Rating Action

Ramkrishna Forgings Credit Rating Downgraded by India Ratings Amid Elevated Debt and Margin Pressure

NSE

rkforge

BSE

532527

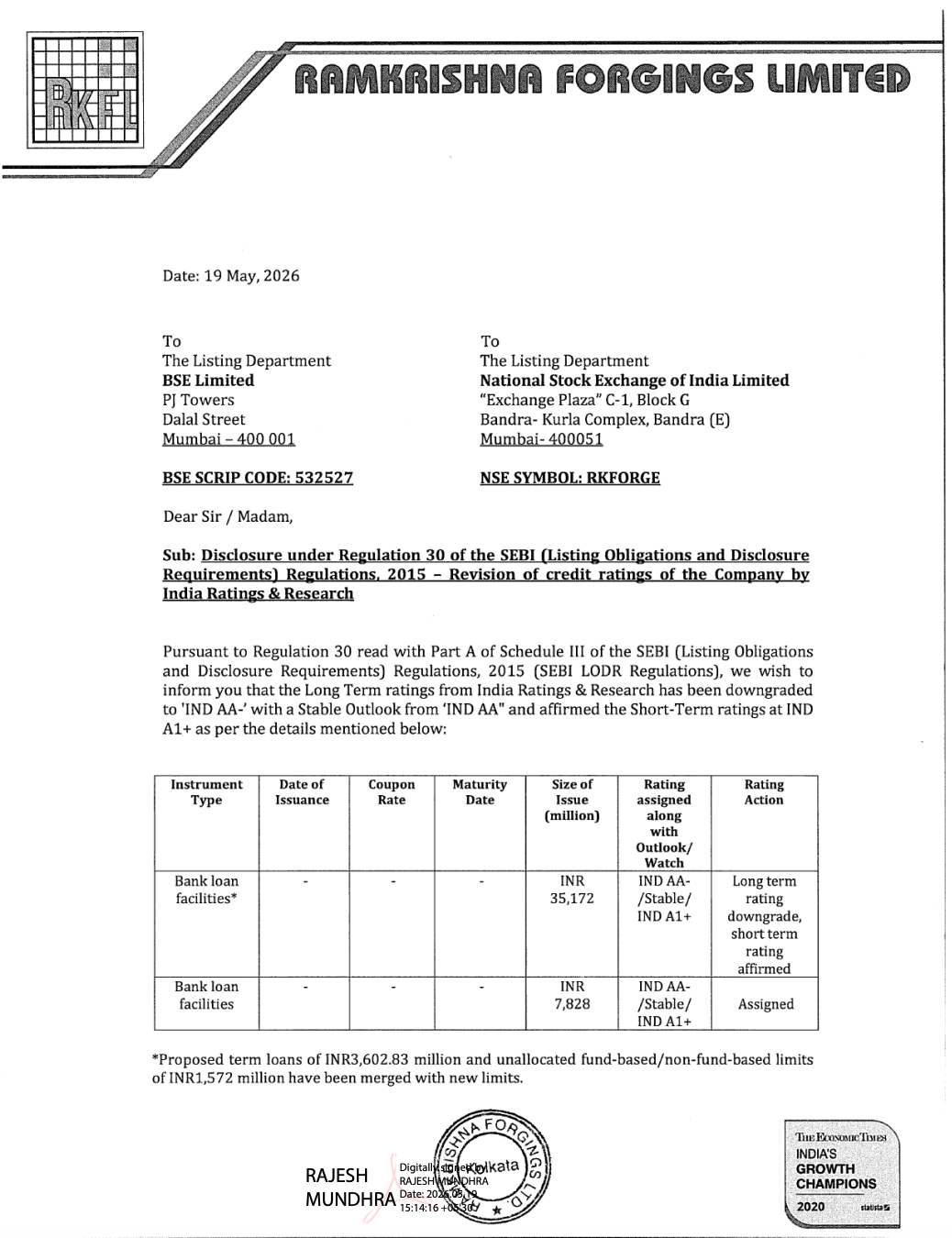

Ramkrishna Forgings Limited informed exchanges that India Ratings & Research has downgraded the company’s long-term credit rating to IND AA- from IND AA while maintaining a Stable Outlook. The downgrade reflects weakened credit metrics, elevated leverage due to ongoing capex, margin moderation, and inventory accounting discrepancies identified during FY25 verification.

PRICE-SENSITIVE TRIGGER

Event: Credit Rating Downgrade by India Ratings & Research

Type: Rating Action

Impact: Negative

Immediate Effect: The downgrade indicates increased pressure on the company’s leverage profile and profitability, which may impact future borrowing costs and investor sentiment.

Key Metrics:

- Long-Term Rating: Downgraded to IND AA- from IND AA

- Short-Term Rating: Affirmed at IND A1+

- Rated Bank Facilities: INR 35,172 million

- Additional Bank Facilities: INR 7,828 million

- FY26 Revenue: INR 42,381 million (+5.1% YoY)

- FY26 EBITDA Margin: 15.2%

- FY26 Net Adjusted Leverage: 4.6x

- FY26 Capex: INR 9,237 million

- FY26 Cash Flow from Operations: INR 6,503 million

- FY26 Free Cash Flow: Negative INR 2,915 million

Highlight Metric:

- Inventory overstatement resulted in an adverse post-tax impact of approximately INR 2,026 million, equivalent to nearly 6.73% of net worth.

What Happened ?

Ramkrishna Forgings Limited disclosed that India Ratings & Research downgraded its long-term bank loan facilities rating to IND AA- with Stable Outlook while affirming the short-term rating at IND A1+.

The rating agency cited weakened credit metrics, elevated leverage levels, ongoing debt-funded capex, and moderation in EBITDA margins as key reasons behind the downgrade. Lower export contribution, especially from high-margin North American business, also impacted profitability.

Additionally, the agency highlighted inventory discrepancies identified during FY25 annual physical verification, which negatively impacted margins and financial metrics.

Key Details

Rating Rationale:

- Adjusted consolidated net leverage increased to 4.64x in FY26 due to elevated debt and capex spending.

- EBITDA margins moderated because of reduced share of high-margin exports.

- Interest coverage ratio declined to 3.1x in FY26 from 5.3x in FY24.

- Total debt levels increased to INR 31,438 million in FY26.

Inventory Discrepancies:

- RKFL identified discrepancies between physical inventory and book inventory during FY25 verification.

- The issue involved work-in-progress, raw materials, and scrap accounting.

- Inventory overstatement stood at INR 2,205.2 million as of March 31, 2025.

- Management stated that internal controls have now been strengthened.

Operational Positives:

- FY26 consolidated revenue grew 5.1% YoY to INR 42,381 million.

- The company expects FY27 revenue to rise to INR 48,000–50,000 million.

- Diversification into railways, EVs, aluminum forgings, and non-auto sectors continues.

- Revenue contribution from non-auto businesses increased to 26% in FY26.

- Indian Railways contribution improved to 7.5% of revenue.

Liquidity and Funding:

- Consolidated cash balance stood at INR 1,629 million at FY26 end.

- Promoters infused INR 2,020 million through warrants.

- Additional tax refunds of around INR 2,800 million are expected to support liquidity.

Note:

- India Ratings expects leverage to improve gradually in FY27, but remain above preferred threshold levels in the near term.

Risk Analysis

Key Risks:

- High debt levels due to aggressive capex and acquisitions.

- Dependence on cyclical MHCV industry demand.

- Continued weakness in exports may impact margins further.

- Working capital cycle remains elevated at 193 days.

- Newly acquired businesses currently operate at lower margins.

Worst Case Scenario:

- If export demand recovery remains slow and leverage stays elevated above 3x for an extended period, further pressure on ratings and profitability may emerge.

Risk Level: High

Company Commentary

- Management expects consolidated revenue to grow further in FY27 driven by domestic CV recovery and railway orders.

- RKFL stated that internal controls have been strengthened after inventory discrepancies were identified.

- The company continues expanding into EVs, railways, aluminum forgings, and non-auto industrial segments.

- Management expects gradual improvement in leverage and profitability over the next two-to-three years.

Official Exchange Filing: Ramkrishna Forgings Limited