Financial Results with Business Expansion

Asian Energy Services Delivers Strong FY26 Growth; Revenue Surges 70% YoY

NSE

asianene

BSE

530355

Asian Energy Services Limited reported robust FY26 performance driven by strong execution momentum, Kuiper acquisition integration, and improved operational efficiencies. FY26 revenue rose 70.1% YoY to ₹791.1 crore, while adjusted PAT increased 43.6% YoY to ₹60.6 crore. The company also maintained a healthy order book of around ₹1,750 crore and announced a dividend of ₹1.25 per share.

PRICE-SENSITIVE TRIGGER

Event: Asian Energy Services announced audited Q4 FY26 and FY26 financial results along with business expansion updates.

Type: Financial Results with Business Expansion

Impact: Positive

Immediate Effect: Strong growth in revenue, EBITDA, and profitability along with healthy order book visibility and merger progress boosted operational outlook.

Key Metrics:

Q4 FY26 Performance:

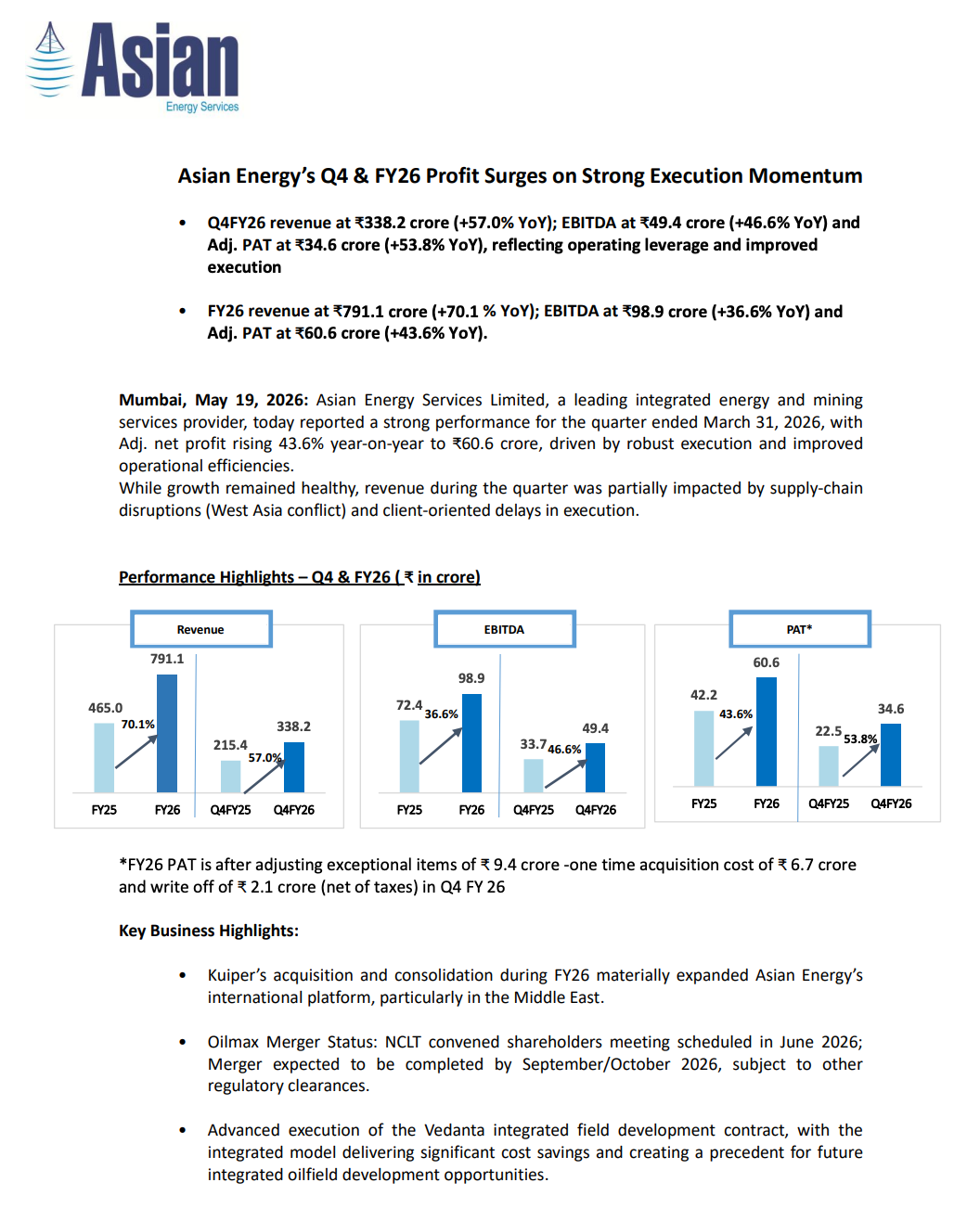

- Revenue: ₹338.2 crore vs ₹215.4 crore YoY (+57.0%)

- EBITDA: ₹49.4 crore vs ₹33.7 crore YoY (+46.6%)

- Adjusted PAT: ₹34.6 crore vs ₹22.5 crore YoY (+53.8%)

FY26 Performance:

- Revenue: ₹791.1 crore vs ₹465.0 crore YoY (+70.1%)

- EBITDA: ₹98.9 crore vs ₹72.4 crore YoY (+36.6%)

- Adjusted PAT: ₹60.6 crore vs ₹42.2 crore YoY (+43.6%)

Other Key Metric:

- Standalone Order Book: ~₹1,750 crore

- Dividend Announced: ₹1.25 per share

- Indrora Block Current Production: ~100 BOPD

- Target Production FY27: ~1,000 BOPD

- Recent Warrant Conversion Proceeds: ₹92 crore

Highlight Metric:

- FY26 revenue surged 70.1% YoY to ₹791.1 crore.

What Happened ?

Asian Energy Services Limited delivered strong FY26 financial performance supported by robust project execution, operational efficiencies, and strategic business expansion.

The company highlighted that the acquisition and consolidation of Kuiper significantly strengthened its international platform, particularly in the Middle East. Progress was also reported in the Oilmax merger process, which is expected to complete by September/October 2026 subject to approvals.

During FY26, the company secured major contracts including the Vedanta integrated field development project and the Lakhanpur CHP Project from MCL. Operational progress in the Indrora Block also improved production visibility.

Despite temporary supply-chain disruptions due to the West Asia conflict and some client-side execution delays, the company maintained strong profitability growth.

Key Details

Business Expansion & Strategic Developments:

- Kuiper acquisition expanded AESL’s international operations and Middle East presence.

- Oilmax merger process is progressing with NCLT shareholder meeting expected in June 2026.

- Merger completion targeted by September/October 2026.

Operational Highlights:

- Vedanta integrated field management contract progressed significantly.

- Lakhanpur CHP Project secured from MCL during FY26.

- NM-01 well in Indrora Block currently producing ~100 BOPD.

- Company targets ~1,000 BOPD production at block level by FY27.

Financial & Balance Sheet Strength:

- Company remains net-zero debt.

- ₹92 crore received through warrant conversion further strengthened liquidity.

- Strong order book provides long-term revenue visibility.

Future Guidance:

- Management expects standalone India services business growth of 30-40% in FY27.

- Kuiper revenue guidance for FY27 stands at USD 60–65 million with improved margins.

Note:

- Standalone Q4FY26 revenue was partially impacted by supply-chain disruptions arising from the West Asia conflict and client-oriented execution delays.

Risk Analysis

Key Risks:

- West Asia conflict may continue disrupting supply chains.

- Delay in Oilmax merger approvals could affect strategic timelines.

- Project execution delays from clients may impact quarterly revenue.

- Commodity and energy price volatility could pressure margins.

- International expansion exposes business to geopolitical uncertainty.

Worst Case Scenario:

- Prolonged geopolitical disruptions or delayed project execution may weaken revenue growth and margin expansion in FY27.

Risk Level: Medium

Company Commentary

- FY26 has been a landmark year for Asian Energy, driven by the Kuiper acquisition and initiation of the Oilmax merger.

- We move into FY27 with a healthy order book, strong balance sheet, and expansive opportunity pipeline.

- We are pleased to announce a dividend of ₹1.25 per share.

- We remain confident of growing our standalone India services business by 30-40% in FY27.

Official Exchange Filing: Asian Energy Services Limited