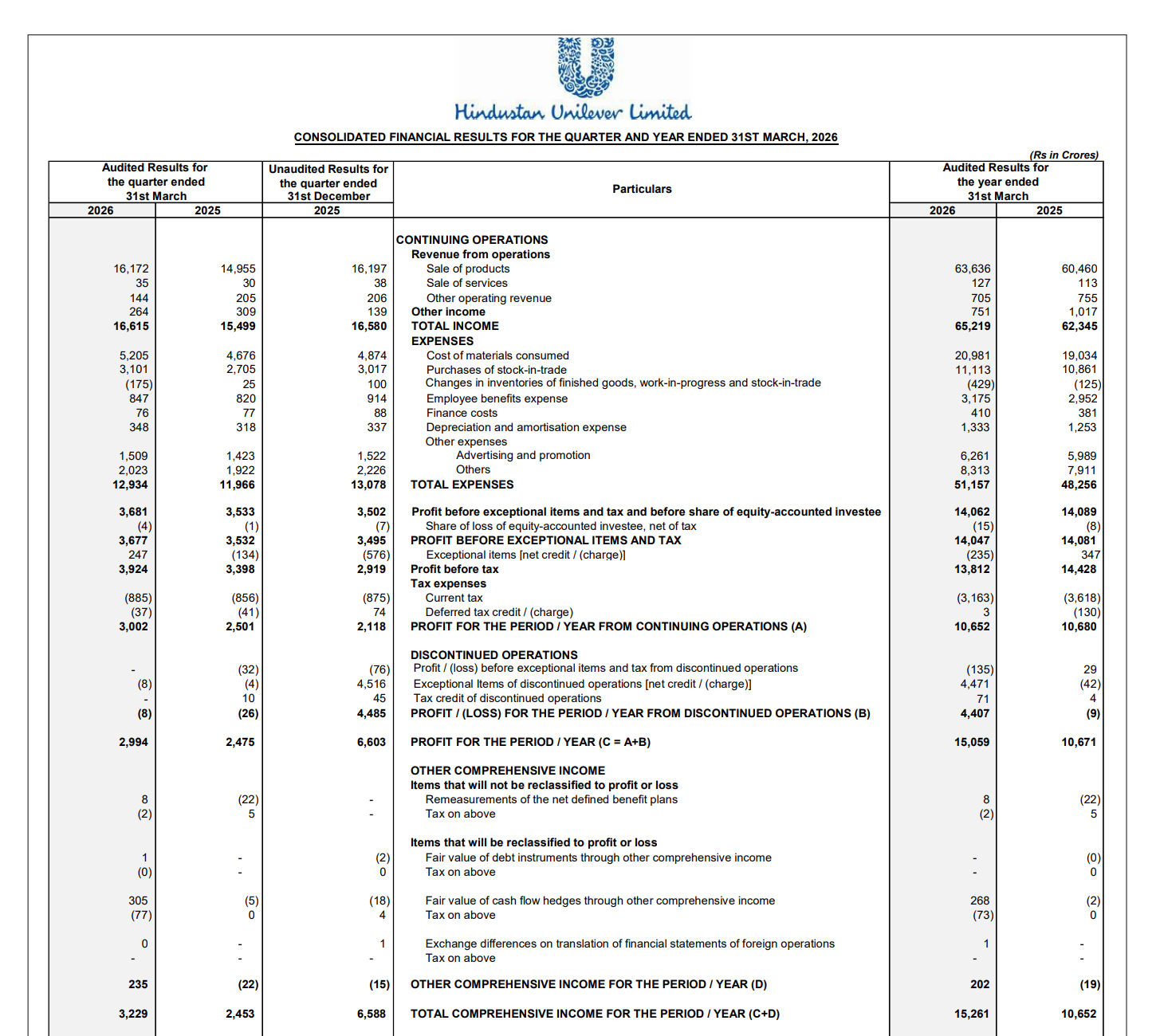

Quarter Ended: March 2026

Hindustan Unilever Limited – Q4 FY26 Results

NSE

hindunilvr

BSE

500696

Core business remains steady but muted, while reported profits are significantly supported by exceptional items (ice cream business demerger impact)

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹16,172 Cr

- QoQ Change: -0.15%

- YoY Change: +8.1%

- Previous Quarter (Q3 FY26): ₹16,197 Cr

- Previous Year (Q4 FY25): ₹14,955 Cr

- Revenue (Q4 FY26): ₹16,172 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,994 Cr

- QoQ Change: +41.4%

- YoY Change: +20.9%

- Previous Quarter (Q3 FY26): ₹2,118 Cr

- Previous Year (Q4 FY25): ₹2,475 Cr

- PAT (Q4 FY26): ₹2,994 Cr

- QoQ Performance

- Revenue Trend: Flat

- Profit Trend: Strong Increase

Margin Analysis

Key Drivers:

- Stable gross margins with controlled raw material costs

- Increased advertising & promotion expenses

- Exceptional gain from ice cream business demerger (~₹4,611 Cr impact at PBT level)

Key Signal: Underlying margins are stable, but headline profitability is distorted by one-offs

Segment performance

Segment: Home Care

- Revenue: ₹6,344 Cr

- Insights:

- Largest contributor

- Stable growth

Segment: Beauty & Wellbeing

- Revenue: ₹3,697 Cr

- Insights:

- Premiumization driving growth

- Margin supportive

Segment: Personal Care

- Revenue: ₹2,229 Cr

- Insights:

- Moderate growth

- Competitive segment

Segment: Foods

- Revenue: ₹3,566 Cr

- Insights:

- Strong demand resilience

- Consistent performer

Segment: Others (Exports)

- Revenue: ₹515 Cr

- Insights:

- Small but stable

Segment insight

Summary:

- HUL continues to operate as a diversified FMCG leader, with balanced contributions across segments

Characteristics:

- Defensive demand profile

- Strong brand portfolio

- Pricing power with gradual volume growth

Earning quality check

Drivers:

- Exceptional gain from demerger (~₹4,611 Cr)

- Core operating profit remains stable (~₹3,600–3,900 Cr range)

- Minimal reliance on fair value gains

Interpretation:

- Earnings quality is moderate, as headline profit is significantly influenced by one-time gains

balance sheet Analysis

- Total Assets: ₹79,752 Cr

- Total Liabilities: ₹30,744 Cr

Insight:

- Strong cash-rich balance sheet

- Low leverage

- Decline in cash balance YoY (₹6,071 Cr → ₹2,583 Cr) due to capital allocation

key risks

- Volume growth slowdown

- Rural demand weakness

- High competition in FMCG space

- Dependence on pricing for growth

management strategy signals

Focus Area:

- Premiumization

- Digital & distribution expansion

- Portfolio restructuring (demerger impact)

- Cost efficiency

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹16,615 Crore | +0.2% | +7.2% |

| PBT | ₹3,812 Crore | -29.7% | -4.3% |

| PAT | ₹2,994 Crore | +41.4% | +20.9% |

HUL delivered a stable operational quarter, but headline profit growth is misleading due to exceptional gains. The core business remains steady but lacks strong volume momentum. The company continues to be a defensive compounder, but near-term upside depends on demand revival rather than financial engineering

Official Exchange Filing: Hindustan Unilever Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED