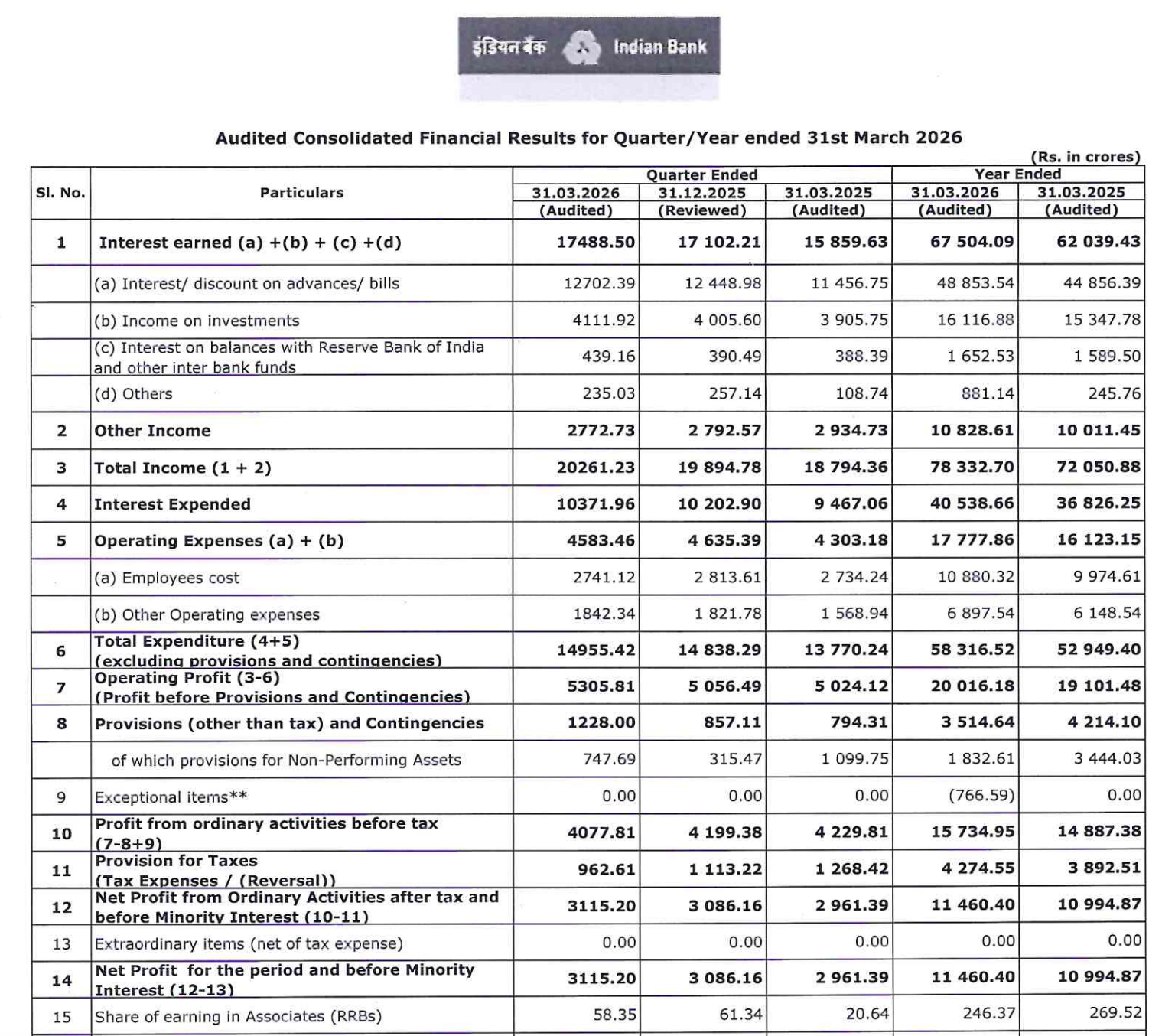

Quarter Ended: March 2026

Indian Bank – Q4 FY26 Results

NSE

indianb

BSE

532814

Strong loan growth, declining NPAs, and stable margins support consistent earnings trajectory

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹20,261 Cr

- QoQ Change: +1.84%

- YoY Change: +7.80%

- Previous Quarter (Q3 FY26): ₹19,894 Cr

- Previous Year (Q4 FY25): ₹18,794 Cr

- Revenue (Q4 FY26): ₹20,261 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹3,173 Cr

- QoQ Change: +0.86%

- YoY Change: +6.41%

- Previous Quarter (Q3 FY26): ₹3,146 Cr

- Previous Year (Q4 FY25): ₹2,982 Cr

- PAT (Q4 FY26): ₹3,173 Cr

- QoQ Performance

- Revenue Trend: Stable Growth

- Profit Trend: Slight improvement

Margin Analysis

Key Drivers:

- Increase in interest income driven by advances growth

- Slight rise in operating expenses

- Elevated provisioning impact

- Stable yield environment

Key Signal: Margins remain stable but under mild pressure due to provisioning and cost expansion

Segment performance

Segment: Treasury Operations

- Revenue: ₹4,598.46 Cr

- Slight QoQ decline but YoY growth maintained

Segment: Corporate / Wholesale Banking

- Revenue: ₹6,680.38 Cr

- Strong contributor with steady expansion

Segment: Retail Banking

- Revenue: ₹8,265.20 Cr

- Largest segment; consistent growth driver

Segment: Other Banking Operations

- Revenue: ₹717.19 Cr

- Volatile but improving

Segment insight

Summary:

- Retail banking dominates revenue contribution, while corporate banking provides stability. Treasury operations remain cyclical.

Characteristics:

- Retail-led growth strategy

- Diversified revenue streams

- Increasing digital banking contribution

- Balanced domestic and foreign exposure

Earning quality check

Drivers:

- Core income growth from advances

- Controlled NPAs

- Stable other income

- Provisioning normalization vs last year

Interpretation:

- Earnings quality is strong and sustainable, driven by core banking operations rather than one-offs

balance sheet Analysis

- Total Assets: ₹9,91,552.79 Cr

- Total Liabilities: ₹9,91,552.79 Cr

Insight:

- Strong balance sheet expansion driven by advances and deposits growth indicates healthy credit demand and liquidity position.

key risks

- Rising operating expenses

- Interest rate volatility impacting margins

- Slower treasury performance

- Credit cost fluctuations

management strategy signals

Focus Area:

- Retail and digital banking expansion

- Strengthening asset quality

- Deposit mobilization

- Cost efficiency initiatives

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹20,261.23 Crore | +1.84% | +7.81% |

| Operating Profit | ₹5,305.81 Crore | +4.93% | +5.61% |

| PAT | ₹3,173.05 Crore | +0.83% | +6.42% |

Indian Bank delivered a well-balanced performance in Q4 FY26 with:

- Strong balance sheet expansion

- Stable profitability growth

- Improving asset quality (GNPA: 1.98% vs 3.09% YoY)

- Controlled risk profile

Official Exchange Filing: Indian Bank Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

23%

NET PROFIT AS % OF REVENUE

15.66%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED