Quarterly & Annual Financial Results

Fujiyama Power Systems Reports Strong Q4 FY26 & FY26 Results with Revenue Growth of 87.5% YoY in Q4

NSE

UTLSOLAR

BSE

544613

Fujiyama Power Systems Limited announced its audited annual financial results and limited reviewed quarterly results for the period ended March 31, 2026. The company reported strong growth across revenue, EBITDA, and PAT, supported by expansion in distribution reach, increased manufacturing capacity, and growing demand for rooftop solar solutions.

PRICE-SENSITIVE TRIGGER

Event: Announcement of audited FY26 annual results and Q4 FY26 quarterly performance.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong revenue and profitability growth, along with manufacturing expansion and channel network growth, may improve investor confidence and strengthen growth outlook for the company.

Key Metrics:

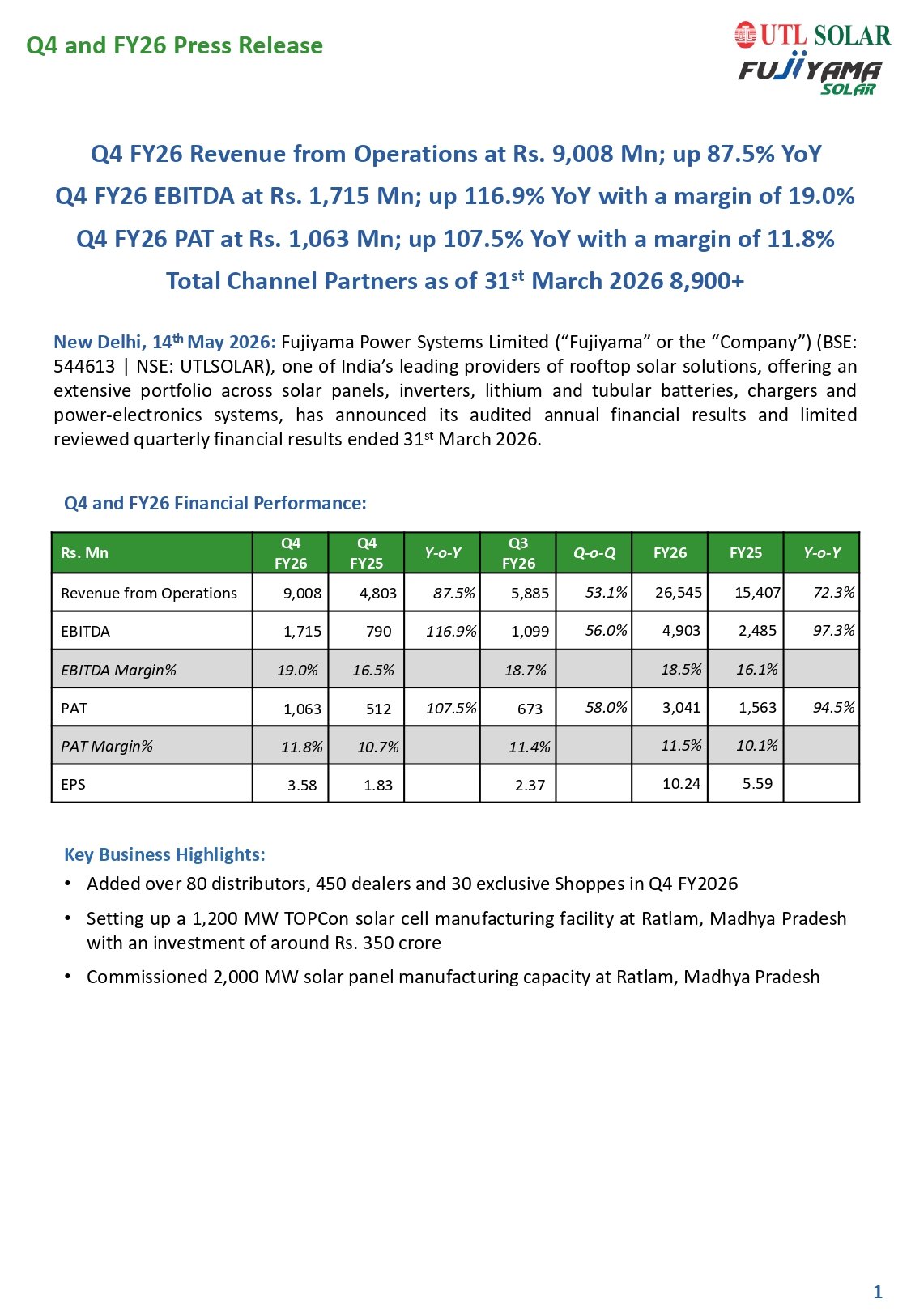

- Q4 FY26 Revenue from Operations: Rs. 9,008 Mn

- Q4 FY26 Revenue Growth YoY: 87.5%

- Q4 FY26 EBITDA: Rs. 1,715 Mn

- Q4 FY26 EBITDA Growth YoY: 116.9%

- Q4 FY26 EBITDA Margin: 19.0%

- Q4 FY26 PAT: Rs. 1,063 Mn

- Q4 FY26 PAT Growth YoY: 107.5%

- Q4 FY26 PAT Margin: 11.8%

- FY26 Revenue from Operations: Rs. 26,545 Mn

- FY26 Revenue Growth YoY: 72.3%

- FY26 EBITDA: Rs. 4,903 Mn

- FY26 EBITDA Growth YoY: 97.3%

- FY26 EBITDA Margin: 18.5%

- FY26 PAT: Rs. 3,041 Mn

- FY26 PAT Growth YoY: 94.5%

- FY26 EPS: 10.24

Highlight Metric:

- Q4 FY26 EBITDA Growth: 116.9% YoY

What Happened ?

Fujiyama Power Systems Limited released its Q4 FY26 and FY26 financial results, reporting strong operational and financial performance across all major metrics.

The company achieved Q4 FY26 revenue from operations of Rs. 9,008 million, representing an 87.5% year-on-year increase. EBITDA for the quarter rose 116.9% YoY to Rs. 1,715 million, while PAT increased 107.5% YoY to Rs. 1,063 million.

For the full financial year FY26, revenue from operations reached Rs. 26,545 million, growing 72.3% YoY. EBITDA stood at Rs. 4,903 million with margin improvement to 18.5%, while PAT rose to Rs. 3,041 million.

The company attributed growth to increasing adoption of rooftop solar solutions, expansion in Tier-2 and Tier-3 markets, stronger backward integration, and manufacturing scale-up initiatives.

Fujiyama also highlighted operational milestones including commissioning of 2,000 MW solar panel manufacturing capacity at Ratlam and ongoing development of a 1,200 MW TOPCon solar cell manufacturing facility.

key highlights

Key Announcement details:

- Added over 80 distributors, 450 dealers, and 30 exclusive shoppes during Q4 FY26.

- Total channel partner network crossed 8,900+ as of March 2026.

- Commissioned 2,000 MW solar panel manufacturing capacity at Ratlam, Madhya Pradesh.

- Setting up a 1,200 MW TOPCon solar cell manufacturing facility with planned investment of around Rs. 350 crore.

- Strong growth driven by rooftop solar demand in Tier-2 and Tier-3 cities.

- EBITDA margins improved due to higher operating scale and better manufacturing utilization.

- Company expects inverter manufacturing line commissioning by Q1FY27.

- Battery manufacturing commissioning expected by Q2FY27.

- Continued expansion of backward integration capabilities across solar value chain.

- Presence across four manufacturing facilities in Himachal Pradesh, Uttar Pradesh, Haryana, and Madhya Pradesh.

Note:

- Management stated that favourable government policies, increasing awareness regarding reliable power solutions, and DBT-linked residential solar schemes are expected to support long-term growth in the rooftop solar segment.

Risk Analysis

Key Risks:

- Delays in commissioning battery and power electronics capacities.

- Dependence on evolving government policies and subsidy schemes.

- Competitive pressure in rooftop solar and solar manufacturing industry.

- Supply chain and geopolitical risks impacting equipment procurement timelines.

- Technology transition risks related to lithium-ion battery and TOPCon manufacturing.

- Margin pressure possibility due to raw material price fluctuations.

Worst Case Scenario:

- Project execution delays, weakening solar demand, subsidy disruptions, or manufacturing inefficiencies could impact profitability, growth targets, and investor sentiment.

Risk Level: Medium

Company Commentary

- Management stated FY26 marked the company’s first full financial reporting year post IPO.

- The company highlighted strong growth in rooftop solar demand across India.

- Fujiyama aims to strengthen backward integration and manufacturing capabilities.

- Management remains optimistic about long-term solar sector demand supported by government initiatives.

- The company plans continued expansion in distribution network and operational efficiencies.

- Fujiyama emphasized its focus on delivering dependable and high-quality solar solutions.

Official Exchange Filing: Fujiyama Power Systems Ltd