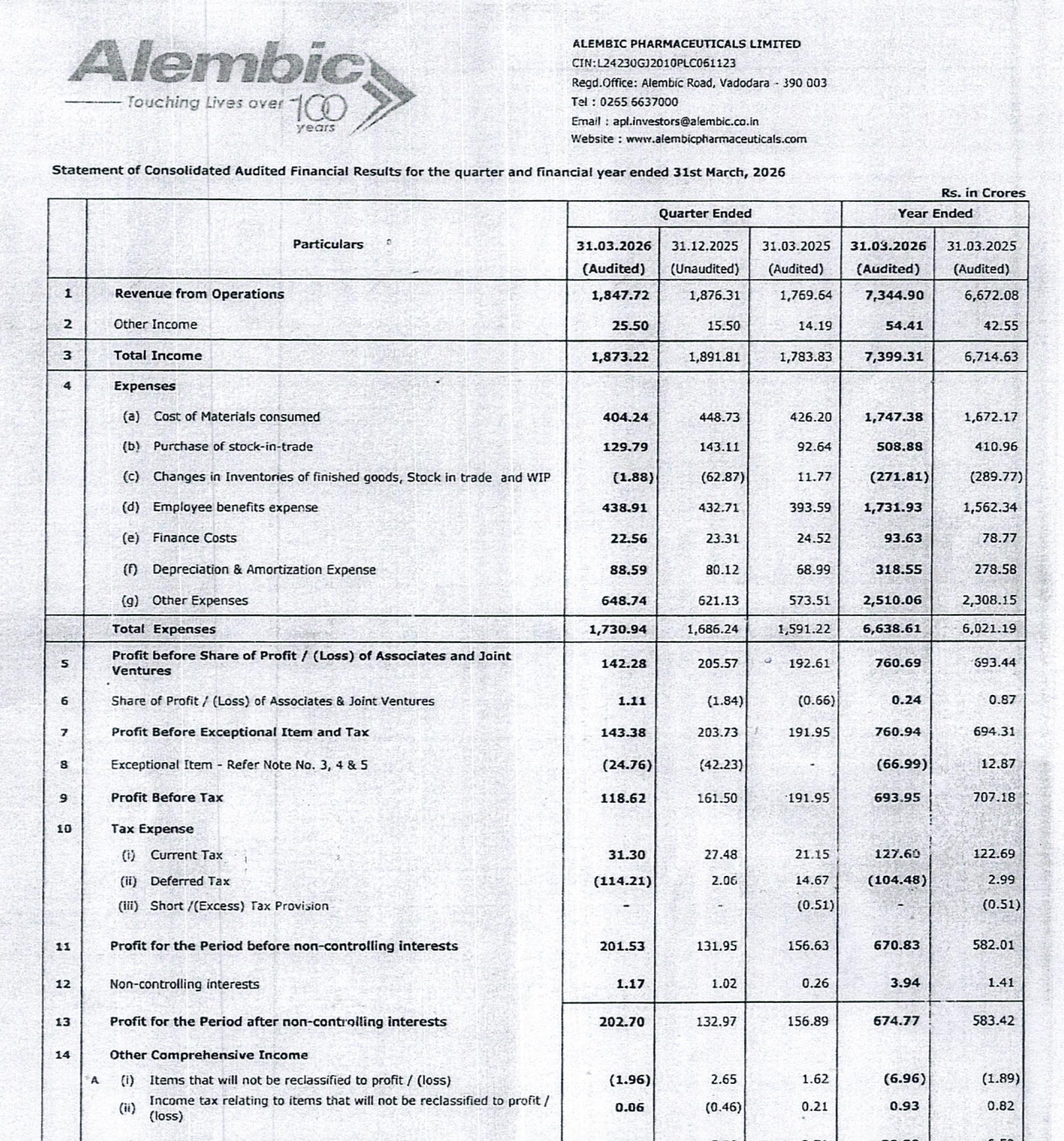

Quarter Ended: March 2026

Alembic Pharmaceuticals Limited – Q4 FY26 Results

NSE

aplltd

BSE

533573

Alembic Pharmaceuticals Limited reported steady revenue growth in Q4 FY26, while profitability improved sequentially despite pressure from exceptional items and elevated operating costs.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,847.72 Crores

- QoQ Change: -1.52%

- YoY Change: +4.41%

- Previous Quarter (Q3 FY26): ₹1,876.31 Crores

- Previous Year (Q4 FY25): ₹1,769.64 Crores

- Revenue (Q4 FY26): ₹1,847.72 Crores

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹202.70 Crores

- QoQ Change: +52.45%

- YoY Change:+29.19%

- Previous Quarter (Q3 FY26): ₹132.97 Crores

- Previous Year (Q4 FY25): ₹156.89 Crores

- PAT (Q4 FY26): ₹202.70 Crores

- QoQ Performance:

- Revenue Trend: Revenue remained largely stable sequentially with marginal decline.

- Profit Trend: Net profit improved significantly QoQ driven by operational recovery and lower exceptional drag.

- Revenue Trend: Revenue remained largely stable sequentially with marginal decline.

Margin Analysis

Drivers:

- Higher employee benefit expenses impacted margins.

- Other operating expenses remained elevated.

- Inventory movement supported operational efficiency.

- Finance costs remained under control.

- Exceptional item losses impacted profitability.

Insight:

- The company demonstrated resilient profitability despite ongoing margin pressures in the pharmaceutical sector.

Earning quality check

Key Drivers:

- Operating cash flow improved sharply during FY26.

- Working capital management improved significantly versus last year.

- Cash generation remained healthy despite higher inventory levels.

- Finance costs remained manageable.

- Core operating profitability supported earnings.

Interpretations:

- Earnings quality remains healthy with profitability supported by operating cash flows and stable pharmaceutical operations.

balance sheet Analysis

- Total Assets: ₹8,762.59 Crores

- Total Liabilities: ₹3,093.61 Crores

Insight:

- The company maintained a strong balance sheet with healthy equity base, manageable borrowings, and improved cash position during FY26.

key risks

- Pricing pressure in US generics market.

- Regulatory compliance risks.

- Margin pressure from raw material costs.

- Currency fluctuation risks.

- Competition in domestic formulations.

- Elevated operating expenditure.

management strategy signals

Focus Area:

- Expansion in specialty and regulated markets.

- Product pipeline enhancement.

- Improving operational efficiencies.

- Strengthening domestic branded portfolio.

- Controlled capex and R&D investments.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹1,873.22 Crores | -0.98% | +5.01% |

| PBT | ₹118.62 Crores | -26.55% | -38.20% |

| PAT | ₹202.70 Crores | +52.45% | +29.19% |

Alembic Pharmaceuticals Limited delivered a stable Q4 FY26 performance with modest revenue growth and strong sequential profit recovery. While margin pressure and exceptional items weighed on profitability, the company maintained healthy operating cash flows and balance sheet strength. Long-term growth prospects remain supported by its diversified pharmaceutical portfolio, export opportunities, and operational scale.

Official Exchange Filing: Alembic Pharmaceuticals Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED