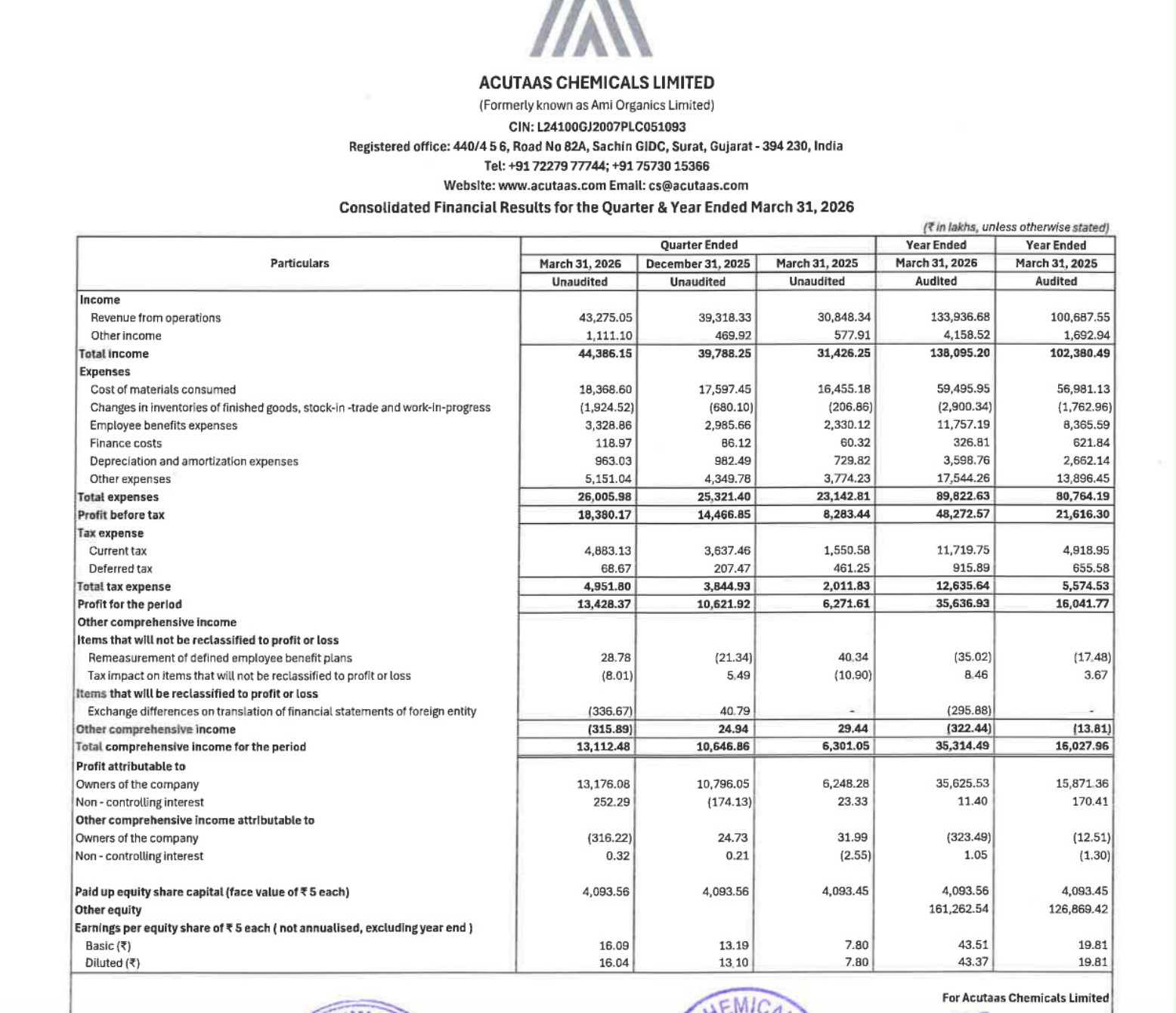

Quarter Ended: March 2026

Acutaas Chemicals Limited (Formerly Ami Organics) – Q4 FY26 Results

NSE

acutaas

BSE

543349

Acutaas delivered a sharp improvement in profitability and operating cash flows, indicating strong execution, though heavy capex and working capital absorption remain key themes.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹43,275 Cr

- QoQ Change: +10.1%

- YoY Change: +40.3%

- Previous Quarter (Q3 FY26): ₹39,318 Cr

- Previous Year (Q4 FY25): ₹30,848 Cr

- Revenue (Q4 FY26): ₹43,275 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹13,428 Cr

- QoQ Change: +26.4%

- YoY Change: +114%

- Previous Quarter (Q3 FY26): ₹10,622 Cr

- Previous Year (Q4 FY25): ₹6,271 Cr

- PAT (Q4 FY26): ₹13,428 Cr

- QoQ Performance

- Revenue Trend: Strong Growth

- Profit Trend: Strong expansion

Margin Analysis

Key Drivers:

- Operating leverage improvement

- Better cost absorption despite rising employee and other expenses

- Lower finance cost impact YoY

- Improved realization / product mix

Key Signal: Margins are expanding both QoQ and YoY, indicating strong pricing power + operating efficiency

Segment insight

Summary:

- Acutaas operates in specialty chemicals & pharma intermediates, a high-margin, export-oriented segment.

Characteristics:

- High entry barriers

- Strong client stickiness

- Export-driven revenue

- Capex-heavy expansion phase

Earning quality check

Drivers:

- Operating cash flow increased sharply to ₹29,217 Cr (vs ₹11,834 Cr YoY)

- Profit backed by real cash generation

- Minimal reliance on exceptional items

Interpretation:

- Earnings quality is very strong, supported by:

- High cash conversion

- Sustainable core business growth

balance sheet Analysis

- Total Assets: ₹1,98,396 Cr

- Total Liabilities: ₹27,321 Cr

- Total Equity: ₹1,71,075 Cr

Insight:

- Strong equity base expansion (retained earnings)

- Moderate increase in borrowings (₹2,649 Cr)

- High capex reflected in PPE jump (~₹58,279 Cr)

key risks

- Heavy capex → execution risk

- Working capital pressure (inventory & receivables increase)

- Chemical sector cyclicality

- Export demand dependency

management strategy signals

Focus Area:

- Capacity expansion (capex heavy phase)

- Specialty chemical scaling

- Export market penetration

- Product diversification

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹44,386 Crore | +11.6% | +41.4% |

| PBT | ₹18,380 Crore | +27.1% | +121.0% |

| PAT | ₹13,428 Crore | +26.4% | +114.0% |

Acutaas Chemicals delivered a breakout performance, with:

- Strong revenue growth

- Significant margin expansion

- Excellent cash flow generation

Official Exchange Filing: Acutaas Chemicals Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

60%

NET PROFIT AS % OF REVENUE

31%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED