Quarter Ended: March 2026

NDR Auto Components Limited – Q4 FY26 Results

NSE

ndrauto

BSE

543214

NDR Auto Components reported strong double-digit revenue and profit growth in Q4 FY26, supported by operational expansion and associate income contribution, while operating cash flow weakened sharply due to working capital pressure.

key financial highlights

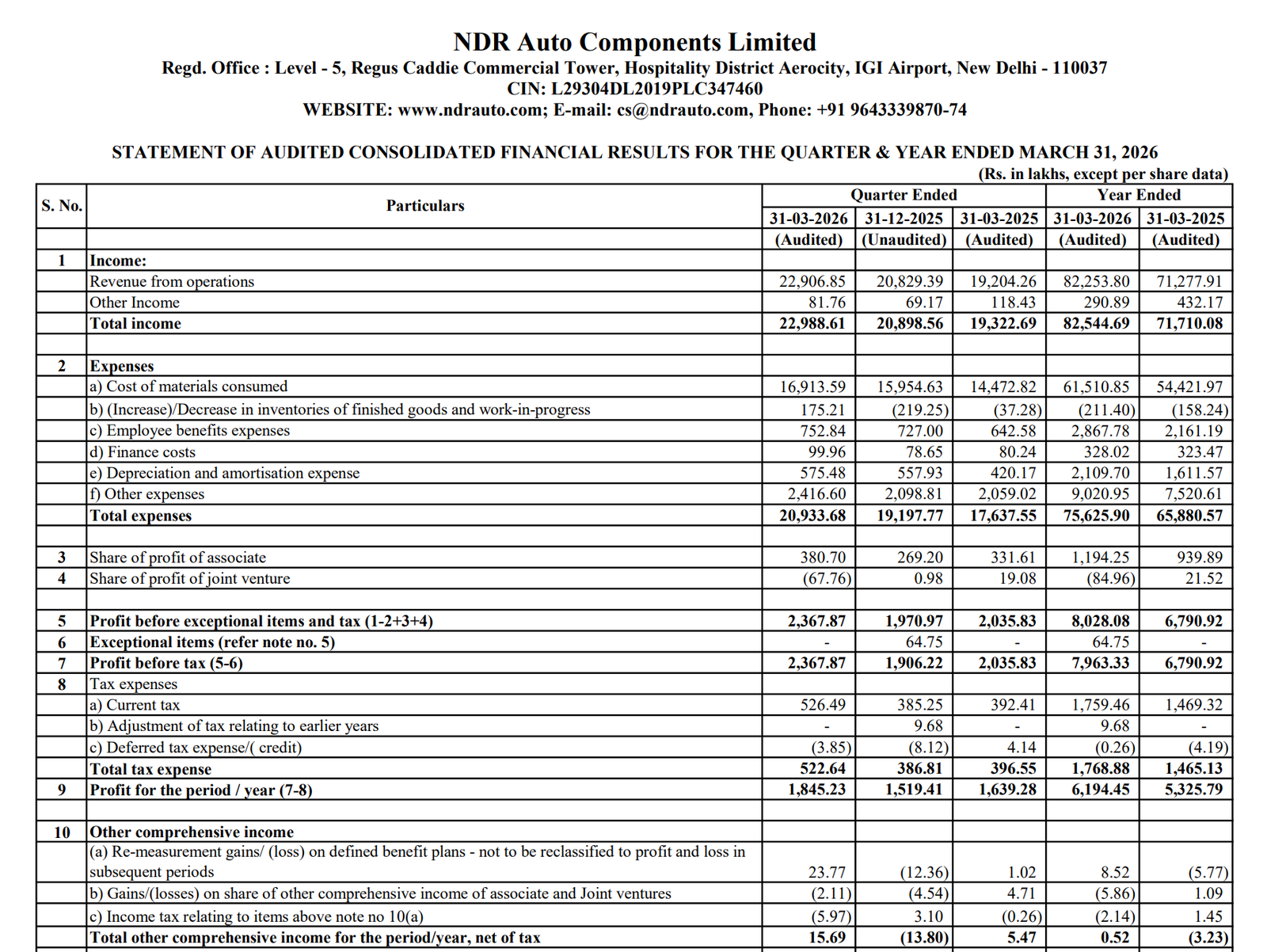

- Revenue from Operations:

- Revenue (Q4 FY26): ₹22,906.85 Lakhs

- QoQ Change: +10.94%

- YoY Change: +19.28%

- Previous Quarter (Q3 FY26): ₹20,829.39 Lakhs

- Previous Year (Q4 FY25): ₹19,204.26 Lakhs

- Revenue (Q4 FY26): ₹22,906.85 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹1,845.23 Lakhs

- QoQ Change: +21.44%

- YoY Change: +12.56%

- Previous Quarter (Q3 FY26): ₹1,519.41 Lakhs

- Previous Year (Q4 FY25): ₹1,639.28 Lakhs

- PAT (Q4 FY26): ₹1,845.23 Lakhs

- QoQ Performance:

- Revenue Trend: Revenue improved sequentially because of stronger operational execution and higher business activity during Q4 FY26.

- Profit Trend: Profit growth outpaced revenue growth on a QoQ basis, indicating improved earnings efficiency during the quarter.

- Revenue Trend: Revenue improved sequentially because of stronger operational execution and higher business activity during Q4 FY26.

Margin Analysis

Drivers:

- Cost of materials consumed increased to ₹16,913.59 Lakhs during Q4 FY26.

- Employee benefit expenses remained relatively controlled compared to revenue growth.

- Depreciation and amortisation expenses increased because of expansion in fixed assets and right-of-use assets.

- Associate income positively supported overall profitability.

- Finance costs remained manageable despite higher lease liabilities.

Insight:

- The company maintained stable profitability despite elevated material and depreciation expenses, reflecting reasonable operational efficiency.

Earning quality check

Key Drivers:

- Revenue growth remained supported by operational business expansion.

- Share of profit from associates contributed ₹380.70 Lakhs during Q4 FY26.

- Other comprehensive income remained positive.

- Operating cash flow turned negative due to working capital stress.

- Trade receivables and other financial assets increased significantly.

Interpretations:

- Accounting profitability remained healthy, but weak operating cash flow indicates elevated working capital pressure and slower cash conversion efficiency.

balance sheet Analysis

- Total Assets: ₹56,301.97 Lakhs

- Total Equity: ₹35,771.87 Lakhs

- Total Current Liabilities: ₹14,819.57 Lakhs

- Total Non-Current Liabilities: ₹5,710.53 Lakhs

Insight:

- The company significantly expanded its asset base during FY26 through investments in property, right-of-use assets and equity-accounted investments. Equity also strengthened materially due to retained earnings growth.

key risks

- Operating cash flow turned negative during FY26.

- Trade receivables increased substantially, impacting liquidity.

- Higher lease liabilities increased fixed financial commitments.

- Working capital requirements remain elevated.

- Dependence on associate and joint venture contribution may increase earnings volatility.

management strategy signals

Focus Area:

- Expansion of manufacturing and operational assets.

- Scaling associate and joint venture participation.

- Strengthening long-term business growth.

- Managing working capital and receivable cycles.

- Enhancing operational efficiency.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹22,988.61 Lakhs | +10.00% | +18.97% |

| PBT | ₹2,367.87 Lakhs | +24.22% | +16.31% |

| PAT | ₹1,845.23 Lakhs | +21.44% | +12.56% |

NDR Auto Components delivered a strong operational and earnings performance during Q4 FY26 with healthy double-digit growth in revenue and profitability. The balance sheet expanded meaningfully and equity strengthened substantially.

However, weak operating cash flow and rising working capital intensity remain important monitoring factors. Overall, the results indicate solid business growth momentum but with emerging liquidity and cash conversion concerns.

Official Exchange Filing: NDR Auto Components Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED