Quarterly & Annual Financial Results

Kilburn Engineering Delivers Strong FY26 Performance with 48% Revenue Growth and Capacity Expansion

NSE

klbreng-b

BSE

522101

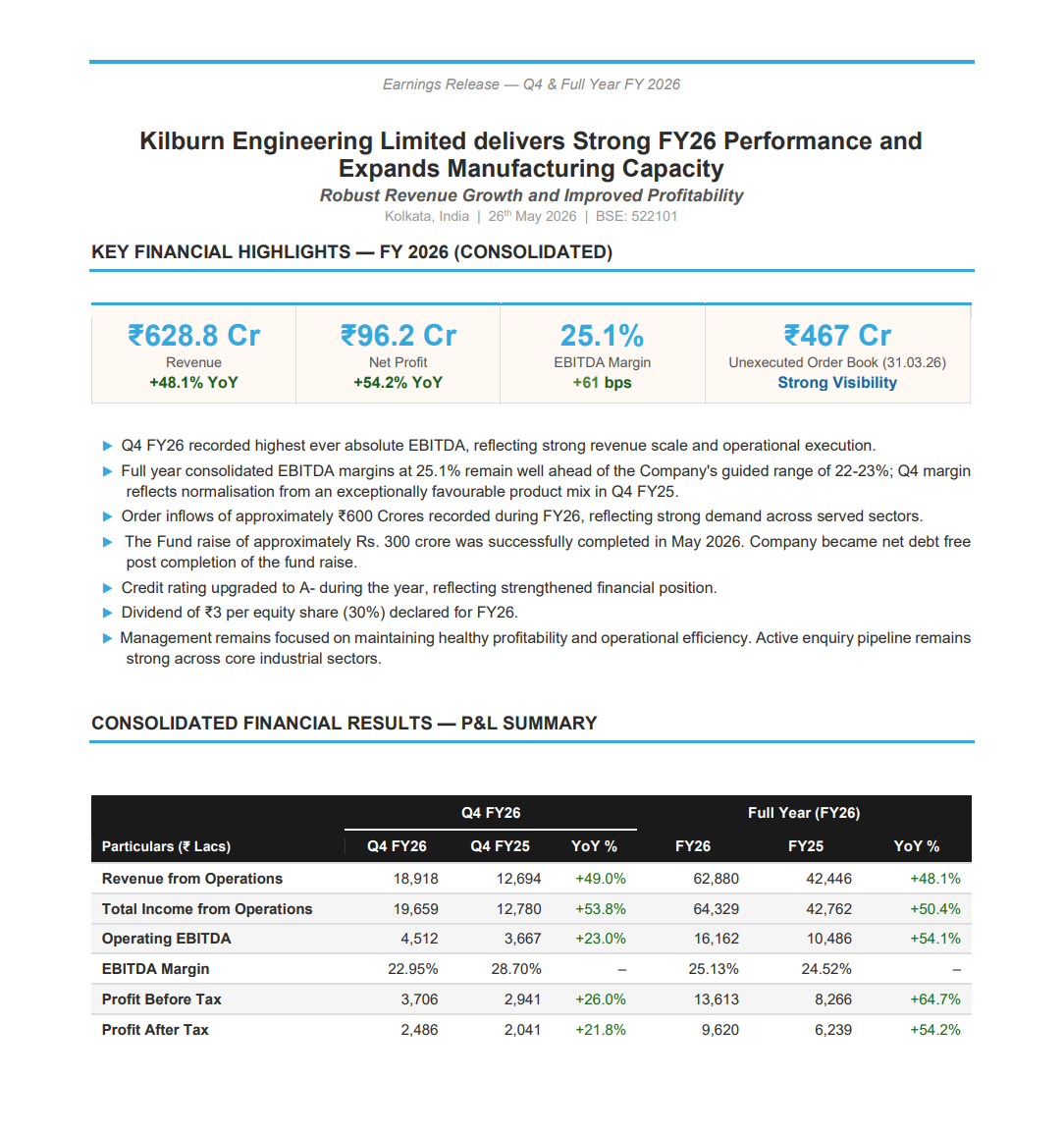

Kilburn Engineering Limited reported strong FY26 consolidated performance with revenue rising 48.1% YoY to ₹628.8 crore and PAT increasing 54.2% YoY to ₹96.2 crore. The company also expanded manufacturing capabilities, strengthened order inflows, completed a ₹300 crore fund raise and turned net debt free during FY26.

PRICE-SENSITIVE TRIGGER

Event: Announcement of audited Q4 and FY26 financial results along with operational and capacity expansion updates.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong revenue growth, margin expansion, improved profitability and healthy order inflows reinforce Kilburn Engineering’s execution momentum and long-term industrial manufacturing growth outlook.

