Quarter Ended: March 2026

Central Bank of India – Q4 FY26 Results

NSE

centralbk

BSE

532885

YoY performance strong, but QoQ decline in profitability and margins needs attention

key financial highlights

- Revenue from Operations:

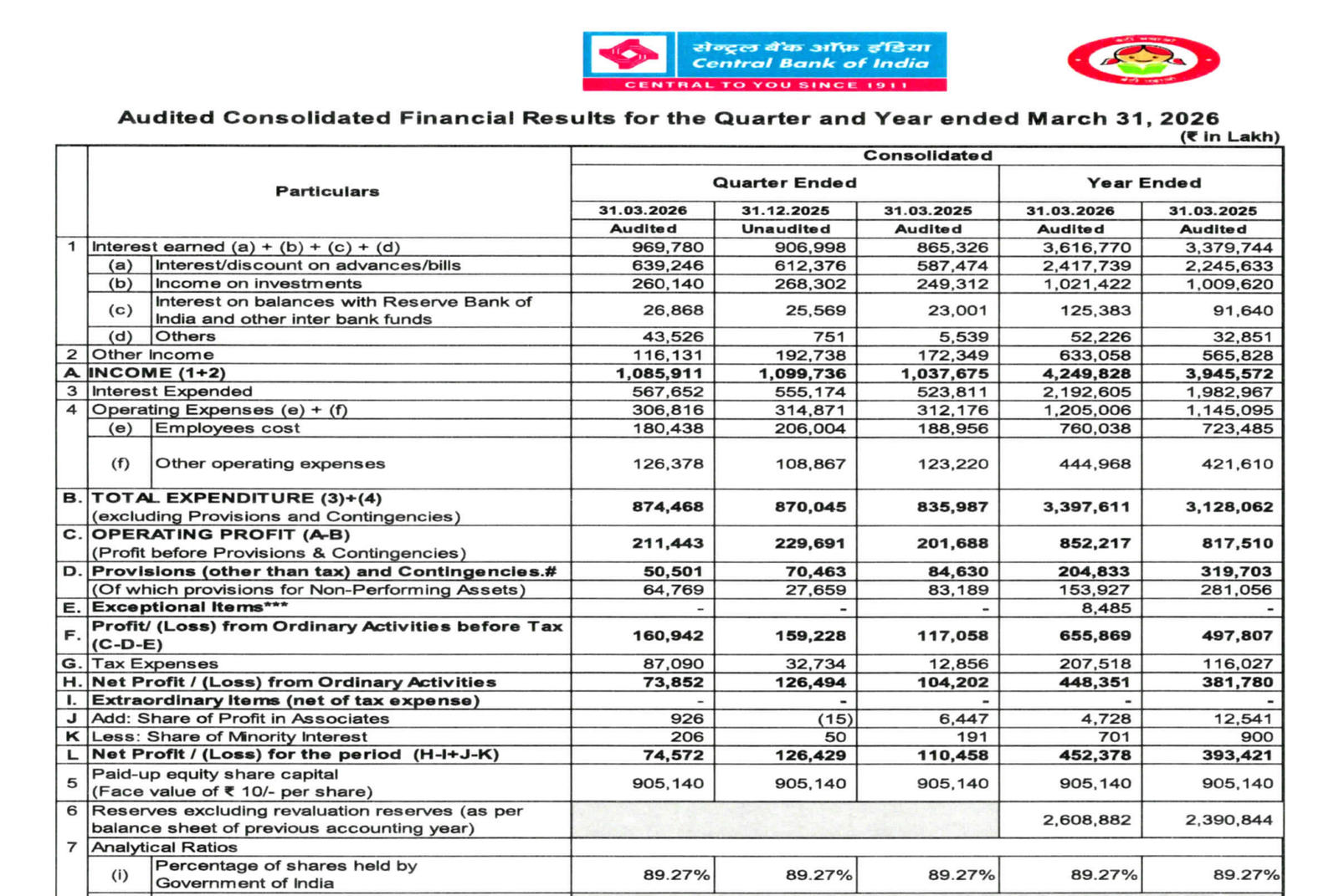

- Total Income (Q4 FY26): ₹10,85,911 Lakhs

- QoQ Change: -1.26%

- YoY Change: +4.65%

- Previous Quarter (Q3 FY26): ₹10,99,736 Lakhs

- Previous Year (Q4 FY25): ₹10,37,675 Lakhs

- Total Income (Q4 FY26): ₹10,85,911 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹74,572 Lakhs

- QoQ Change: -41.01%

- YoY Change: -32.49%

- Previous Quarter (Q3 FY26): ₹1,26,429 Lakhs

- Previous Year (Q4 FY25): ₹1,10,458 Lakhs

- PAT (Q4 FY26): ₹74,572 Lakhs

- QoQ Performance

- Revenue Trend: Slight Decline

- Profit Trend: Sharp Decline

Margin Analysis

Drivers:

- Higher provisions vs previous quarter

- Moderation in operating profit

- Stable cost structure

Insight:

- Margin compression QoQ → credit cost impact visible

Segment performance

Revenue Mix (FY26)

- Retail Banking: ₹18,60,238 Lakhs

- Treasury Operations: ₹13,55,683 Lakhs

- Wholesale Banking: ₹9,83,145 Lakhs

Observation

- Retail banking is the largest contributor (~44%)

- Treasury remains significant earnings driver

Segment insight

Key Insight:

- Balanced mix of Retail + Treasury + Corporate banking

Business Nature:

- PSU bank → interest income driven

- Sensitive to:

- Interest rate cycles

- Asset quality (NPAs)

Earning quality check

Drivers:

- Core income stable

- Profit impacted by provisioning swings

Interpretations:

- Earnings quality is moderate, dependent on credit cost normalization

balance sheet Analysis

Key Numbers:

- Total Assets: ₹55,10,791 Cr

- Capital Employed: ₹3,90,011 Cr

Asset Quality:

- Gross NPA: ₹9,25,851 Lakhs

- Net NPA: ₹1,70,828 Lakhs

Ratios:

- Gross NPA %: 2.67%

- Net NPA %: 0.50%

Insight:

- Asset quality improving vs past years

- Still provisioning-sensitive

Cash flow analysis

Operating Cash Flow: ₹2,803.98 Cr

Investing Cash Flow: ₹453.86 Cr

Financing Cash Flow: (₹712.82 Cr)

Insight:

- Positive operating cash flow (good sign)

- Dividend payout impacting financing

key risks

- High sensitivity to provisioning cycles

- PSU bank → policy & governance influence

- Interest rate volatility

- NPA slippages

management strategy signals

Focus Area:

- Strengthening retail loan book

- Improving asset quality

- Controlled credit growth

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹10,859 Cr | -1.26% | +4.65% |

| Operating Profit | ₹2,114 Cr | -7.95% | +4.83% |

| PAT | ₹745.72 Cr | -41.01% | -32.49% |

Central Bank delivered stable revenue but weak profitability this quarter, primarily due to higher provisioning impact. Long-term story intact with improving asset quality, but short-term momentum is weak

Official Exchange Filing: Central Bank of India

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED