Quarter Ended: March 2026

Seamec Limited – Q4 FY26 Results

NSE

seamecltd

BSE

526807

Seamec Limited delivered a sharp improvement in Q4 FY26 profitability backed by strong overseas segment recovery, higher operating leverage, and substantial annual revenue expansion.

key financial highlights

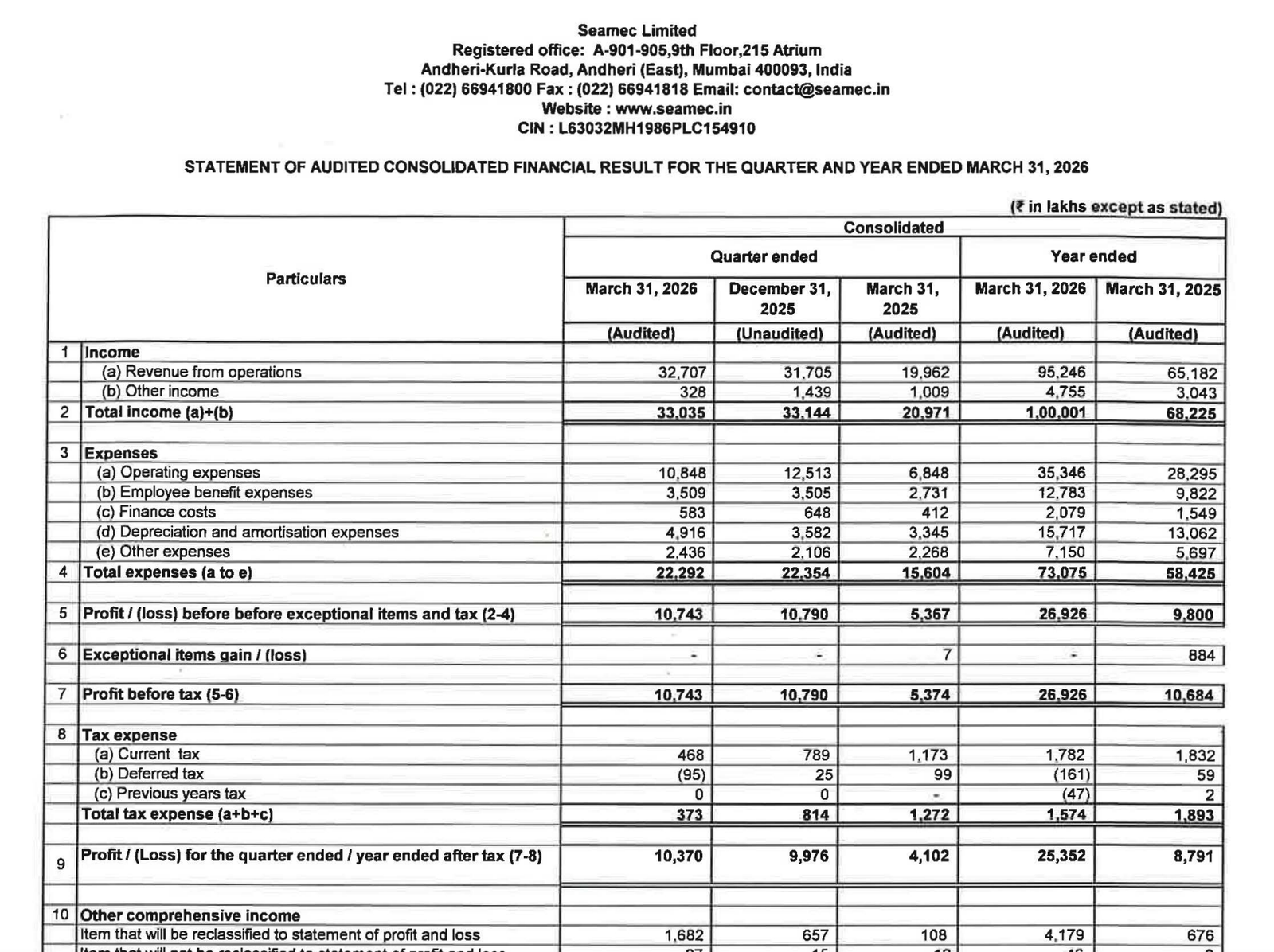

- Revenue from Operations:

- Revenue (Q4 FY26): ₹32,707 Lakhs

- QoQ Change: +3.16%

- YoY Change: +63.84%

- Previous Quarter (Q3 FY26): ₹31,705 Lakhs

- Previous Year (Q4 FY25): ₹19,962 Lakhs

- Revenue (Q4 FY26): ₹32,707 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹10,370 Lakhs

- QoQ Change: +3.95%

- YoY Change: +152.80%

- Previous Quarter (Q3 FY26): ₹9,976 Lakhs

- Previous Year (Q4 FY25): ₹4,102 Lakhs

- PAT (Q4 FY26): ₹10,370 Lakhs

- QoQ Performance:

- Revenue Trend: Stable sequential growth supported by offshore business momentum.

- Profit Trend: Profit remained resilient QoQ despite elevated depreciation and finance costs.

- Revenue Trend: Stable sequential growth supported by offshore business momentum.

Margin Analysis

Drivers:

- Strong revenue growth improved operational leverage.

- Overseas segment profitability turned positive versus prior-year losses.

- Higher depreciation reflects ongoing asset and vessel investments.

- Finance costs increased due to borrowings and expansion activities.

- Employee costs remained controlled relative to revenue growth.

Insight:

- Operational efficiency improved materially as fixed costs were absorbed by higher offshore execution volumes.

Segment performance

Segments: Domestic

- Revenue: ₹24,921 lakhs

- Insights:

- Domestic business continued contributing majority revenue share.

- Domestic profitability remained stable and strong.

- Sequential performance softened slightly but remained healthy.

Segments: Overseas

- Revenue: ₹7,786 lakhs

- Insights:

- Overseas revenue remained stable QoQ.

- Segment profitability improved sharply from prior-year loss.

- International offshore demand recovery significantly supported earnings.

Segment insight

Business Summary:

Seamec’s earnings profile improved substantially due to recovery in international offshore operations alongside steady domestic execution.

Key Characteristics:

- Offshore marine services-led business model.

- Asset-heavy operations with vessel deployment dependency.

- Revenue visibility linked to offshore energy activity.

- International segment turnaround materially improved margins.

Earning quality check

Key Drivers:

- Operating cash flow remained very strong at ₹32,130 lakhs.

- Profit growth aligned with revenue expansion.

- Positive working capital support from payables.

- Strong recurring operating profitability.

- Large capex investments indicate long-term capacity expansion.

Interpretations:

- Earnings quality appears strong with healthy operating cash generation, though receivable expansion and rising leverage require monitoring.

balance sheet Analysis

- Total Assets: ₹1,86,076 lakhs

- Total Liabilities: ₹55,699 lakhs

Insight:

- The balance sheet strengthened considerably with rising equity base, expanding cash reserves, and increased asset deployment supporting long-term growth strategy.

key risks

- Trade receivables increased sharply year-on-year.

- Higher borrowings increased finance cost burden.

- Offshore business remains cyclical and energy-price sensitive.

- Elevated capex could pressure future free cash flow.

- Asset-heavy model exposes company to utilization risks.

management strategy signals

Focus Area:

- Expansion of offshore asset utilization.

- Overseas business recovery and scaling.

- Strengthening long-duration offshore contracts.

- Strategic capex deployment.

- Improving operational efficiency.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹33,035 Lakhs | -0.33% | +57.53% |

| PBT | ₹10,743 Lakhs | -0.44% | +99.94% |

| PAT | ₹10,370 Lakhs | +3.95% | +152.80% |

Seamec Limited reported an exceptionally strong Q4 FY26 performance driven by offshore business recovery, significant YoY profitability expansion, and robust operating cash flows. The overseas segment turnaround and strong margin profile materially strengthened earnings quality. While leverage and receivable growth warrant monitoring, the company appears positioned for continued operational momentum supported by offshore energy activity and strategic asset investments.

Official Exchange Filing: Seamec Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED