Quarterly & Annual Financial Results

Symphony Reports Weak FY26 Performance Amid Australia Reset and Demand Pressure

NSE

symphony

BSE

517385

Symphony Limited announced its FY26 and Q4FY26 financial results, reporting pressure on revenues and margins across both standalone and consolidated businesses. The company also unveiled a strategic reset of its Australian operations and approved acquisitions aimed at simplifying ownership structures and strengthening global operations.

PRICE-SENSITIVE TRIGGER

Event: Announcement of FY26 financial results along with strategic business restructuring and acquisitions.

Type: Quarterly & Annual Financial Results

Impact: Negative

Immediate Effect: Revenue and profitability declined sharply due to weak domestic demand, inventory overhang, and continued pressure in Australian operations.

Key Metrics:

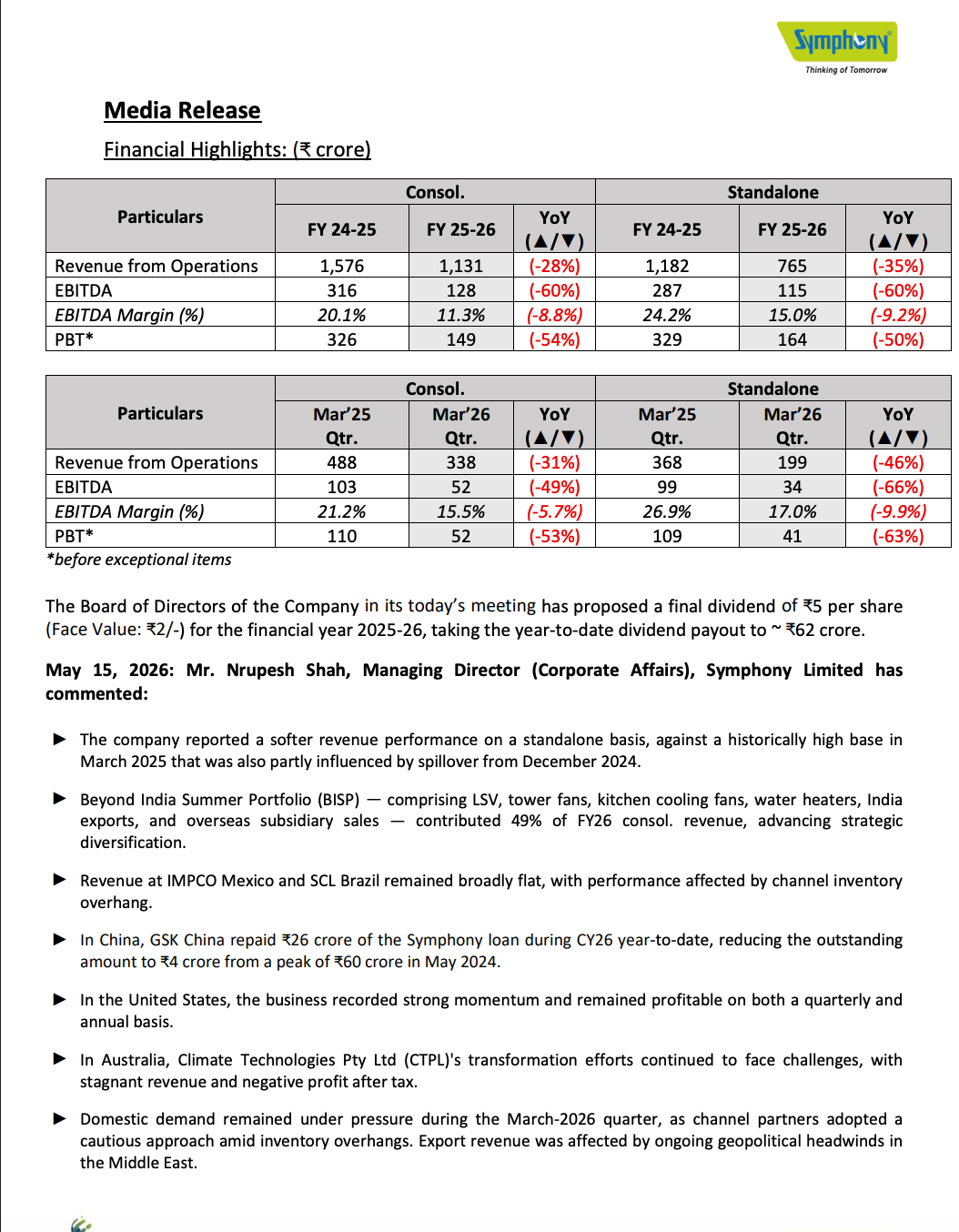

FY26 Consolidated Highlights:

- Revenue from operations declined to ₹1,131 crore, down 28% YoY

- EBITDA fell to ₹128 crore, down 60% YoY

- EBITDA margin contracted to 11.3% from 20.1%

- Profit Before Tax (PBT) declined to ₹149 crore, down 54% YoY

FY26 Standalone Highlights:

- Revenue from operations declined to ₹765 crore, down 35% YoY

- EBITDA stood at ₹115 crore, down 60% YoY

- EBITDA margin reduced to 15.0%

- PBT fell to ₹164 crore, down 50% YoY

Q4FY26 Consolidated Highlight:

- Quarterly revenue declined to ₹338 crore, down 31% YoY

- EBITDA declined to ₹52 crore, down 49% YoY

- EBITDA margin stood at 15.5%

- Quarterly PBT declined 53% YoY

Additional Highlight:

- Board proposed final dividend of ₹5 per share

- Beyond India Summer Portfolio (BISP) contributed 49% of FY26 consolidated revenue

- U.S. operations remained profitable during both quarterly and annual periods

Highlight:

- Symphony approved a strategic restructuring of its Australian business, including impairments of approximately ₹298 crore (standalone) and ₹259 crore (consolidated) to align carrying values with market realities.

What Happened ?

Symphony Limited reported weaker FY26 financial performance due to subdued domestic demand, export challenges, and persistent operational difficulties in Australia.

The company highlighted that domestic channel partners remained cautious amid inventory overhangs, while exports faced geopolitical disruptions in the Middle East. Australian subsidiary Climate Technologies Pty Ltd (CTPL) continued to witness stagnant revenues and losses.

To improve operational clarity and financial discipline, Symphony initiated a strategic balance sheet reset in Australia and approved acquisitions of intellectual property rights and U.S.-based Bonaire USA LLC.

Key Details

Operational Performance:

- Domestic demand remained weak during the March 2026 quarter

- Inventory overhang impacted channel sales momentum

- Export revenue affected by geopolitical headwinds in Middle East markets

- U.S. operations continued to remain profitable

Business Diversification:

- Beyond India Summer Portfolio (BISP) revenue reached ₹192 crore

- BISP contributed around 25% of standalone revenue

- Diversified segments helped reduce seasonal dependence on air cooler demand

Australia Reset:

- Symphony initiated a strategic reset of Australian operations

- Impairments booked to improve transparency and align business valuations

- No additional capital allocation planned beyond approved commitments

Acquisitions Approved:

- Acquisition of CTPL intellectual property rights for approximately ₹23 crore

- Acquisition of Bonaire USA LLC for approximately ₹30 crore

- Transactions aimed at improving ownership clarity and reducing working capital borrowings

Risk Analysis

Key Risks:

- Weak summer demand in some regions

- Channel inventory overhang impacting sales

- Margin contraction due to operating deleverage

- Continued weakness in Australian subsidiary operations

- Export uncertainty because of geopolitical disruptions

Worst Case Scenario:

- If domestic demand recovery remains slow and overseas subsidiaries continue underperforming, profitability and cash flow generation could remain under pressure in FY27.

Risk Level: High

Company Commentary

- Management stated that business momentum improved from early April in South and West India

- Domestic summer demand is yet to fully pick up across North and Northeast India

- Symphony emphasized long-term focus on ownership simplification and capital discipline

- The company expects strategic acquisitions to improve control over key brands and intellectual property

- Management reiterated commitment toward operational efficiency and global business optimization

Official Exchange Filing: Symphony Limited