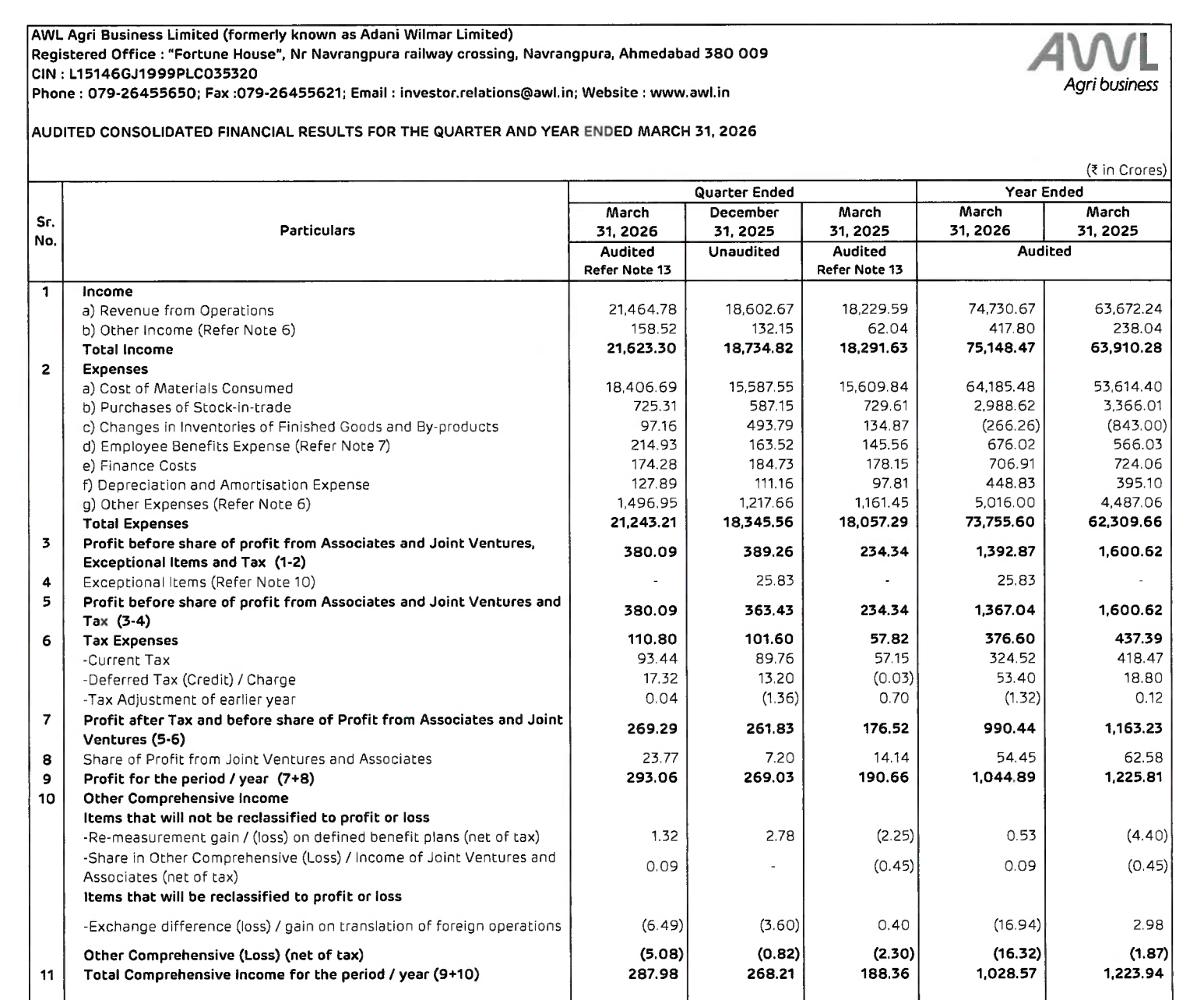

Quarter Ended: March 2026

AWL Agri – Q4 FY26 Results

NSE

awl

BSE

543458

Strong topline growth led by edible oil segment, but margin compression and cost pressures impacted profitability significantly

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹21,464.78 Cr

- QoQ Change: +15.4%

- YoY Change: +17.7%

- Previous Quarter (Q3 FY26): ₹18,602.67 Cr

- Previous Year (Q4 FY25): ₹18,229.59 Cr

- Revenue (Q4 FY26): ₹21,464.78 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹293.06 Cr

- QoQ Change: +9.0%

- YoY Change: +53.7%

- Previous Quarter (Q3 FY26): ₹269.03 Cr

- Previous Year (Q4 FY25): ₹190.66 Cr

- PAT (Q4 FY26): ₹293.06 Cr

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Moderate growth

Margin Analysis

Key Drivers:

- High raw material cost (₹18,406 Cr)

- Increased operating and distribution expenses

- Volatility in edible oil pricing

- Thin margins in core edible oil business

Key Signal: Despite revenue growth, margin profile remains structurally thin, limiting profit scalability

Segment performance

Segment: Edible Oil

Revenue: ₹17,519.80 Cr

Insights:

- Dominant contributor (~82% of revenue)

- Volume-driven growth

- Highly price-sensitive business

Segment: Food & FMCG

Revenue: ₹1,730.51 Cr

Insights:

- Emerging growth segment

- Better margin potential vs edible oil

Segment: Industry Essentials

Revenue: ₹2,214.47 Cr

Insights:

- Stable contribution

- Linked to industrial demand cycles

Segment insight

Summary:

- Business is heavily dependent on edible oil segment, which drives volume but limits margins, while FMCG is the future margin driver

Characteristics:

- Commodity-linked pricing

- High volume, low margin model

- FMCG transition underway

- Diversification in progress

Earning quality check

Drivers:

- Strong operating cash flow: ₹3,928 Cr

- High working capital movement

- Commodity-driven earnings volatility

Interpretation:

- Earnings quality is moderate, supported by cash flows but exposed to commodity cycles

balance sheet Analysis

- Total Assets: ₹24,758.62 Cr

- Total Liabilities: ₹14,314.94 Cr

Insight:

- Strong working capital intensity (inventory ₹8,190 Cr)

- Increased borrowings

- Stable equity base (~₹10,443 Cr)

key risks

- Commodity price volatility (edible oil)

- Thin operating margins

- High working capital requirement

- Dependence on import/export policies

management strategy signals

Focus Area:

- Expanding FMCG segment

- Strengthening brand portfolio

- Improving margin mix

- Backward integration

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹21,623.30 Crore | +15.4% | +18.2% |

| PBT | ₹380.09 Crore | +4.6% | +62.1% |

| PAT | ₹293.06 Crore | +9.0% | +53.7% |

AWL Agri is a high-volume, low-margin business, showing strong revenue growth but limited profitability expansion. The real long-term story lies in its FMCG transition, which, if successful, can significantly improve margins.

Official Exchange Filing: AWL Agri Business Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED