Quarterly & Annual Financial Results

Juniper Hotels Reports Strong Q4 & FY26 Performance with Record Revenue and PAT Growth

NSE

juniper

BSE

544129

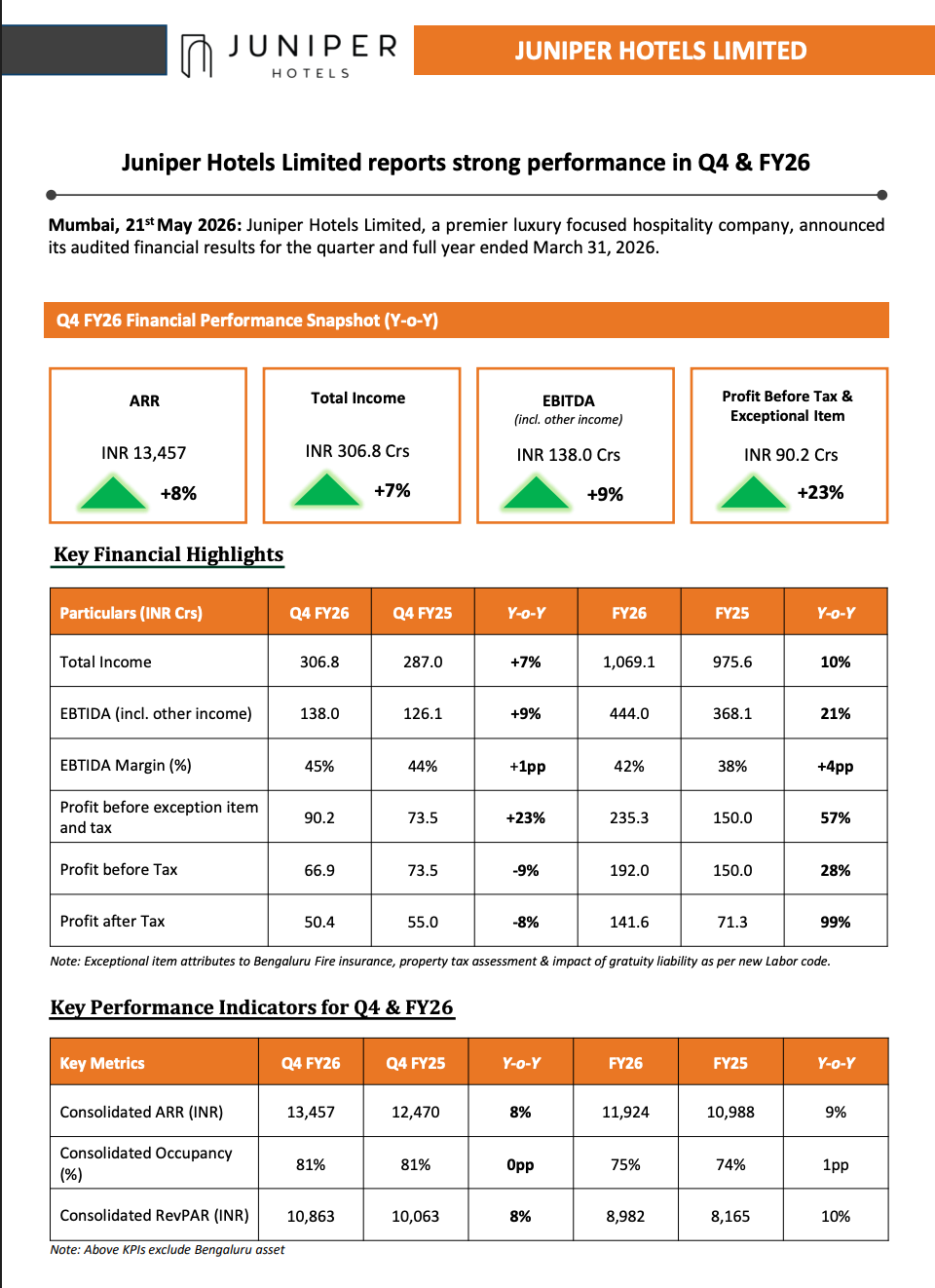

Juniper Hotels Limited reported strong audited Q4 and FY26 financial performance driven by robust demand across Grand Hyatt Mumbai, Andaz Delhi and Hyatt Regency Ahmedabad. FY26 total income crossed ₹1,069 crore while PAT nearly doubled to ₹142 crore. The company also announced expansion plans including a new luxury hotel project in Dwarka, New Delhi and upcoming Westin Bengaluru operations.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Audited Financial Results Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered record annual revenue, strong EBITDA growth, improved margins, and significant PAT expansion supported by operational leverage, occupancy improvement, and premium hospitality demand.

Key Metrics:

- FY26 Total Income: ₹1,069.1 Crore

- FY25 Total Income: ₹975.6 Crore

- FY26 Revenue Growth: 10% YoY

- Q4 FY26 Revenue: ₹306.8 Crore

- Q4 FY26 EBITDA: ₹138.0 Crore

- FY26 EBITDA: ₹444.0 Crore

- FY26 EBITDA Growth: 21% YoY

- FY26 EBITDA Margin: 42%

- FY26 PAT: ₹141.6 Crore

- FY25 PAT: ₹71.3 Crore

- FY26 PAT Growth: 99% YoY

- Q4 FY26 PAT: ₹50.4 Crore

- Portfolio ARR: ₹13,457

- Portfolio Occupancy: 81%

- FY26 Consolidated RevPAR: ₹8,982

- FY26 RevPAR Growth: 10% YoY

Highlight Metric:

- Juniper Hotels reported its highest-ever annual revenue of ₹1,069 crore and nearly doubled FY26 PAT to ₹142 crore.

What Happened ?

Juniper Hotels Limited announced audited standalone and consolidated financial results for Q4 and FY26 ended March 31, 2026.

Key developments during the year include:

- Record FY26 total income crossing ₹1,000 crore for the first time.

- EBITDA improved significantly due to operational leverage and cost efficiencies.

- PAT nearly doubled YoY reflecting stronger profitability.

- Portfolio ARR and RevPAR improved on sustained luxury hospitality demand.

- The company maintained strong occupancy levels at 81%.

- Juniper secured a Letter of Award from DDA for development of a ~500-key luxury hotel project in Dwarka, New Delhi near Yashobhoomi and Delhi International Airport.

- Westin Bengaluru Phase I is expected to become operational by Q2 FY27.

- The company plans to add more than 1,400 keys over the next four years through multiple development projects.

Management highlighted strong performance from:

- Grand Hyatt Mumbai

- Andaz Delhi

- Hyatt Regency Ahmedabad

The company stated that disciplined capital allocation and operational focus continue to support long-term growth opportunities.

Key Details

Q4 FY26 and FY26 Business & Financial Highlights:

- FY26 total income reached:

- ₹1,069.1 crore.

- FY26 revenue growth:

- 10% YoY.

- Q4 FY26 total income:

- ₹306.8 crore.

- FY26 EBITDA:

- ₹444 crore.

- FY26 EBITDA growth:

- 21% YoY.

- FY26 EBITDA margin:

- Expanded to 42%.

- Q4 FY26 EBITDA:

- ₹138 crore.

- FY26 PAT:

- ₹141.6 crore.

- FY26 PAT growth:

- 99% YoY.

- Q4 FY26 PAT:

- ₹50.4 crore.

- Sixth consecutive PAT-positive quarter achieved.

- Portfolio ARR:

- Increased 8% YoY to ₹13,457.

- Occupancy:

- Maintained at 81%.

- RevPAR:

- Improved from ₹8,165 to ₹8,982 in FY26.

- New Delhi expansion:

- Received DDA Letter of Award for ~500-key luxury hotel project in Dwarka.

- Bengaluru expansion:

- Westin Bengaluru Phase I expected operational by Q2 FY27.

- Growth pipeline:

- More than 1,400 additional hotel keys planned over next four years.

- Current portfolio:

- 1,895 keys including serviced apartments across 7 hotels.

- Major operational contributors:

- Grand Hyatt Mumbai.

- Andaz Delhi.

- Hyatt Regency Ahmedabad.

Note:

- The company’s improving occupancy, ARR growth, stronger margins, and aggressive expansion pipeline indicate continued momentum in India’s premium hospitality sector.

Risk Analysis

Summary:

- Despite strong operating performance, the hospitality business remains exposed to economic cycles, travel demand fluctuations, project execution timelines, and luxury segment competition.

Key Risks:

- Hospitality demand may weaken during economic slowdowns.

- New hotel projects could face regulatory or construction delays.

- Rising operating costs may pressure margins.

- Dependence on premium travel and corporate demand remains high.

- Geopolitical uncertainty could impact international travel flows.

- Expansion projects may require significant capital deployment.

Worst Case Scenario:

- If demand softens or expansion execution gets delayed, occupancy levels and profitability growth may moderate over the coming quarters.

Risk Level: Medium

Company Commentary

- Management stated FY26 was a landmark year with record bookings and strong cash generation.

- The company highlighted highest-ever annual revenue exceeding ₹1,000 crore.

- Juniper Hotels reported strong demand across existing hotel portfolio.

- Management emphasized disciplined capital allocation and operational focus.

- The company stated that Westin Bengaluru and upcoming Delhi projects strengthen long-term growth visibility.

- Management expects continued growth opportunities in India’s luxury hospitality sector.

Official Exchange Filing: Juniper Hotels Limited