Capacity Expansion / Strategic Acquisition

Dalmia Bharat Acquires 5.2 MnTPA Cement Capacity from Jaiprakash Associates; Capacity to Rise to 54.7 MnTPA

NSE

dalbharat

BSE

542216

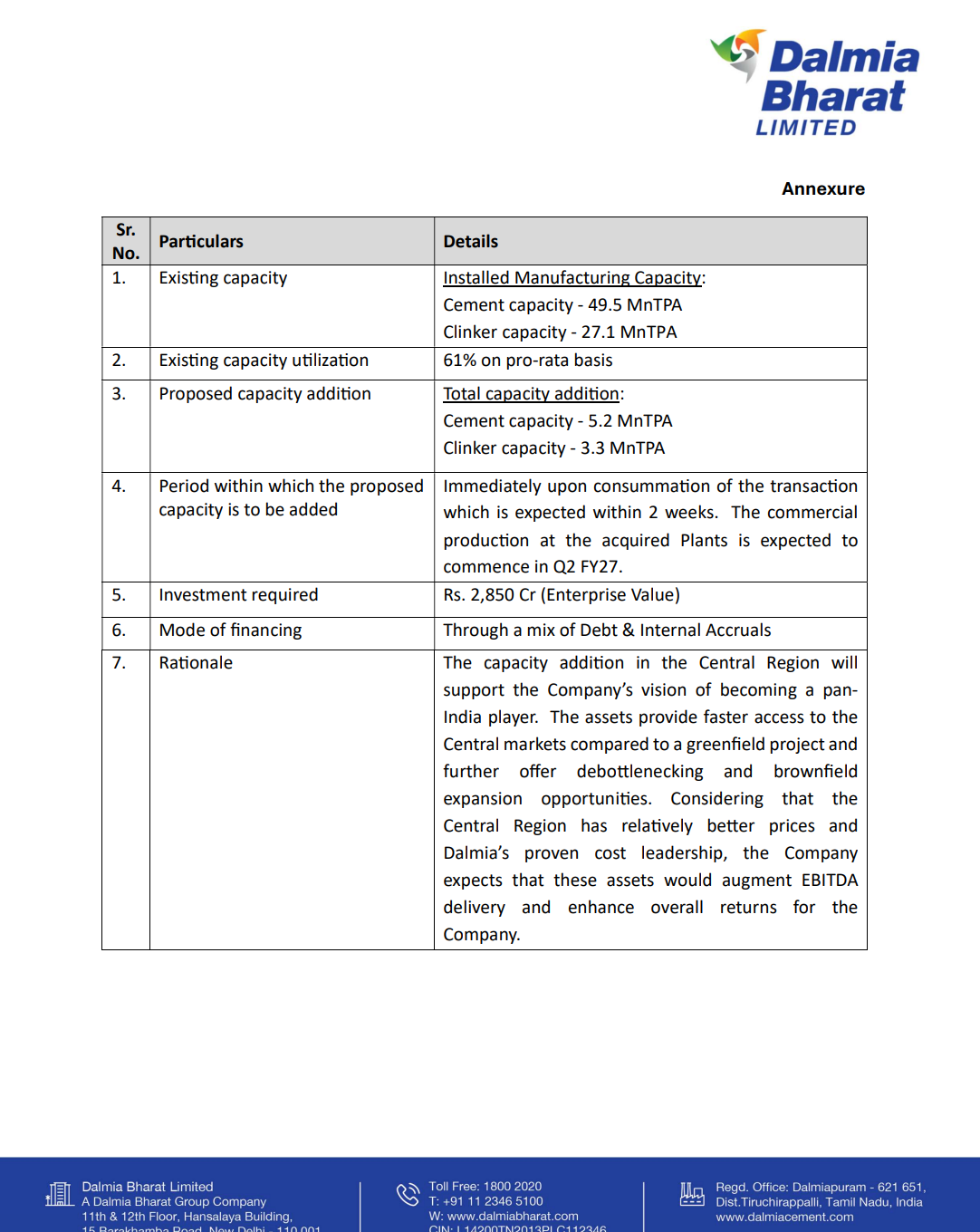

Dalmia Cement (Bharat) Limited, a wholly owned subsidiary of Dalmia Bharat Limited, executed a Business Transfer Agreement to acquire cement assets from Jaiprakash Associates Limited and Adani Infra (India) Limited for an enterprise value of ₹2,850 crore. The acquisition adds 5.2 MnTPA cement capacity and 3.3 MnTPA clinker capacity across Madhya Pradesh and Uttar Pradesh, strengthening Dalmia Bharat’s position in the Central India cement market.

PRICE-SENSITIVE TRIGGER

Event: Dalmia Bharat executed a Business Transfer Agreement to acquire cement manufacturing assets in Central India from Jaiprakash Associates and Adani Infra.

Type: Capacity Expansion / Strategic Acquisition

Impact: Positive

Immediate Effect: The acquisition will increase Dalmia Bharat’s cement capacity from 49.5 MnTPA to 54.7 MnTPA and strengthen its Central India market presence.

Key Metrics:

- Enterprise Value of Acquisition: ₹2,850 crore.

- Cement Capacity Acquired: 5.2 MnTPA.

- Clinker Capacity Acquired: 3.3 MnTPA.

- Thermal Power Capacity Included: 99 MW.

- Current Cement Capacity: 49.5 MnTPA.

- Post-Acquisition Cement Capacity: 54.7 MnTPA.

- Target Cement Capacity by Q2-Q3 FY28: 66.7 MnTPA.

- Existing Capacity Utilisation: 61% on pro-rata basis.

- Expected Deal Closure: Within two weeks.

- Commercial Production Start: Expected in Q2 FY27.

- Refurbishment Capex: Approximately ₹300 crore within one year.

- Efficiency Capex including WHRS: Approximately ₹250 crore over two years.

- Financing Structure: Mix of debt and internal accruals.

- Net Debt to EBITDA: Expected to remain comfortably below 2x.

- Integrated Plant Location: Rewa, Madhya Pradesh.

- Grinding Units: Chunar and Churk, Uttar Pradesh.

- Blending Unit: Sadwa, Uttar Pradesh.

Highlight Metric:

- Dalmia Bharat acquired 5.2 MnTPA cement capacity and 3.3 MnTPA clinker capacity in Central India for ₹2,850 crore, accelerating its pan-India expansion strategy and strengthening its market access in high-growth cement regions.

What Happened ?

Dalmia Cement (Bharat) Limited (DCBL), a wholly owned subsidiary of Dalmia Bharat Limited, executed a Business Transfer Agreement with Jaiprakash Associates Limited (JAL) and Adani Infra (India) Limited for acquisition of cement assets located in Madhya Pradesh and Uttar Pradesh.

The acquisition includes cement plants at Rewa, Churk, Chunar and Sadwa with combined cement capacity of 5.2 MnTPA and clinker capacity of 3.3 MnTPA. The transaction also includes 99 MW thermal power capacity and railway siding infrastructure.

The deal is valued at an enterprise value of ₹2,850 crore and is expected to be consummated within two weeks. Commercial production from the acquired facilities is expected to commence in Q2 FY27.

The company stated that the acquisition provides faster market access to Central India compared to a greenfield project while also offering debottlenecking and brownfield expansion opportunities. Management highlighted that the acquired assets are located in regions with relatively stronger pricing dynamics and lower per-capita cement consumption, creating long-term growth potential.

Dalmia Bharat expects the transaction to support its strategy of becoming a pan-India cement player while enhancing EBITDA generation and return ratios through operational efficiencies and cost leadership initiatives.

Key Details

Acquired Asset Portfolio:

- The acquisition includes four cement assets across Madhya Pradesh and Uttar Pradesh.

- Rewa integrated unit includes:

- Cement capacity of 1.1 MnTPA

- Clinker capacity of 3.3 MnTPA

- 62 MW thermal power plant

- Railway siding

- Limestone reserves exceeding 100 MnT

- Chunar grinding unit includes:

- Cement capacity of 2.5 MnTPA

- 37 MW thermal power plant

- Railway siding

- Churk grinding unit has:

- Cement capacity of 1.0 MnTPA

- Common railway siding infrastructure

- Sadwa blending unit has:

- Cement capacity of 0.6 MnTPA

- Assets also provide future debottlenecking opportunities:

- Additional clinker potential of 0.5–0.7 MnTPA

- Additional cement potential of 1.5–2.0 MnTPA

Note:

- The acquisition provides Dalmia Bharat immediate operating footprint expansion in strategically important Central India markets.

Strategic & Operational Benefits:

- The acquisition strengthens Dalmia Bharat’s Central India market presence.

- Central India markets offer:

- Strong pricing environment

- Large population base

- Significant state infrastructure spending

- Low per-capita cement consumption

- The transaction accelerates pan-India expansion strategy.

- Existing familiarity with assets from earlier tolling arrangements may support faster ramp-up.

- Brownfield and debottlenecking opportunities reduce expansion lead time compared to greenfield projects.

- Proximity to Dalmia’s captive limestone mines in Satna improves raw material integration.

- Market diversification could reduce regional business volatility.

Note:

- Management positioned the transaction as a strategically superior alternative to greenfield capacity creation in Central India.

Transaction Structure & Expansion Roadmap:

- The acquisition is structured as a slump sale on a “clean slate” basis.

- Financing will be through:

- Debt

- Internal accruals

- Net debt-to-EBITDA is expected to remain below 2x.

- Refurbishment capex of approximately ₹300 crore will be incurred within one year.

- Additional efficiency capex including WHRS of around ₹250 crore will be spent over two years.

- Post acquisition, cement capacity will rise to 54.7 MnTPA.

- Ongoing projects at:

- Belgaum

- Pune

- Kadapa

will increase cement capacity to 66.7 MnTPA by Q2-Q3 FY28.

- Clinker capacity is expected to rise from 27.1 MnTPA to 37.6 MnTPA by FY28.

Note:

- The acquisition forms part of Dalmia Bharat’s broader long-term manufacturing scale-up strategy across India.

Risk Analysis

Summary:

- While the acquisition significantly strengthens Dalmia Bharat’s market position in Central India, execution, integration, and refurbishment-related risks remain relevant over the near term.

Key Risks:

- Successful integration of acquired assets remains critical.

- Refurbishment and efficiency capex execution could impact timelines and costs.

- Demand slowdown in Central India may affect utilization ramp-up.

- Debt-funded acquisition increases financial leverage exposure.

- Operational turnaround of acquired facilities may take longer than expected.

- Cement pricing volatility could impact EBITDA realization.

- Regulatory and operational approvals remain necessary for full transition.

Worst Case Scenario:

- If integration delays, refurbishment overruns, or weaker cement demand emerge simultaneously, Dalmia Bharat could face slower-than-expected capacity utilization and lower acquisition returns.

Risk Level: Medium

Company Commentary

- Management described the acquisition as a major milestone in Dalmia Bharat’s pan-India expansion journey.

- The company believes the assets provide faster market access than greenfield expansion.

- Dalmia Bharat expects the assets to enhance EBITDA generation and return ratios.

- Existing familiarity with the acquired plants is expected to support faster operational ramp-up.

- Management remains confident in leveraging cost leadership and operational efficiencies across the acquired facilities.

- The company expects commercial production to commence in Q2 FY27.

Official Exchange Filing: Dalmia Bharat Limited