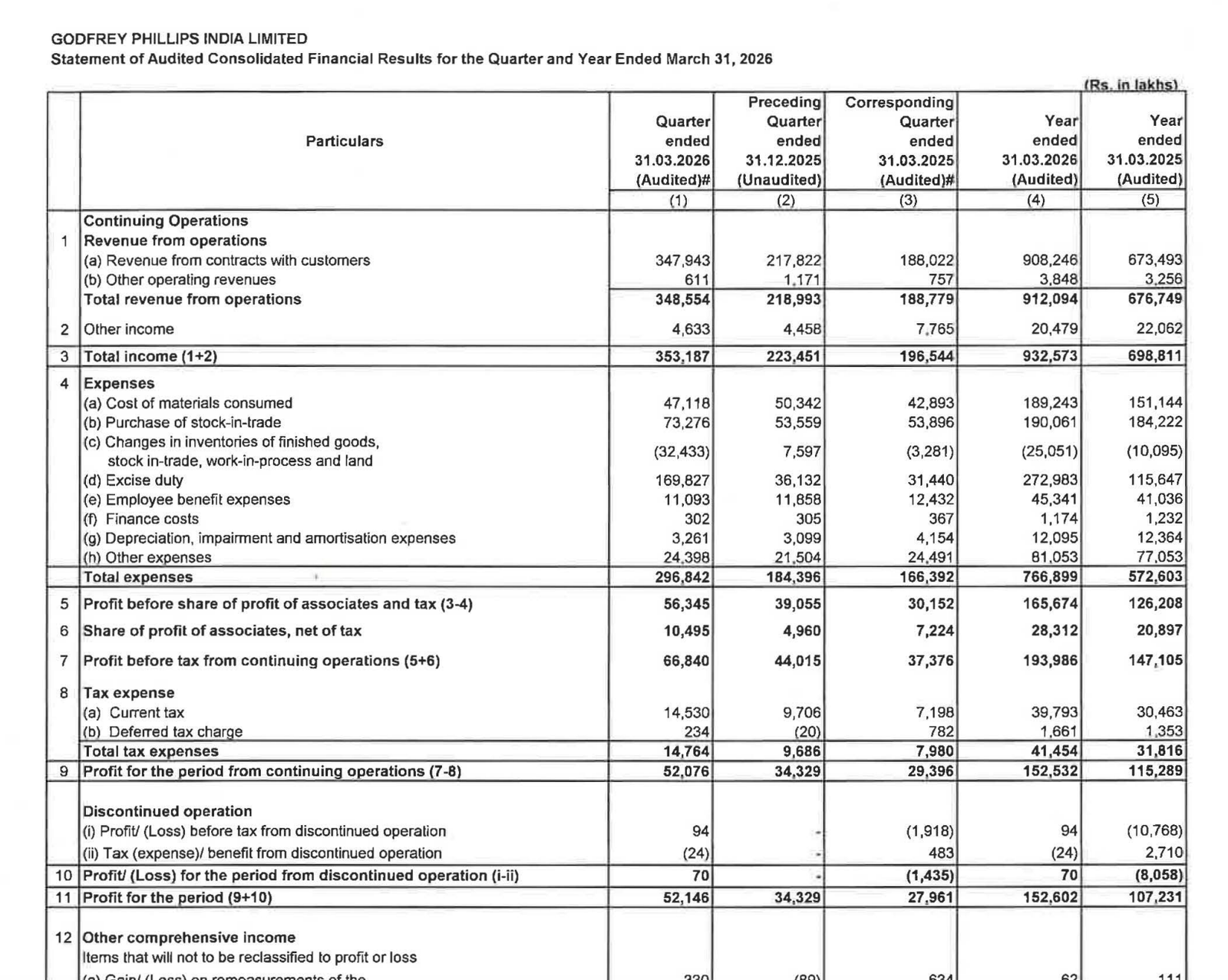

Quarter Ended: March 2026

Godfrey Phillips India Limited – Q4 FY26 Results

NSE

GODFRYPHLP

BSE

500163

Godfrey Phillips India reported a strong Q4 FY26 performance with sharp growth in revenue and profitability driven by its cigarettes and tobacco business.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹3,48,554 Lakh

- QoQ Change: +59.2%

- YoY Change: +84.6%

- Previous Quarter (Q3 FY26): ₹2,18,993 Lakh

- Previous Year (Q4 FY25): ₹1,88,779 Lakh

- Revenue (Q4 FY26): ₹3,48,554 Lakh

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹52,146 Lakh

- QoQ Change: +51.9%

- YoY Change:+86.5%

- Previous Quarter (Q3 FY26): ₹34,329 Lakh

- Previous Year (Q4 FY25): ₹27,961 Lakh

- PAT (Q4 FY26): ₹52,146 Lakh

- Trend:

- Revenue Trend: Revenue surged sharply both sequentially and annually due to strong growth in cigarettes and tobacco products.

- Profit Trend: Profitability improved significantly due to higher revenue scale, operating leverage, and improved segment profitability.

- Revenue Trend: Revenue surged sharply both sequentially and annually due to strong growth in cigarettes and tobacco products.

Margin Analysis

Drivers:

- Excise duty-linked revenue growth boosted operating scale.

- Tobacco segment EBIT more than doubled YoY.

- Employee and finance costs remained relatively controlled versus revenue expansion.

- Inventory adjustments supported quarterly profitability.

- Associate income contribution remained strong.

Insight:

- The company demonstrated strong operating leverage with profits growing faster than revenue.

Segment performance

Segments: Cigarettes, Tobacco and Related Products

- Revenue: ₹3,461.81 crore

- Insights:

- Core segment contributed nearly entire consolidated revenue.

- Segment revenue rose sharply from ₹1,865.89 crore YoY.

- Segment profit more than doubled YoY.

Segments: Other

- Revenue: ₹23.73 Crores

- Insights:

- Non-core business contribution remained limited.

- Segment profitability stayed weak.

Segment insight

Business Summary:

The company remains predominantly dependent on its cigarettes and tobacco portfolio for growth and profitability.

Key Characteristics:

- High-margin tobacco-led business model.

- Strong pricing and distribution strength.

- Large operating leverage benefits visible.

- Minor contribution from non-core operations.

Earning quality check

Key Drivers:

- Net cash generated from operating activities increased to ₹518.16 crore.

- Profit before working capital changes rose significantly.

- Associate income contribution remained healthy.

- Finance costs remained under control.

Interpretations:

- Earnings quality appears strong as profitability is supported by cash flow generation and operational performance.

balance sheet Analysis

- Total Assets: ₹8,310.38 crore

- Total Liabilities: ₹2,091.30 crore

Insight:

- Equity base strengthened substantially.

- Current assets increased materially due to inventory and receivable growth.

- Company maintained relatively low debt levels.

key risks

- Tobacco sector regulatory risks.

- Excise duty changes may impact profitability.

- Heavy dependence on cigarettes business.

- ESG-related pressure on tobacco companies.

- Working capital intensity increased during FY26.

management strategy signals

Focus Area:

- Expanding tobacco business scale.

- Improving profitability and operational efficiency.

- Strengthening market leadership.

- Maintaining dividend payouts.

- Efficient capital allocation.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹3,531.87 Crore | +58.1% | +79.7% |

| PBT | ₹668.40 Crore | +51.9% | +78.8% |

| PAT | ₹521.46 Crore | +51.9% | +86.5% |

Godfrey Phillips India delivered an exceptionally strong Q4 FY26 performance with sharp revenue growth, expanding profitability, strong operating cash flow generation, and improved balance sheet strength. The tobacco segment remains the dominant earnings driver, though regulatory and taxation risks continue to remain important long-term monitorables.

Official Exchange Filing: Godfrey Philips India Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED