Quarterly & Annual Financial Results

Man Industries reports highest-ever consolidated EBITDA margins; standalone PAT surges 74% YoY in FY26

NSE

maninds

BSE

513269

Man Industries (India) Limited reported strong FY26 operational and profitability performance with record standalone and consolidated EBITDA margins. The company also completed the strategic acquisition of National Pipe Company (NPC), Saudi Arabia, strengthening its global pipeline manufacturing platform and positioning itself for large energy infrastructure opportunities.

PRICE-SENSITIVE TRIGGER

Event: Announcement of audited standalone and consolidated Q4 FY26 and FY26 financial results along with strategic acquisition update.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered strong profitability growth, margin expansion, robust order book visibility, and strengthened global manufacturing capabilities through the NPC acquisition.

Key Metrics:

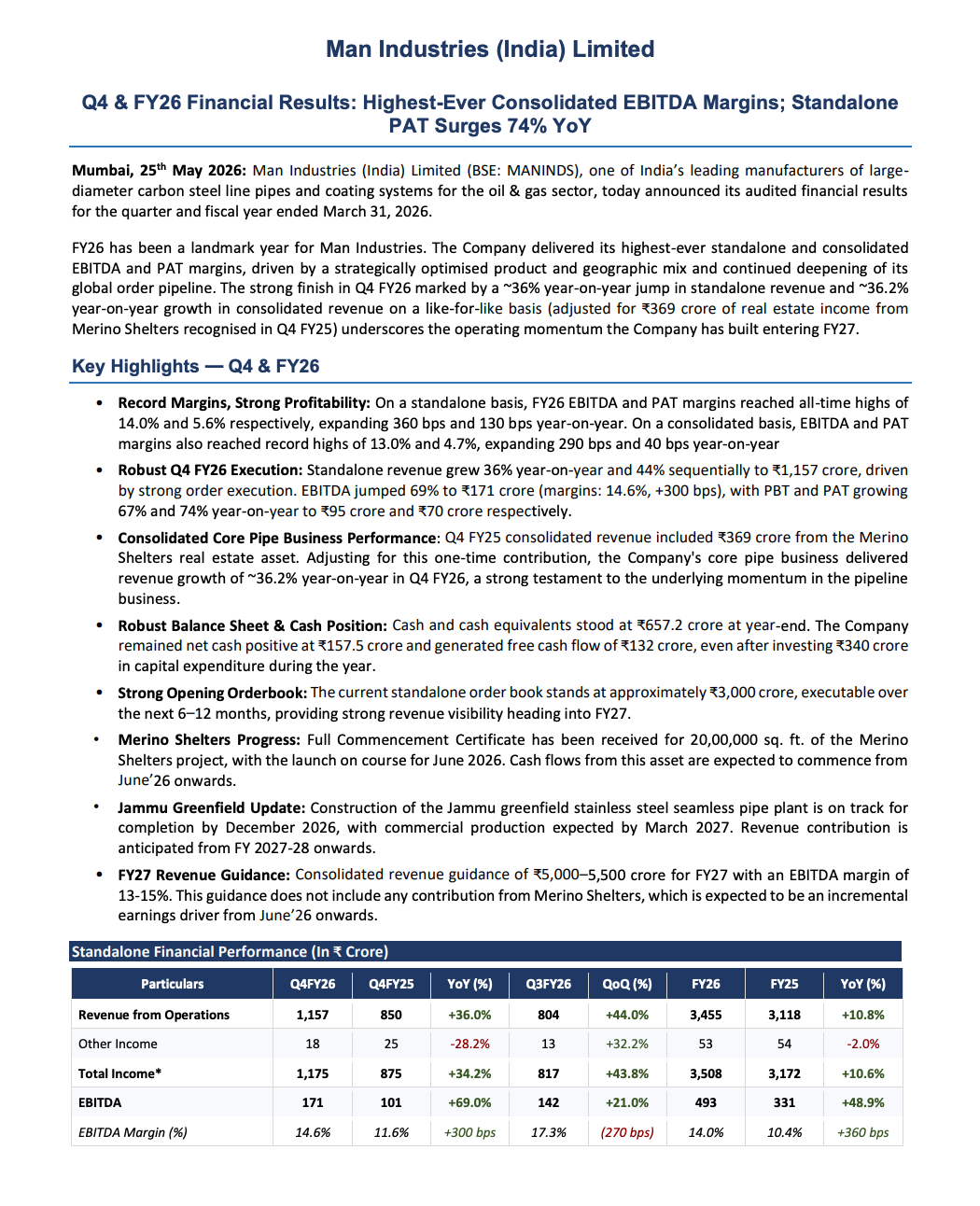

- Standalone Q4 FY26 Revenue: ₹1,157 crore

- Standalone Q4 Revenue Growth YoY: 36.0%

- Standalone FY26 Revenue: ₹3,455 crore

- Standalone FY26 Revenue Growth YoY: 10.8%

- Standalone Q4 FY26 EBITDA: ₹171 crore

- Standalone Q4 EBITDA Growth YoY: 69.0%

- Standalone FY26 EBITDA: ₹493 crore

- Standalone FY26 EBITDA Growth YoY: 48.9%

- Standalone FY26 EBITDA Margin: 14.0%

- Standalone FY25 EBITDA Margin: 10.4%

- Margin Expansion: 360 bps YoY

- Standalone Q4 FY26 PAT: ₹70 crore

- Standalone Q4 PAT Growth YoY: 74.1%

- Standalone FY26 PAT: ₹196 crore

- Standalone FY26 PAT Growth YoY: 42.8%

- Standalone FY26 PAT Margin: 5.6%

- Standalone FY25 PAT Margin: 4.3%

- Consolidated Q4 FY26 Revenue: ₹1,157 crore

- Consolidated FY26 Revenue: ₹3,564 crore

- Consolidated FY26 Revenue Growth YoY: 1.7%

- Consolidated FY26 EBITDA: ₹468 crore

- Consolidated FY26 EBITDA Growth YoY: 31.3%

- Consolidated FY26 EBITDA Margin: 13.0%

- Consolidated Margin Expansion: 290 bps YoY

- Consolidated FY26 PAT: ₹170 crore

- Consolidated FY26 PAT Growth YoY: 11.3%

- Cash & Cash Equivalents: ₹657.2 crore

- Net Cash Position: ₹157.5 crore

- Free Cash Flow Generated: ₹132 crore

- Standalone Order Book: Approximately ₹3,000 crore executable over next 6–12 months

- NPC Acquisition Value: USD 102 million (~₹1,000 crore)

Highlight:

- Label: Record Margin Performance

- Value: FY26 standalone EBITDA margin expanded to an all-time high of 14.0%, while standalone PAT surged 74% YoY in Q4 FY26.

What Happened ?

Man Industries (India) Limited announced its audited Q4 FY26 and FY26 financial results, reporting record profitability and strong operational momentum across standalone and consolidated businesses.

The company achieved all-time high standalone and consolidated EBITDA and PAT margins during FY26, supported by product mix optimization, operational leverage, and disciplined financial execution.

Q4 FY26 standalone revenue increased 36% year-on-year to ₹1,157 crore, driven by strong order execution. EBITDA rose 69% YoY to ₹171 crore, while PAT surged 74% YoY to ₹70 crore.

The company also completed the acquisition of Saudi Arabia-based National Pipe Company (NPC) through its wholly owned subsidiary MISIC for USD 102 million, significantly expanding its global manufacturing footprint.

Key Details

Strategic Growth Initiatives & Operational Updates:

- The acquisition of National Pipe Company (NPC), Saudi Arabia adds:

- 430,000 MTPA HSAW and LSAW pipe capacity

- Blue-chip customer relationships including Saudi Aramco

- Debt-free balance sheet with USD 83 million cash and liquid assets

- Management stated the NPC acquisition is EPS-accretive from Day 1.

- Combined with MAN Industries’ India capacity and Dammam coating facility, the acquisition creates an integrated cross-border pipeline solutions platform.

- The company is developing a greenfield stainless steel seamless pipe manufacturing facility in Jammu.

- Jammu facility construction remains on track for completion by December 2026, with commercial production expected by March 2027.

- Management guided FY27 consolidated revenue in the range of ₹5,000–5,500 crore with EBITDA margins of 13–15%.

- Guidance excludes expected revenue contribution from Merino Shelters, anticipated from June 2026 onward.

- Merino Shelters project received Full Commencement Certificate for 20,00,000 sq. ft. development.

- The company generated ₹132 crore free cash flow despite ₹340 crore capital expenditure during FY26.

- Strong operational momentum was supported by improved product mix, international diversification, and pipeline execution strength.

Note:

- Management indicated that FY26 marked an operational inflection point for the company, with strong execution visibility supported by international expansion and a healthy order pipeline.

Risk Analysis

Summary:

- Despite strong profitability and growth momentum, the company remains exposed to commodity cycles, execution risks in international projects, integration risks from acquisitions, and global energy infrastructure demand volatility.

Key Risks:

- Revenue visibility remains linked to oil & gas and energy infrastructure capital expenditure cycles.

- Successful integration of NPC Saudi Arabia operations remains critical for expected synergies and profitability improvement.

- Large capital expenditure commitments for the Jammu facility could impact cash flows if execution timelines are delayed.

- International operations expose the company to geopolitical, currency, and regulatory risks.

- Order execution delays or project cancellations may impact quarterly revenue recognition.

- Margin sustainability could be affected by steel price volatility and competitive pricing pressure.

Worst Case Scenario:

- Delays in large project execution, slower energy infrastructure spending, or unsuccessful integration of NPC could pressure margins, cash flows, and revenue growth in FY27.

Risk Level: Medium

Company Commentary

- Managing Director Nikhil Mansukhani stated that FY26 was a defining year with record EBITDA and PAT margins driven by optimized product mix and international expansion.

- Management highlighted that strong Q4 standalone performance demonstrated embedded operating leverage in the business model.

- The company emphasized that the NPC acquisition and Jammu expansion are building a more diversified and resilient platform for long-term growth.

- Management stated the standalone order book of approximately ₹3,000 crore provides strong revenue visibility entering FY27.

- The company indicated that foundations are now in place for sustained operational and financial scaling over the coming years.

Official Exchange Filing: Man Industries (India) Limited