Quarterly & Annual Financial Results

Ashoka Buildcon Reports Strong FY26 PAT Growth; Order Book Stands at ₹15,312 Crore

NSE

ashoka

BSE

533271

Ashoka Buildcon Limited reported audited FY26 and Q4 FY26 financial results supported by strong execution across EPC, HAM, railways, and power transmission businesses. The company maintained a robust order book of ₹15,312 crore and announced multiple domestic and international project wins across Saudi Arabia, Angola, Bihar, Maharashtra, and Liberia.

PRICE-SENSITIVE TRIGGER

Event: Ashoka Buildcon announced audited FY26 financial results along with major order wins, project updates, and operational developments.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company reported strong FY26 PAT growth, maintained a diversified infrastructure order book exceeding ₹15,000 crore, and secured multiple new domestic and international infrastructure contracts.

Key Metrics:

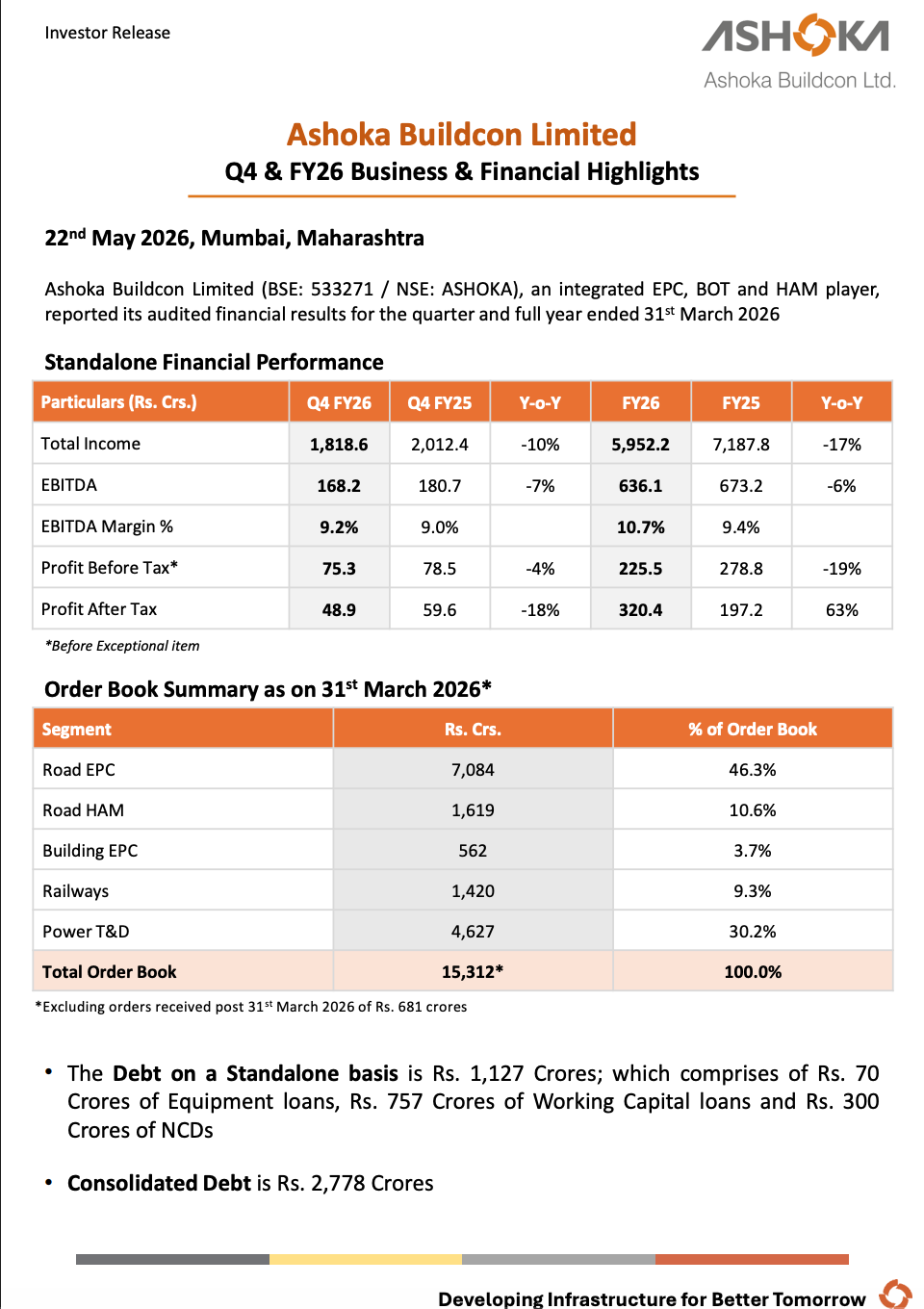

- FY26 Total Income: ₹5,952.2 crore, down 17% YoY.

- FY26 EBITDA: ₹636.1 crore, down 6% YoY.

- FY26 EBITDA Margin: 10.7% versus 9.4% in FY25.

- FY26 Profit Before Tax: ₹225.5 crore, down 19% YoY.

- FY26 PAT: ₹320.4 crore, up 63% YoY.

- Q4 FY26 Total Income: ₹1,818.6 crore, down 10% YoY.

- Q4 FY26 EBITDA: ₹168.2 crore, down 7% YoY.

- Q4 FY26 EBITDA Margin: 9.2% versus 9.0% in Q4 FY25.

- Q4 FY26 Profit Before Tax: ₹75.3 crore, down 4% YoY.

- Q4 FY26 PAT: ₹48.9 crore, down 18% YoY.

- Order Book as on March 31, 2026: ₹15,312 crore.

- Road EPC Order Book: ₹7,084 crore.

- Power T&D Order Book: ₹4,627 crore.

- Railways Order Book: ₹1,420 crore.

- Road HAM Order Book: ₹1,619 crore.

- Building EPC Order Book: ₹562 crore.

- Standalone Debt: ₹1,127 crore.

- Consolidated Debt: ₹2,778 crore.

Highlight Metric:

- Ashoka Buildcon reported 63% YoY growth in FY26 PAT to ₹320.4 crore while maintaining a diversified order book of over ₹15,000 crore across roads, power, railways, and EPC infrastructure segments.

What Happened ?

Ashoka Buildcon Limited announced audited standalone and consolidated financial results for Q4 FY26 and FY26, highlighting strong profitability, operational execution, and order inflows across infrastructure verticals.

For FY26, total income declined 17% YoY to ₹5,952.2 crore while EBITDA fell 6% YoY to ₹636.1 crore. However, EBITDA margin improved to 10.7% compared to 9.4% in FY25, reflecting operational efficiency improvements.

Profit after tax for FY26 increased sharply by 63% YoY to ₹320.4 crore despite lower revenue and EBITDA performance.

The company maintained a strong order book of ₹15,312 crore led by Road EPC, Power T&D, Railways, and HAM projects.

Ashoka Buildcon also announced several new domestic and international project wins including contracts in Saudi Arabia, Bihar, Angola, Liberia, and Maharashtra.

Additionally, the company received COD milestones for its Karnataka HAM road project, updated timelines for HAM SPV monetization, and disclosed reaffirmation of credit ratings with removal from “Rating Watch”.

Key Details

FY26 & Q4 Financial Performance:

- FY26 total income declined 17% YoY to ₹5,952.2 crore.

- FY26 EBITDA declined 6% YoY to ₹636.1 crore.

- EBITDA margin improved to 10.7% from 9.4% in FY25.

- FY26 PAT increased 63% YoY to ₹320.4 crore.

- Q4 FY26 total income declined 10% YoY to ₹1,818.6 crore.

- Q4 FY26 EBITDA stood at ₹168.2 crore.

- Q4 FY26 EBITDA margin improved marginally to 9.2%.

- Q4 FY26 PAT declined 18% YoY to ₹48.9 crore.

- Profitability performance remained stronger than topline trends due to margin improvements and execution efficiency.

Note:

- Despite moderation in revenue, the company demonstrated stronger earnings resilience through improved operational margins.

Order Book & Segment Mix:

- Total order book stood at ₹15,312 crore as of March 31, 2026.

- Road EPC contributed:

- ₹7,084 crore

- 46.3% of order book

- Power T&D contributed:

- ₹4,627 crore

- 30.2% of order book

- Road HAM projects contributed:

- ₹1,619 crore

- 10.6% of order book

- Railways contributed:

- ₹1,420 crore

- 9.3% of order book

- Building EPC contributed:

- ₹562 crore

- 3.7% of order book

Note:

- The order book remains diversified across multiple infrastructure segments with Roads and Power T&D dominating the execution pipeline.

Major Project Wins & International Expansion:

- Ashoka Buildcon’s Saudi Arabia subsidiary secured LOA from Diriyah Company for hotel construction works worth SAR 717 million.

- The company’s attributable project share in the Saudi JV stands at approximately ₹846.4 crore.

- A JV project in Bihar secured EPC bridge construction LOA worth ₹474.4 crore.

- The company secured a Liberia road infrastructure project worth $45 million.

- Ashoka Buildcon received Letter of Contract Acceptance from Angola Ministry of Energy & Water for a $72 million distribution rehabilitation project.

- The company and RailTel consortium received LOI for Maharashtra IGR office modernization project worth approximately ₹1,136 crore.

- Multiple projects have execution periods ranging from 24 to 60 months.

Note:

- The company continues expanding internationally while maintaining strong domestic infrastructure order momentum.

Operational & Corporate Updates:

- Ashoka Buildcon extended completion timeline for sale of remaining six HAM SPVs till June 30, 2026.

- The company received COD for sections of the Tumkur-Shivamogga HAM project in Karnataka.

- Rights issue allotments were completed across multiple wholly owned subsidiaries.

- Acuité reaffirmed:

- ACUITE AA (Stable)

- ACUITE A1+

- Both ratings were removed from “Rating Watch”.

- Standalone debt stood at ₹1,127 crore.

- Consolidated debt stood at ₹2,778 crore.

Note:

- Credit rating stabilization and COD milestones improve visibility on operational execution and financial stability.

Risk Analysis

Summary:

- While Ashoka Buildcon maintains a strong order pipeline and diversified infrastructure exposure, the company remains exposed to execution risks, working capital intensity, and project monetization timelines.

Key Risks:

- Revenue decline indicates moderation in execution pace during FY26.

- Infrastructure projects remain exposed to regulatory and execution delays.

- HAM SPV monetization timelines have already been extended.

- International projects introduce geopolitical and currency risks.

- Elevated debt levels may continue impacting balance sheet flexibility.

- Working capital requirements remain high across EPC and HAM businesses.

- Margin sustainability depends on timely project execution and cost control.

Worst Case Scenario:

- If project execution slows further or monetization timelines are delayed, Ashoka Buildcon could face pressure on cash flows, debt reduction plans, and profitability visibility.

Risk Level: Medium

Company Commentary

- Ashoka Buildcon highlighted strong execution across EPC, BOT, and HAM verticals.

- The company emphasized its diversified infrastructure order pipeline.

- Management continues focusing on domestic and international expansion opportunities.

- The company reaffirmed execution progress across roads, railways, power, and building EPC segments.

- Credit ratings were reaffirmed with removal from “Rating Watch”.

- COD milestones and project wins are expected to support future revenue visibility.

Official Exchange Filing: Ashoka Buildcon Limited