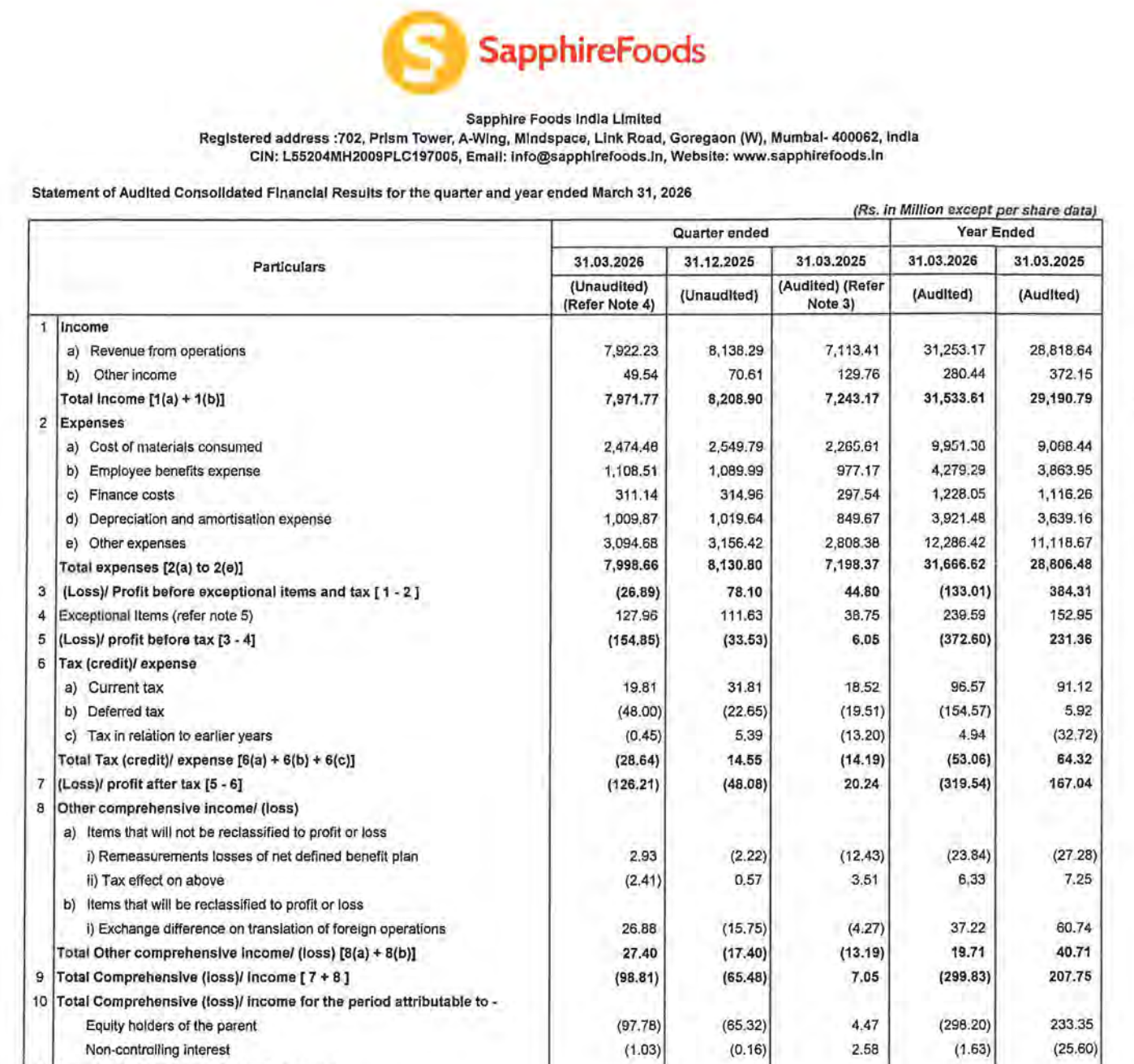

Quarter Ended: March 2026

Sapphire Foods India – Q4 FY26 Results Analysis

NSE

sapphire

BSE

543397

Despite steady topline growth, rising operating and finance costs have pushed the company into losses, highlighting margin stress in the QSR business

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹792.22 Cr

- QoQ Change: -2.65%

- YoY Change: +11.35%

- Previous Quarter (Q3 FY26): ₹813.83 Cr

- Previous Year (Q4 FY25): ₹711.34 Cr

- Revenue (Q4 FY26): ₹792.22 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): -₹12.62 Cr (Loss)

- QoQ Change: Deterioration

- YoY Change: Down

- Previous Quarter (Q3 FY26): -₹4.81 Cr

- Previous Year (Q4 FY25): ₹20.24 Cr

- PAT (Q4 FY26): -₹12.62 Cr (Loss)

- QoQ Performance

- Revenue Trend: Slight Decline

- Profit Trend: Weak / Loss-making

Margin Analysis

Key Drivers:

- High employee benefit expenses (~₹110 Cr)

- Increase in finance costs (~₹31 Cr)

- Rising store operating costs

- Negative operating leverage in some regions

Key Signal: Margins have turned negative, indicating serious pressure from cost escalation vs revenue growth

Segment insight

Summary:

- Business driven by QSR chains (KFC, Pizza Hut) with expansion-led growth

Characteristics:

- Aggressive store expansion strategy

- High dependence on urban consumption demand

- Cost-heavy model with high fixed expenses

Earning quality check

Drivers:

- Weak core profitability

- High operating cost base

- Limited contribution from non-operating income

Interpretation:

- Earnings quality is weak, as growth is not translating into profitability

balance sheet Analysis

- Total Assets: ₹3,255.89 Cr

- Total Liabilities: ₹1,867.04 Cr

Insight:

- Rising lease liabilities (store expansion impact)

- Moderate debt but increasing financial obligations

- Stable equity base (~₹1,388 Cr)

- Working capital pressures visible

key risks

- High cost inflation (food, rentals, wages)

- Weak consumer demand in QSR segment

- Negative operating leverage

- Expansion risk without profitability

- Dependence on discretionary spending

management strategy signals

Focus Area:

- Store expansion

- Brand strengthening (KFC, Pizza Hut)

- Cost optimization

- Improving store-level profitability

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹797.18 Crore | -2.89% | +10.06% |

| PBT | -₹15.48 Crore | Deterioration | Sharp Decline |

| PAT | -₹12.62 Crore | Negative | Down from Profit |

Sapphire Foods is currently facing a classic growth vs profitability dilemma. While revenue continues to grow, cost pressures and expansion expenses are eroding margins, leading to losses. The near-term outlook remains cautious unless the company achieves better operating leverage and cost control.

Official Exchange Filing: Sapphire Foods Ltd

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED

Keep on writing, great job!

Thank you so much for your wonderful words