved

- Positioned to benefit from strong solar sector tailwinds

Official Exchange Filing: Websol Energy System Ltd