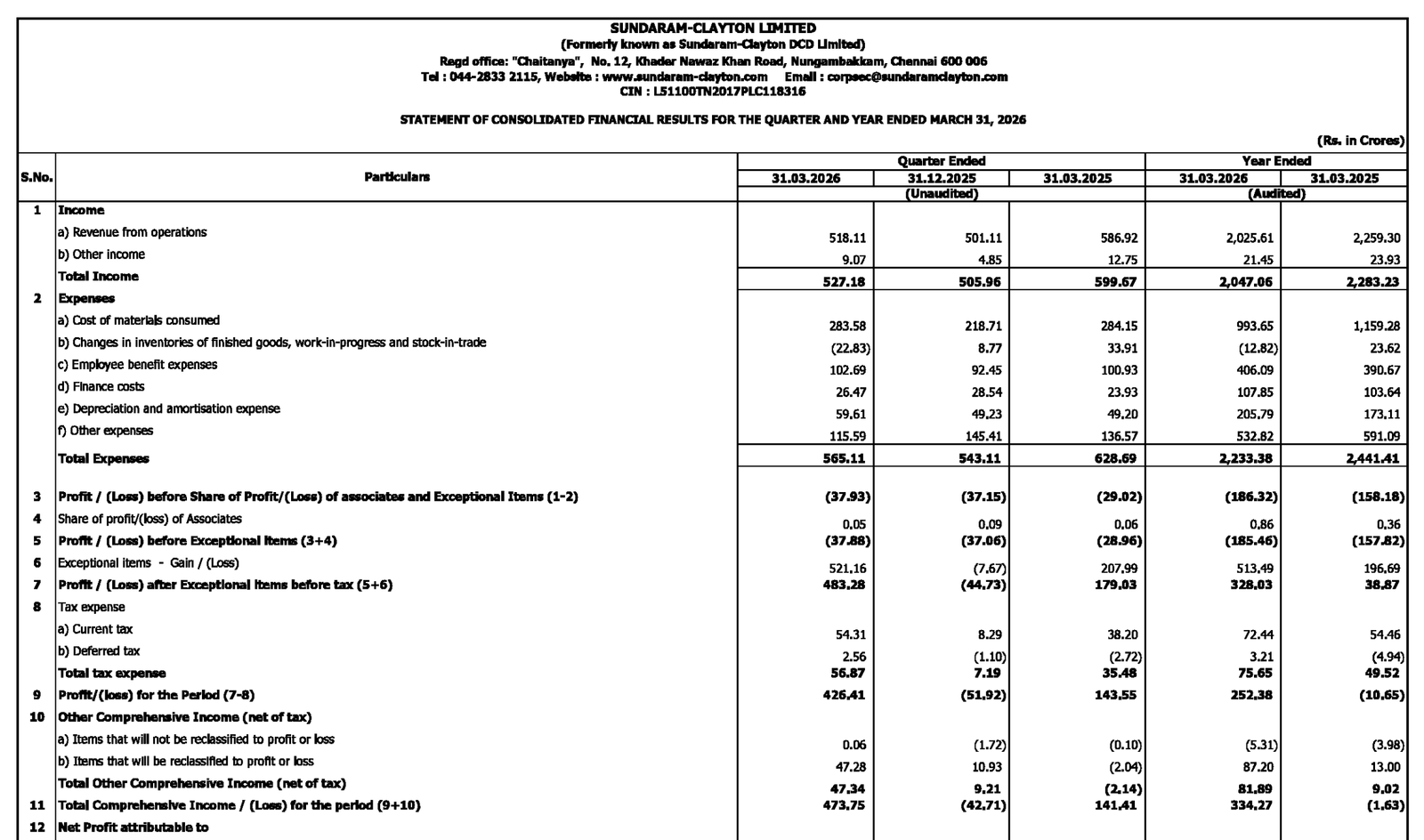

Quarter Ended: March 2026

Sundaram-Clayton Limited – Q4 FY26 Results

NSE

sunclay

BSE

544066

Sundaram-Clayton reported a sharp turnaround in Q4 FY26 profitability aided by exceptional gains despite revenue decline and pressure on operating profitability.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹518.11 Cr

- QoQ Change: +3.39%

- YoY Change: -11.72%

- Previous Quarter (Q3 FY26): ₹501.11 Cr

- Previous Year (Q4 FY25): ₹586.92 Cr

- Revenue (Q4 FY26): ₹518.11 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹426.41 Cr

- QoQ Change: Turnaround

- YoY Change: +197.05%

- Previous Quarter (Q3 FY26): – ₹51.92 Cr Loss

- Previous Year (Q4 FY25): ₹143.55 Cr

- PAT (Q4 FY26): ₹426.41 Cr

Margin Analysis

Drivers:

- Exceptional gain of ₹521.16 crore significantly boosted profitability.

- Revenue from operations declined on a YoY basis.

- Employee benefit and other operating expenses remained elevated.

- Finance costs and depreciation increased moderately.

- Inventory adjustments supported quarterly cost structure.

Insight:

- Reported earnings were heavily influenced by non-operational exceptional gains rather than core business expansion.

Earning quality check

Key Drivers:

- Strong reported PAT primarily due to exceptional item gains.

- Operating loss before exceptional items persisted.

- Operating cash flow remained negative.

- Investing activities generated substantial inflow through asset sales.

- Debt repayment and financing outflows continued.

Interpretations:

- Reported profitability quality remains weak as earnings were largely non-recurring and core operational profitability stayed negative.

balance sheet Analysis

- Total Assets: ₹3,281.77 crore

- Total Liabilities: ₹1,986.37 crore

Insight:

- Balance sheet strengthened with higher equity base and lower total liabilities, supported by profit accretion and reduction in borrowings.

key risks

- Core operating business remains loss-making before exceptional gains.

- Revenue contraction indicates demand pressure.

- Negative operating cash flow remains a concern.

- Dependence on non-recurring gains can impact earnings sustainability.

- Automotive sector cyclicality may affect future growth.

management strategy signals

Focus Area:

- Asset optimization initiatives.

- Debt reduction and balance sheet strengthening.

- Operational restructuring.

- Improving manufacturing efficiency.

- Enhancing profitability in core operations.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹527.18 Cr | +4.19% | +19.28% |

| PBT Before Exceptional Items | -₹37.88 Cr | Improvement | Improvement |

| PAT | ₹426.41 Cr | Turnaround | +197.05% |

Sundaram-Clayton delivered a headline strong Q4 FY26 result due to exceptional gains, resulting in sharp profit expansion and stronger equity position.

However, underlying operational performance remained weak with declining revenue, operating losses before exceptional items, and negative operating cash flows. Investors may closely monitor whether the company can restore sustainable profitability in its core business operations going forward.

Official Exchange Filing: Sundaram-Clayton Limited

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED