Quarterly & Annual Financial Results

DEE Development Engineers Reports 38% FY26 Revenue Growth, Record EBITDA and Strong Order Book of ₹1,940 Crore

NSE

deedev

BSE

544198

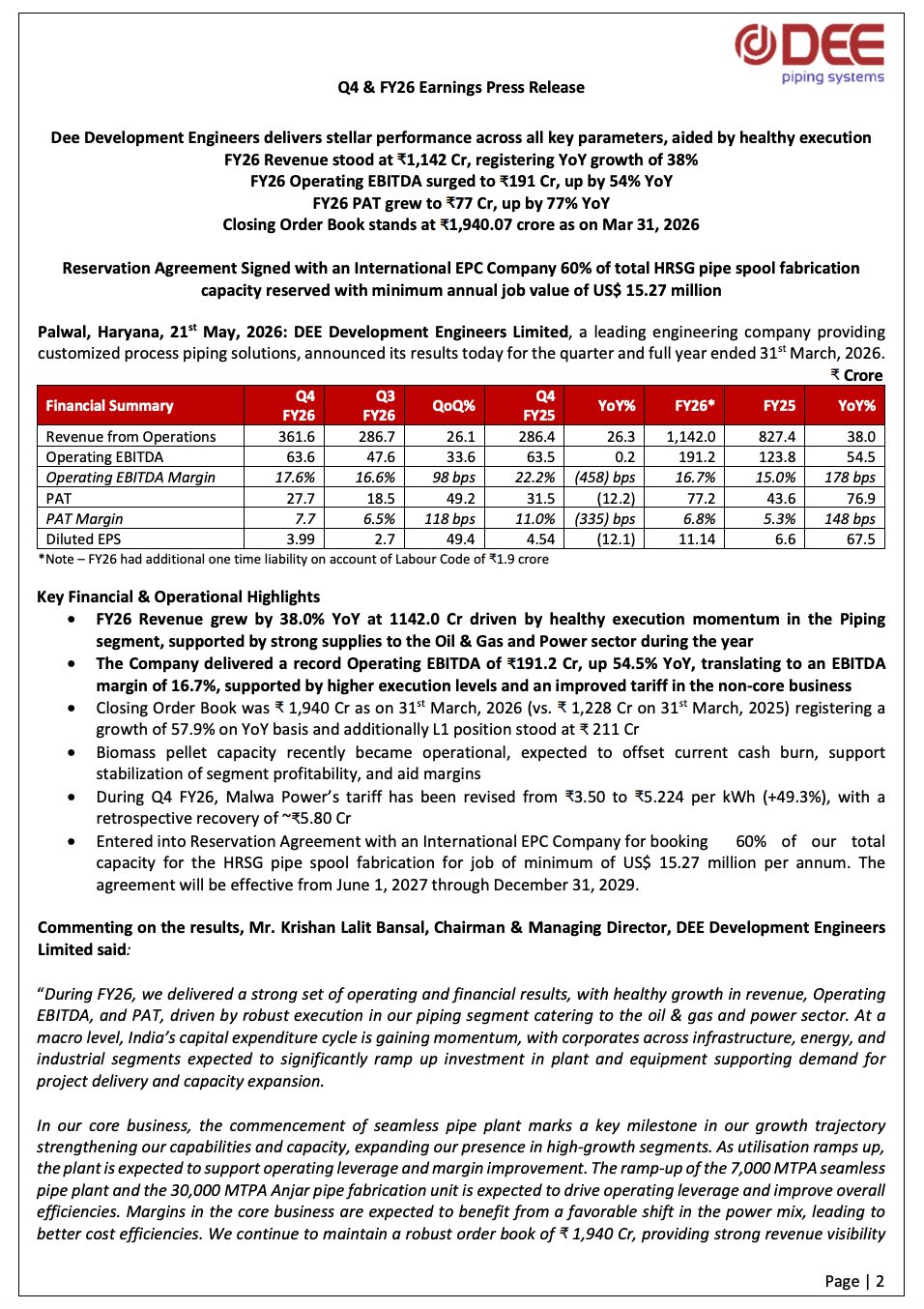

DEE Development Engineers Limited reported strong FY26 financial performance with revenue rising 38% YoY to ₹1,142 crore, EBITDA increasing 54.5% YoY to ₹191.2 crore, and PAT growing 77% YoY to ₹77.2 crore. The company also reported a closing order book of ₹1,940 crore and signed an international reservation agreement securing 60% of HRSG fabrication capacity with minimum annual business value of USD 15.27 million.

PRICE-SENSITIVE TRIGGER

Event: Q4 & FY26 Audited Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong revenue growth, record EBITDA performance, improving margins, and robust order book strengthened visibility for future growth and operational expansion.

Key Metrics:

- FY26 Revenue: ₹1,142.0 Crore

- FY26 Revenue Growth: 38.0% YoY

- FY26 EBITDA: ₹191.2 Crore

- FY26 EBITDA Growth: 54.5% YoY

- FY26 EBITDA Margin: 16.7%

- FY26 PAT: ₹77.2 Crore

- FY26 PAT Growth: 76.9% YoY

- Closing Order Book: ₹1,940.07 Crore

- Q4 FY26 Revenue: ₹361.6 Crore

- Q4 FY26 EBITDA: ₹63.6 Crore

- Q4 FY26 PAT: ₹27.7 Crore

- Q4 FY26 EBITDA Margin: 17.6%

- Reservation Agreement Value: Minimum USD 15.27 Million annually

Highlight Metric:

- DEE Development Engineers delivered record FY26 EBITDA of ₹191.2 crore with 54.5% YoY growth and strong order book visibility of ₹1,940 crore.

What Happened ?

DEE Development Engineers Limited announced its audited Q4 and FY26 financial results, reporting strong operational and profitability growth driven by healthy execution momentum in the piping business and robust demand from oil & gas and power sectors.

For FY26:

- Revenue grew 38% YoY to ₹1,142 crore.

- EBITDA increased 54.5% YoY to ₹191.2 crore.

- EBITDA margin improved to 16.7%.

- PAT rose 77% YoY to ₹77.2 crore.

- Closing order book stood at ₹1,940 crore.

For Q4 FY26:

- Revenue increased 26.3% YoY to ₹361.6 crore.

- EBITDA jumped sharply to ₹63.6 crore.

- PAT stood at ₹27.7 crore.

- EBITDA margin improved to 17.6%.

The company also highlighted:

- Seamless pipe plant commissioning progress.

- Biomass pellet facility becoming operational.

- Tariff revision benefits at Malwa Power.

- Reservation agreement with international EPC company ensuring minimum annual revenue visibility of USD 15.27 million.

Management stated that strong infrastructure, energy, and industrial capex cycles are supporting future growth opportunities.

Key Details

Operational Performance & Growth Outlook:

- FY26 revenue growth:

- 38% YoY to ₹1,142 crore.

- FY26 EBITDA:

- ₹191.2 crore with 16.7% margin.

- FY26 PAT:

- ₹77.2 crore.

- Order book:

- ₹1,940 crore as of March 31, 2026.

- Q4 revenue:

- ₹361.6 crore.

- Q4 EBITDA margin:

- 17.6%.

- Q4 PAT margin:

- 7.7%.

- Key growth drivers:

- Strong execution in piping segment.

- Oil & gas sector demand.

- Power sector supplies.

- Reservation agreement:

- 60% HRSG fabrication capacity reserved.

- Minimum annual job value of USD 15.27 million.

- Infrastructure expansion:

- 7,000 MTPA seamless pipe plant ramp-up.

- 30,000 MTPA Anjar fabrication unit expected to improve operating leverage.

- Non-core power segment:

- Malwa Power tariff revised from ₹3.50 to ₹5.224 per kWh.

- Retrospective recovery of approximately ₹5.80 crore.

- Biomass pellet facility:

- Became operational during FY26.

- Debt outlook:

- Improving cash flows expected to gradually reduce debt levels.

- Market outlook:

- Strong infrastructure and industrial capex momentum expected to continue.

Note:

- Management expects operational leverage, improved utilization, and stronger order execution to support future margin expansion and sustained growth.

Risk Analysis

Summary:

- Despite strong execution and order book visibility, the company remains exposed to infrastructure execution risks, commodity cost volatility, and cyclical industrial demand conditions.

Key Risks:

- Dependence on infrastructure and industrial capex cycles.

- Raw material and steel price volatility may impact margins.

- Large project execution delays can affect cash flows.

- International EPC exposure may involve geopolitical and currency risks.

- Power and energy sector dependence could create cyclicality.

- Capacity expansion ramp-up execution remains critical.

Worst Case Scenario:

- If infrastructure spending slows or execution delays emerge across major projects, revenue visibility and profitability expansion could weaken despite strong order book levels.

Risk Level: Medium

Company Commentary

- Management stated FY26 delivered strong operational and financial performance across core business segments.

- The company highlighted healthy execution momentum in piping operations catering to oil & gas and power sectors.

- DEE confirmed record operating EBITDA and strong order book growth.

- Management stated that infrastructure, energy, and industrial capex momentum remains favorable.

- The company emphasized that the seamless pipe plant and Anjar fabrication unit will support future operating leverage.

- DEE confirmed reservation agreement with international EPC company securing long-term fabrication utilization visibility.

- Management expects improving operating cash flows and gradual debt reduction going forward.

Official Exchange Filing: DEE Development Engineers Limited