Key Metrics:

- FY26 Consolidated Revenue: ₹628.8 crore | +48.1% YoY

- FY26 Net Profit: ₹96.2 crore | +54.2% YoY

- FY26 EBITDA: ₹161.6 crore | +54.1% YoY

- FY26 EBITDA Margin: 25.1% | +61 bps YoY

- FY26 Profit Before Tax: ₹136.1 crore | +64.7% YoY

- Q4 FY26 Revenue: ₹189.2 crore | +49.0% YoY

- Q4 FY26 EBITDA: ₹45.1 crore | +23.0% YoY

- Q4 FY26 PAT: ₹24.9 crore | +21.8% YoY

- Standalone FY26 Revenue: ₹448.3 crore | +33.6% YoY

- Standalone FY26 EBITDA: ₹119.4 crore | +30.8% YoY

- Standalone FY26 PAT: ₹69.1 crore | +26.0% YoY

- Unexecuted Order Book (31 March 2026): ₹467 crore

- FY26 Order Inflows: ~₹600 crore

- Dividend Declared: ₹3 per equity share

- Revenue Target FY28: ₹1,000 crore reaffirmed

Highlight:

- Highlight Label: Record FY26 Financial Performance

- Highlight Value: Consolidated revenue rose 48.1% YoY while PAT increased 54.2% YoY, supported by strong industrial demand, operational execution and expanded manufacturing capabilities.

What Happened ?

Kilburn Engineering Limited announced strong FY26 audited financial performance with robust growth across revenue, EBITDA and profitability metrics.

The company benefited from:

- Strong order inflows

- Improved operational execution

- Expansion of manufacturing infrastructure

- Better project conversion across industrial sectors

During FY26, the company:

- Successfully integrated M.E. Energy and Monga Strayfield operations

- Completed a ₹300 crore fund raise

- Became net debt free

- Expanded manufacturing and execution capabilities

- Maintained strong enquiry pipeline across process industries and energy-related sectors

Management also reaffirmed its FY28 revenue target of ₹1,000 crore with expected annual growth of 20–25%.

Key Details

Operational Expansion, Order Momentum & Strategic Growth:

- FY26 consolidated EBITDA margins remained at 25.1%, ahead of the company’s guided range of 22–23%.

- Q4 FY26 delivered the highest-ever absolute EBITDA for the company.

- Consolidated order inflows during FY26 stood at approximately ₹600 crore.

- Unexecuted order book as of March 31, 2026 stood at ₹467 crore, providing execution visibility.

- The company completed a ₹300 crore fund raise in May 2026 and became net debt free post transaction.

- Credit rating upgraded to:

- A-

- Significant progress made toward:

- Manufacturing infrastructure expansion

- Capacity enhancement

- Operational scale-up

- Engineering capability strengthening

- Integrated operations of:

- M.E. Energy

- Monga Strayfield

- Management highlighted healthy enquiry activity across sectors including:

- Nuclear

- Oil & gas

- Recycling of metals

- Fertilizers

- Carbon black

- Palm oil

- Steel & ferro alloys

- Textiles

- RF drying applications

- Revenue growth expected to remain weighted toward H2 FY27 due to geopolitical and logistics-related disruptions affecting project execution timelines.

- The company continues focusing on:

- Higher execution volumes

- Delivery efficiency

- Project handling capabilities

- Long-term manufacturing scale

Note:

- Kilburn Engineering’s combination of strong order inflows, debt-free balance sheet and industrial sector diversification strengthens visibility for sustained medium-term growth.

Risk Analysis

Summary:

- Despite strong financial momentum and healthy industrial demand, the company remains exposed to project execution cycles, industrial capex trends and geopolitical disruptions.

Key Risks:

- Project execution timelines may be affected by logistics and geopolitical disruptions.

- Industrial capital expenditure slowdown may impact order inflows.

- Margin sustainability depends on operational efficiency and execution discipline.

- Integration risks remain associated with acquired businesses.

- Revenue concentration toward H2 FY27 may create quarterly volatility.

Worst Case Scenario:

- Extended execution delays, industrial demand slowdown or operational inefficiencies could affect revenue realization, profitability and order conversion momentum.

Risk Level: Medium

Company Commentary

- Chairman Amritanshu Khaitan stated FY26 was a transformational year with strong growth in consolidated revenue, EBITDA and PAT.

- Management highlighted successful integration of acquired businesses which expanded the company’s capabilities across:

- Process equipment

- Energy systems

- RF drying technologies

- Managing Director Ranjit Lala stated the company continues strengthening execution capabilities and scaling manufacturing infrastructure.

- Management emphasized increasing opportunities across:

- Ferrous alloys

- Recycling of metals

- Process industries

- Energy systems

- The company reaffirmed:

- ₹1,000 crore revenue target by FY28

- 20–25% annual growth outlook

- Management stated confidence in sustaining long-term growth momentum due to:

- Strong balance sheet

- Debt-free position

- Healthy order backlog

- Expanded manufacturing capabilities

Official Exchange Filing: Kilburn Engineering Limited