Quarter Ended: March 2026

Ethos Limited – Q4 FY26 Results

NSE

ethosltd

BSE

543532

Ethos Limited reported strong revenue growth in FY26 driven by premium luxury watch demand expansion, but profitability remained largely flat due to higher operating costs, inventory investments, and increased depreciation and finance expenses.

key financial highlights

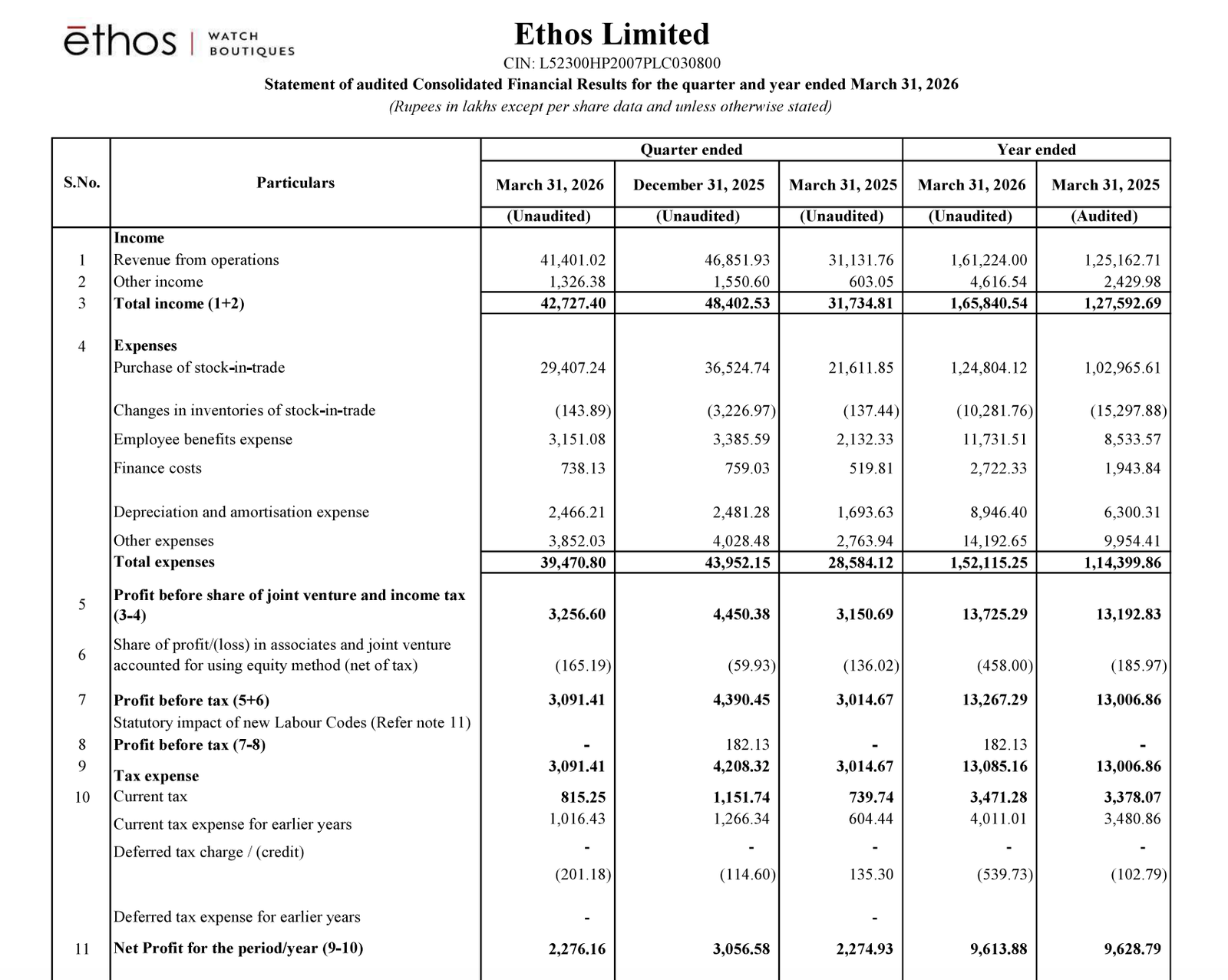

- Revenue from Operations:

- Revenue (Q4 FY26): ₹41,401.02 Lakhs

- QoQ Change: -11.63%

- YoY Change: +32.99%

- Previous Quarter (Q3 FY26): ₹46,851.93 Lakhs

- Previous Year (Q4 FY25): ₹31,131.76 Lakhs

- Revenue (Q4 FY26): ₹41,401.02 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,276.16 Lakhs

- QoQ Change: -25.53%

- YoY Change: +0.05%

- Previous Quarter (Q3 FY26): ₹3,056.58 Lakhs

- Previous Year (Q4 FY25): ₹2,274.93 Lakhs

- PAT (Q4 FY26): ₹2,276.16 Lakhs

- Analysis:

- Revenue: Revenue grew strongly on a YoY basis due to continued demand for luxury watches and boutique expansion, although quarterly revenue softened sequentially after a strong festive and wedding-driven previous quarter.

- Profit: Despite strong revenue growth, profitability remained flat YoY due to higher employee costs, finance expenses, depreciation, and operating investments.

- Revenue: Revenue grew strongly on a YoY basis due to continued demand for luxury watches and boutique expansion, although quarterly revenue softened sequentially after a strong festive and wedding-driven previous quarter.

Margin Analysis

Drivers:

- Higher employee benefit expenses

- Significant increase in depreciation and amortization

- Elevated finance costs

- Expansion-related operational expenses

- Inventory carrying costs

- Store network expansion impact

Insight:

- The business is prioritizing growth and scale expansion over near-term margin optimization.

Segment insight

Business Summary:

Ethos operates in the organized luxury and premium watch retail segment with a portfolio of international watch brands across India.

Key Characteristics:

- Premium discretionary retail business

- Multi-brand luxury watch retail platform

- Strong presence in affluent urban markets

- Inventory-intensive business model

- Expansion through premium boutiques and experiential retail

Earning quality check

Key Drivers:

- Operating cash flow improved sharply to ₹8,959.53 Lakhs from negative ₹2,028.65 Lakhs.

- Large inventory buildup continued.

- Trade payable growth supported working capital funding.

- Significant investment in fixed deposits reduced investing cash flows.

- Equity issuance strengthened liquidity and balance sheet position.

- Cash balance increased substantially to ₹14,407.94 Lakhs.

Interpretations:

- Cash flow quality improved materially in FY26 despite aggressive inventory and expansion investments.

balance sheet Analysis

- Total Assets: ₹2,19,719.32 Lakhs

- Total Liabilities: ₹53,280.95 Lakhs

Insight:

- The company maintains a relatively healthy balance sheet with strong equity capitalization and limited leverage.

Key Observations:

- Total assets expanded sharply by over 55%.

- Inventory increased significantly to ₹69,548.82 Lakhs.

- Cash and bank balances rose strongly.

- Equity base expanded substantially after capital raising.

- Borrowings remained very low, indicating strong financial stability.

key risks

- Slowdown in discretionary luxury spending

- Inventory obsolescence risk

- Dependence on imported luxury brands

- Currency fluctuation exposure

- Rising operating costs

- Premium retail demand sensitivity

management strategy signals

Focus Area:

- Boutique network expansion

- Premium brand partnerships

- Inventory strengthening

- Digital luxury retail ecosystem

- Omnichannel customer engagement

- Premium customer acquisition

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹42,727.40 Lakhs | -11.77% | +34.63% |

| PBT | ₹3,091.41 Lakhs | -26.39% | +2.55% |

| PAT | ₹2,276.16 Lakhs | -25.53% | +0.05% |

Ethos Limited continues to demonstrate strong growth momentum in India’s premium luxury retail segment.

The company delivered healthy revenue growth, strengthened its balance sheet, improved operating cash flows, and expanded liquidity during FY26.

However, profitability growth remained muted due to higher expansion costs, inventory investments, and rising operational expenses.

The long-term outlook remains favorable provided luxury demand sustains and operating leverage improves as store expansion matures.

Official Exchange Filing: Ethos Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED