Quarterly & Annual Financial Results

Hindustan Foods Delivers Record FY26 Performance; Guides FY27 PAT at ₹200–220 Crore

NSE

hndfds

BSE

519126

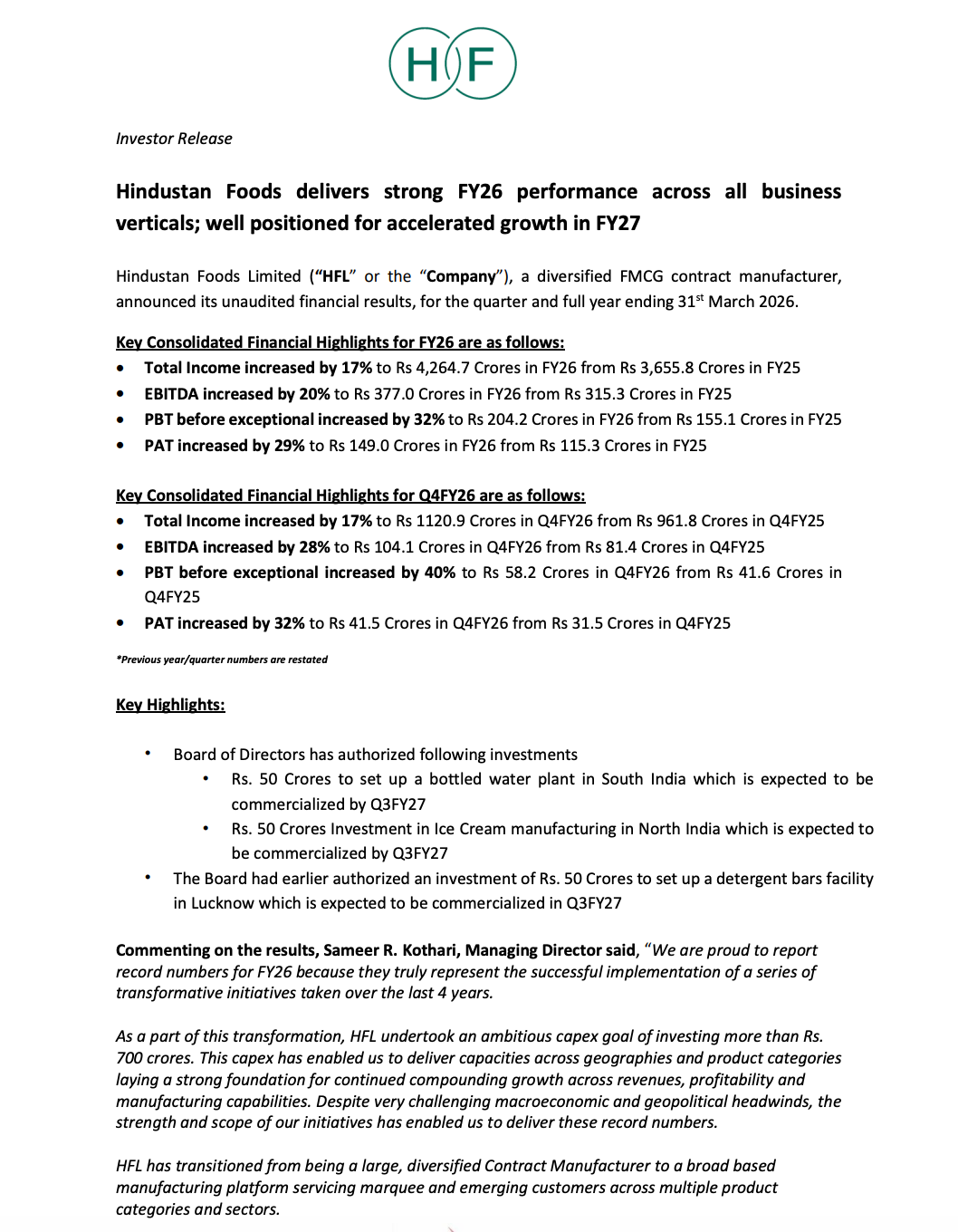

Hindustan Foods Limited (HFL) reported strong FY26 financial performance across business verticals with double-digit growth in revenue, EBITDA, and profitability. The company highlighted record annual PAT, strong operational execution, commercialization of major capex investments, and confidence in delivering FY27 PAT guidance of ₹200–220 crore.

PRICE-SENSITIVE TRIGGER

Event: Hindustan Foods announced FY26 and Q4 FY26 financial performance along with operational updates, capex commercialization progress, and FY27 profitability guidance.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: HFL delivered record FY26 PAT of ₹149 crore, strong EBITDA growth, improving operational leverage, and guided further profitability expansion in FY27 supported by new capacity ramp-up.

Key Metrics:

- FY26 Total Income: ₹4,264.7 crore, up 17% YoY.

- FY26 EBITDA: ₹377.0 crore, up 20% YoY.

- FY26 PBT (Before Exceptional Items): ₹204.2 crore, up 32% YoY.

- FY26 PAT: ₹149.0 crore, up 29% YoY.

- FY25 Total Income: ₹3,655.8 crore.

- FY25 EBITDA: ₹315.3 crore.

- FY25 PBT (Before Exceptional Items): ₹155.1 crore.

- FY25 PAT: ₹115.3 crore.

- Q4 FY26 Total Income: ₹1,120.9 crore, up 17% YoY.

- Q4 FY26 EBITDA: ₹104.1 crore, up 28% YoY.

- Q4 FY26 PBT (Before Exceptional Items): ₹58.2 crore, up 40% YoY.

- Q4 FY26 PAT: ₹41.5 crore, up 32% YoY.

- Q4 FY25 Total Income: ₹961.8 crore.

- Q4 FY25 EBITDA: ₹81.4 crore.

- Q4 FY25 PBT (Before Exceptional Items): ₹41.6 crore.

- Q4 FY25 PAT: ₹31.5 crore.

- Gross Block Including CWIP & Capital Advances: Over ₹1,800 crore.

- Net Debt-to-Equity Ratio: 0.84x.

- FY27 PAT Guidance: ₹200–220 crore.

Highlight Metric:

- Hindustan Foods delivered its highest-ever annual PAT of ₹149 crore in FY26 and guided FY27 PAT in the range of ₹200–220 crore backed by improving utilization and operating leverage.

What Happened ?

Hindustan Foods Limited announced strong FY26 and Q4 FY26 financial performance driven by broad-based growth across manufacturing verticals, operational execution, and recently commercialized capacities.

For FY26, total income increased 17% YoY to ₹4,264.7 crore while EBITDA rose 20% YoY to ₹377 crore. Profit before exceptional items grew 32% YoY to ₹204.2 crore and PAT increased 29% YoY to ₹149 crore, representing the highest annual PAT reported by the company.

Q4 FY26 also delivered strong growth momentum with total income rising 17% YoY to ₹1,120.9 crore and EBITDA increasing 28% YoY to ₹104.1 crore. Quarterly PAT increased 32% YoY to ₹41.5 crore.

Management highlighted that FY26 marked commercialization of the largest investment cycle in the company’s history, with gross block including capital work-in-progress and advances crossing ₹1,800 crore.

The company also announced new investments across bottled water, ice cream manufacturing, and detergent bars facilities expected to be commercialized by Q3 FY27.

HFL maintained confidence in achieving FY27 PAT guidance of ₹200–220 crore supported by improving utilization across newly commissioned facilities and continued operating leverage.

Key Details

FY26 Financial Performance:

- FY26 total income increased 17% YoY to ₹4,264.7 crore.

- FY26 EBITDA rose 20% YoY to ₹377 crore.

- FY26 PBT before exceptional items increased 32% YoY to ₹204.2 crore.

- FY26 PAT increased 29% YoY to ₹149 crore.

- FY26 represented the highest annual PAT reported by the company.

- Profitability growth outpaced revenue growth indicating improving operating leverage.

- Management attributed performance to successful execution of long-term transformation initiatives.

Note:

- The company delivered strong earnings growth despite macroeconomic and geopolitical headwinds during FY26.

Q4 FY26 Operational Performance:

- Q4 FY26 total income increased 17% YoY to ₹1,120.9 crore.

- Q4 FY26 EBITDA rose 28% YoY to ₹104.1 crore.

- Q4 FY26 PBT before exceptional items increased 40% YoY to ₹58.2 crore.

- Q4 FY26 PAT increased 32% YoY to ₹41.5 crore.

- Beverage and ice cream divisions delivered record volume growth during the quarter.

- Smooth commissioning of newer factories supported operational performance.

- Recently acquired businesses contributed positively to growth.

- Strategic inventory build-up helped manage geopolitical supply chain disruptions.

Note:

- Quarterly profitability expansion reflected benefits from scale efficiencies and stronger utilization across manufacturing facilities.

Capex Expansion & Manufacturing Investments:

- HFL commercialized its largest-ever investment cycle during FY26.

- Gross block including CWIP and capital advances crossed ₹1,800 crore by March 2026.

- The Board approved:

- ₹50 crore investment for bottled water plant in South India.

- ₹50 crore investment for ice cream manufacturing in North India.

- Both projects are expected to be commercialized by Q3 FY27.

- The Board had earlier approved ₹50 crore investment for a detergent bars facility in Lucknow.

- The detergent facility is also expected to be commercialized by Q3 FY27.

- Management stated that recently commissioned assets are expected to improve utilization and earnings going forward.

Note:

- The company is entering a utilization-led phase after completing a major capex cycle over the past four years.

Management Outlook & FY27 Guidance:

- HFL guided FY27 PAT in the range of ₹200–220 crore.

- Management expects improving operating leverage across facilities.

- Certain businesses will transition from gross to net revenue recognition from Q3 FY27 onward.

- The accounting transition is not expected to impact absolute profitability.

- Revenue reporting for affected businesses may appear moderated post transition.

- Adjusted ROCE remains above the company’s internal threshold of 18%.

- Net debt-to-equity ratio remains comfortable at 0.84x.

- Management expects sustained profitable growth supported by stronger utilization and manufacturing diversification.

Note:

- FY27 is expected to focus on scaling recently commissioned capacities and improving return metrics after peak investment phase completion.

Risk Analysis

Summary:

- Despite strong operational momentum, HFL remains exposed to raw material inflation, working capital pressure, utilization ramp-up risks, and geopolitical supply chain disruptions.

Key Risks:

- GST-related duty inversion continued impacting working capital.

- Geopolitical conditions required higher inventory buffers.

- LPG shortages temporarily affected certain factories.

- Footwear division faced pressure from petrochemical-linked raw material inflation.

- Large capex commercialization requires sustained utilization growth.

- Transition to net revenue recognition may affect reported topline visibility.

- Rising working capital intensity may pressure cash flows temporarily.

Worst Case Scenario:

- If utilization ramps slower than expected or raw material inflation persists, HFL could face pressure on margins, cash conversion, and return ratios despite higher installed capacity.

Risk Level: Medium

Company Commentary

- FY26 was described as another year of record financial delivery.

- Management stated that the company surpassed its annual PAT guidance.

- HFL remains confident in delivering FY27 PAT guidance of ₹200–220 crore.

- Recently commissioned assets and improving utilization are expected to drive future growth.

- The company highlighted disciplined capital allocation despite peak investment cycle execution.

- Manufacturing capabilities across product categories have expanded significantly.

- HFL believes its manufacturing network is now more diversified and scalable than ever before.

Official Exchange Filing: Hindustan Foods Limited