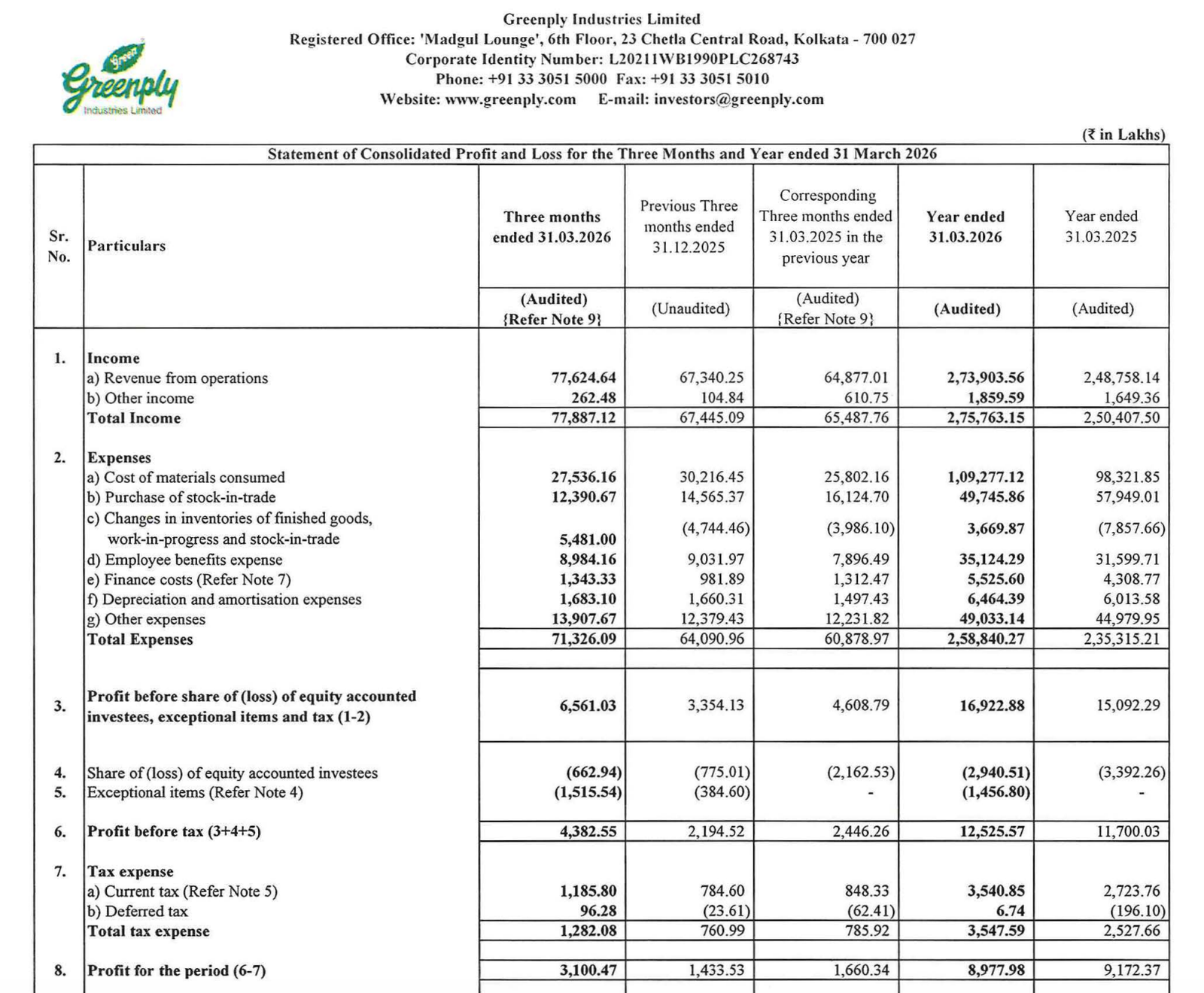

Quarter Ended: March 2026

Greenply Industries Ltd – Q4 FY26 Results

NSE

greenply

BSE

526797

Revenue growth supported by both plywood and MDF segments, while operating leverage and cost control drove sharp profitability improvement

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹7,762.46 Cr

- QoQ Change: +15.3%

- YoY Change: +19.7%

- Previous Quarter (Q3 FY26): ₹6,734.03 Cr

- Previous Year (Q4 FY25): ₹6,487.70 Cr

- Revenue (Q4 FY26): ₹7,762.46 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹310.05 Cr

- QoQ Change: +116.3%

- YoY Change: +86.7%

- Previous Quarter (Q3 FY26): ₹143.35 Cr

- Previous Year (Q4 FY25): ₹166.03 Cr

- PAT (Q4 FY26): ₹310.05 Cr

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Sharp recovery

Margin Analysis

Key Drivers:

- Operating leverage from higher volumes

- Better product mix (MDF growth)

- Controlled raw material cost inflation

- Improved cost efficiency

Key Signal: Margins expanded meaningfully as cost growth lagged revenue growth, indicating strong operating discipline

Segment performance

Segment: Plywood & Allied Products

Revenue: ₹5,873.84 Cr

Insights:

- Core segment (~75% contribution)

- Stable demand and pricing

Segment: MDF & Allied Products

Revenue: ₹1,889.49 Cr

Insights:

- Fastest growing segment

- Higher margin profile vs plywood

Segment insight

Summary:

- Greenply is successfully transitioning toward MDF-led growth, which is structurally higher margin and scalable

Characteristics:

- MDF = Growth + Margin driver

- Plywood = Stable cash generator

- Balanced portfolio improving profitability

Earning quality check

Drivers:

- Strong operating cash flow: ₹246.88 Cr

- Working capital improvement (inventory reduction)

- Lower reliance on non-operating income

Interpretation:

- Earnings quality is high, driven by core operations and cash generation

balance sheet Analysis

- Total Assets: ₹19,616.54 Cr

- Total Liabilities: ₹10,662.83 Cr

Insight:

- Strong equity base (~₹8,953 Cr)

- Controlled leverage

- Improved working capital cycle

key risks

- Raw material cost volatility (timber)

- Demand slowdown in real estate

- Competitive pressure in MDF segment

- Capex execution risks

management strategy signals

Focus Area:

- MDF capacity expansion

- Premium product positioning

- Distribution expansion

- Brand strengthening

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹7,788.71 Crore | +15.3% | +18.9% |

| PBT | ₹438.26 Crore | +99.7% | +79.2% |

| PAT | ₹310.05 Crore | +116.3% | +86.7% |

Greenply has delivered a high-quality quarter, with:

- Strong revenue growth

- Sharp margin expansion

- Significant PAT recovery

The company is clearly benefiting from its MDF strategy, making it a margin expansion story rather than just volume growth.

Official Exchange Filing: Greenply Industries Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

92%

NET PROFIT AS % OF REVENUE

4%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED