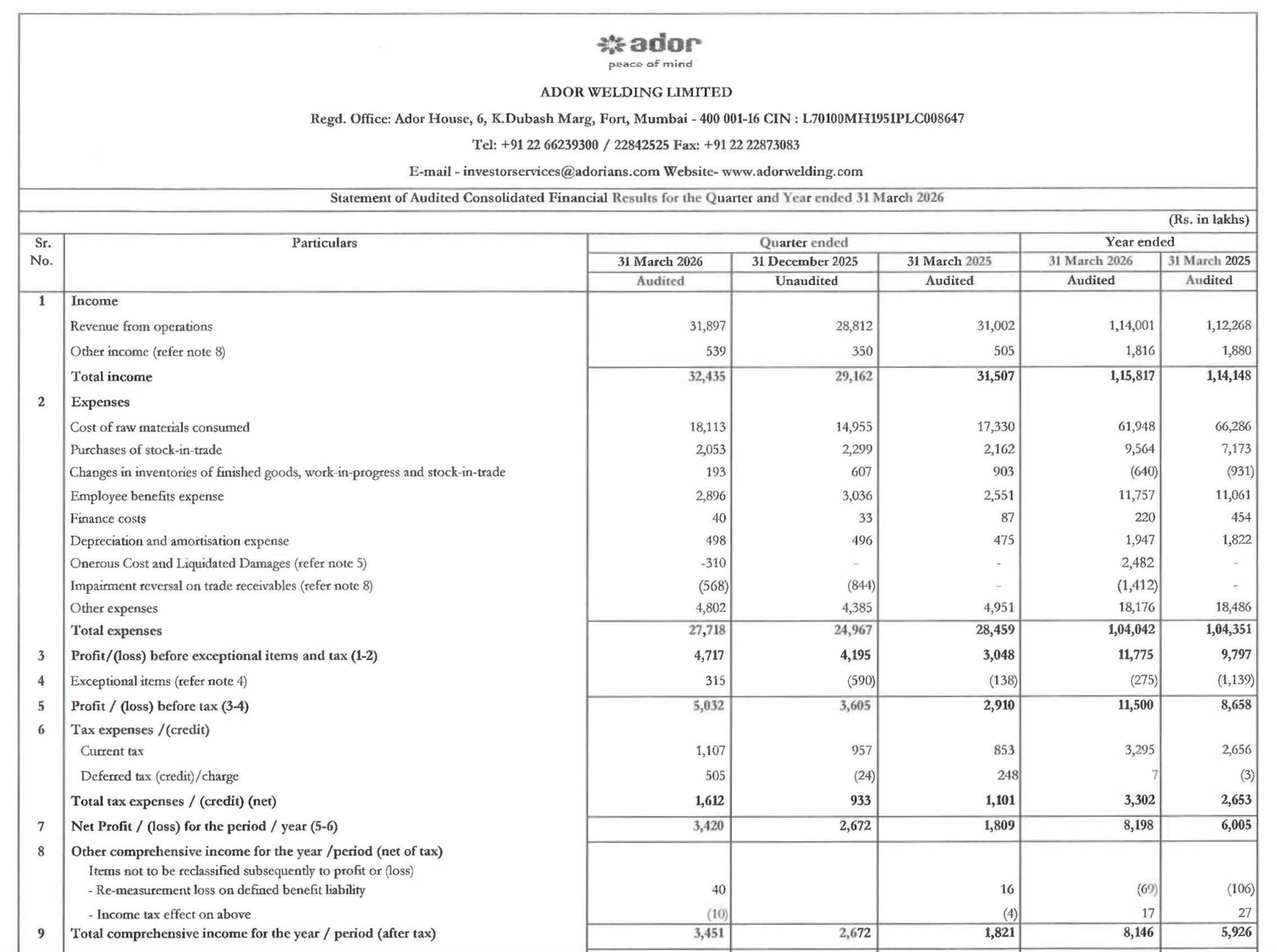

Quarter Ended: March 2026

Ador Welding Limited – Q4 FY26 Results

NSE

adorweld

BSE

517041

Core welding business remains strong with stable profitability, but rising working capital and investing outflows signal expansion phase pressure.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹317.96 Cr

- QoQ Change: +10.8%

- YoY Change: +3.9%

- Previous Quarter (Q3 FY26): ₹286.95 Cr

- Previous Year (Q4 FY25): ₹307.99 Cr

- Revenue (Q4 FY26): ₹317.96 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹34.20 Cr

- QoQ Change: +28%

- YoY Change: +89%

- Previous Quarter (Q3 FY26): ₹26.72 Cr

- Previous Year (Q4 FY25): ₹18.09 Cr

- PAT (Q4 FY26): ₹34.20 Cr

- QoQ Performance

- Revenue Trend: Moderate growth

- Profit Trend: Strong improvement

Margin Analysis

Key Drivers:

- Improved operating leverage

- Lower raw material pressure

- Controlled employee and other expenses

- Impairment reversal support

Key Signal: Margins are stable to improving, indicating operational efficiency

Segment performance

Segment: Welding Segment

- Revenue: ₹305.66 Cr

- Insights:

- Dominant revenue contributor

- Stable growth trajectory

- Strong profitability driver

Segment: Flares & Process Equipment

- Revenue: ₹12.33 Cr

- Insights:

- Smaller segment

- Volatile contribution

- Lower margin visibility

Segment insight

Summary:

- Business remains core manufacturing-driven, with welding segment providing consistent earnings and scale

Characteristics:

- High dependency on core welding segment

- Industrial demand-linked growth

- Limited diversification impact

Earning quality check

Drivers:

- Strong core operating profit (₹50.32 Cr PBT)

- Limited reliance on exceptional items

- Some support from impairment reversal

Interpretation:

- Earnings quality is high, driven largely by core operations rather than one-off gains

balance sheet Analysis

- Total Assets: ₹831.83 Cr

- Total Liabilities: ₹277.41 Cr

Insight:

- Strong equity base (₹554.45 Cr)

- Low debt profile → financially stable company

- Increase in current assets indicates working capital build-up

key risks

- Rising inventory and receivables

- Negative investing cash flow (capex heavy)

- Cyclicality of industrial demand

- Small segment underperformance

management strategy signals

Focus Area:

- Capacity expansion

- Working capital investment

- Strengthening core welding segment

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹324.35 Crore | +11.00% | +2.9% |

| PBT | ₹50.32 Crore | +39.00% | +73.00% |

| PAT | ₹34.20 Crore | +28.00% | +89.00% |

Ador Welding has delivered a solid and clean quarter, backed by strong core operations and margin expansion. While cash flow pressures and working capital increase are visible, they align with a growth phase rather than stress. Overall, the company reflects high-quality earnings with stable fundamentals, making it structurally strong in the industrial segment.

Official Exchange Filing: Ador Welding Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED