Capex Expansion / Backward Integration

Tata Power Enters PV Ingot & Wafer Manufacturing with ₹6,500 Crore Investment Plan

NSE

tatapower

BSE

500400

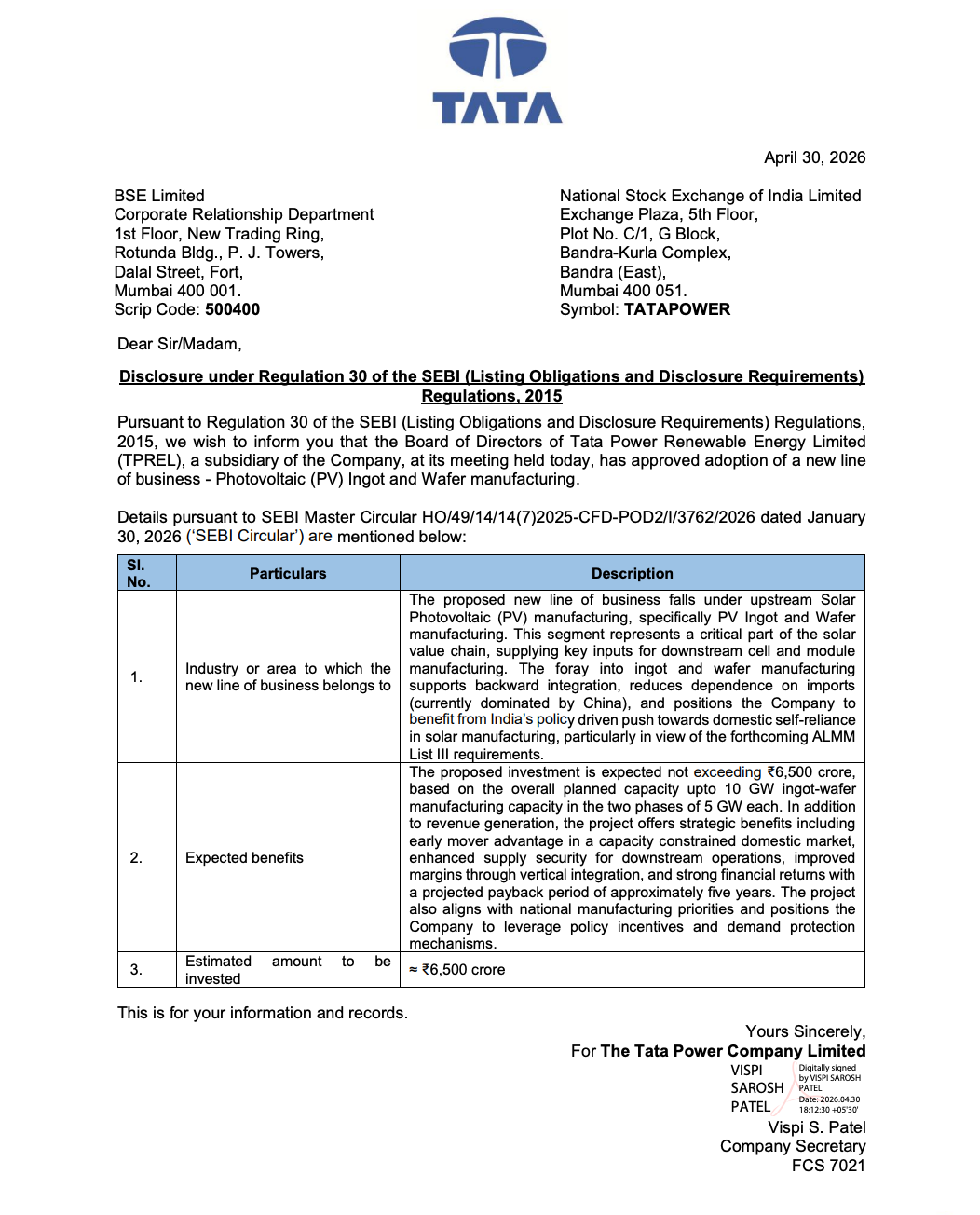

Tata Power’s subsidiary Tata Power Renewable Energy Limited (TPREL) has approved entry into upstream solar manufacturing—PV ingots and wafers—with an investment of up to ₹6,500 crore, strengthening backward integration in the solar value chain

PRICE-SENSITIVE TRIGGER

Event: New Business Line Approval

Type: Capex Expansion / Backward Integration

Impact: Positive

Immediate Effect: Enhances long-term strategic positioning in solar manufacturing and reduces dependency on imports, though near-term earnings impact will be limited

Key Metrics:

- Planned Investment: ₹6,500 crore

- Capacity Target: Up to 10 GW (in two phases of 5 GW each)

- Payback Period: ~5 years (estimated)

Highlight:

- Strategic Shift: Entry into upstream solar manufacturing (ingots & wafers)

What Happened ?

The Board of Tata Power Renewable Energy Limited (TPREL), a subsidiary of Tata Power, has approved the adoption of a new business line focused on manufacturing photovoltaic (PV) ingots and wafers—key upstream components in the solar value chain.

This marks a strategic move toward backward integration and aligns with India’s push for self-reliance in solar manufacturing.

key highlights

New Business Segment:

- Entry into upstream solar manufacturing

- Focus on:

- PV Ingots

- PV Wafers

- Critical inputs for solar cells and modules

Capacity & Investment Plan:

- Total planned capacity: 10 GW

- Execution in 2 phases (5 GW each)

- Investment capped at ₹6,500 crore

Strategic Benefits:

- Enables backward integration in solar value chain

- Reduces reliance on imports (especially China)

- Improves supply chain security

- Enhances margins through vertical integration

- Positions company for ALMM (Approved List of Models & Manufacturers) benefits

Policy Alignment:

- Supports India’s self-reliance (Atmanirbhar Bharat) initiative

- Leverages government incentives and protection mechanisms

- Aligns with domestic solar manufacturing push

Financial & Operational Impact:

- Early mover advantage in capacity-constrained domestic market

- Expected strong financial returns

- Estimated payback period ~5 years

- Improves long-term profitability profile

Note:

Near-term impact may include higher capex and execution risks

Risk Analysis

Key Risks

- High capital expenditure (₹6,500 crore)

- Technology and execution risks in new segment

- Global price volatility in solar value chain

- Competition from established global players

- Policy dependency (subsidies, ALMM protection)

Worst Case Scenario

- If global prices fall or execution delays occur, returns could be lower than expected, impacting ROCE

Risk Level: Medium

Company Commentary

- Entry into ingot & wafer manufacturing supports backward integration

- Reduces import dependency

- Aligns with national manufacturing priorities

- Expected to generate strong financial returns

- Enhances supply chain security and operational efficiency

Official Exchange Filing: Tata Power Renewable Energy Limited