Quarterly & Annual Financial Results

RIR Power Electronics Reports FY26 Revenue Growth, Strong Order Backlog and Advances Semiconductor Expansion Plans

NSE

not listed

BSE

517035

RIR Power Electronics Limited reported FY26 standalone revenue growth of 5.4% to ₹90.87 crore while continuing investments in semiconductor manufacturing and high-power electronics innovation. The company ended FY26 with an order backlog of approximately ₹17 crore, announced its first overseas order for SCR thyristors, and highlighted progress on its Silicon Carbide (SiC) semiconductor facility in Odisha. Despite revenue growth, profitability moderated due to lower margins during the year.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Financial Performance Announcement

Type: Quarterly & Annual Financial Results

Impact: Neutral

Immediate Effect: The company reported revenue growth and a strong improvement in quarterly profitability on a sequential basis, while simultaneously advancing strategic semiconductor and technology development initiatives.

Key Metrics:

FY26 Performance:

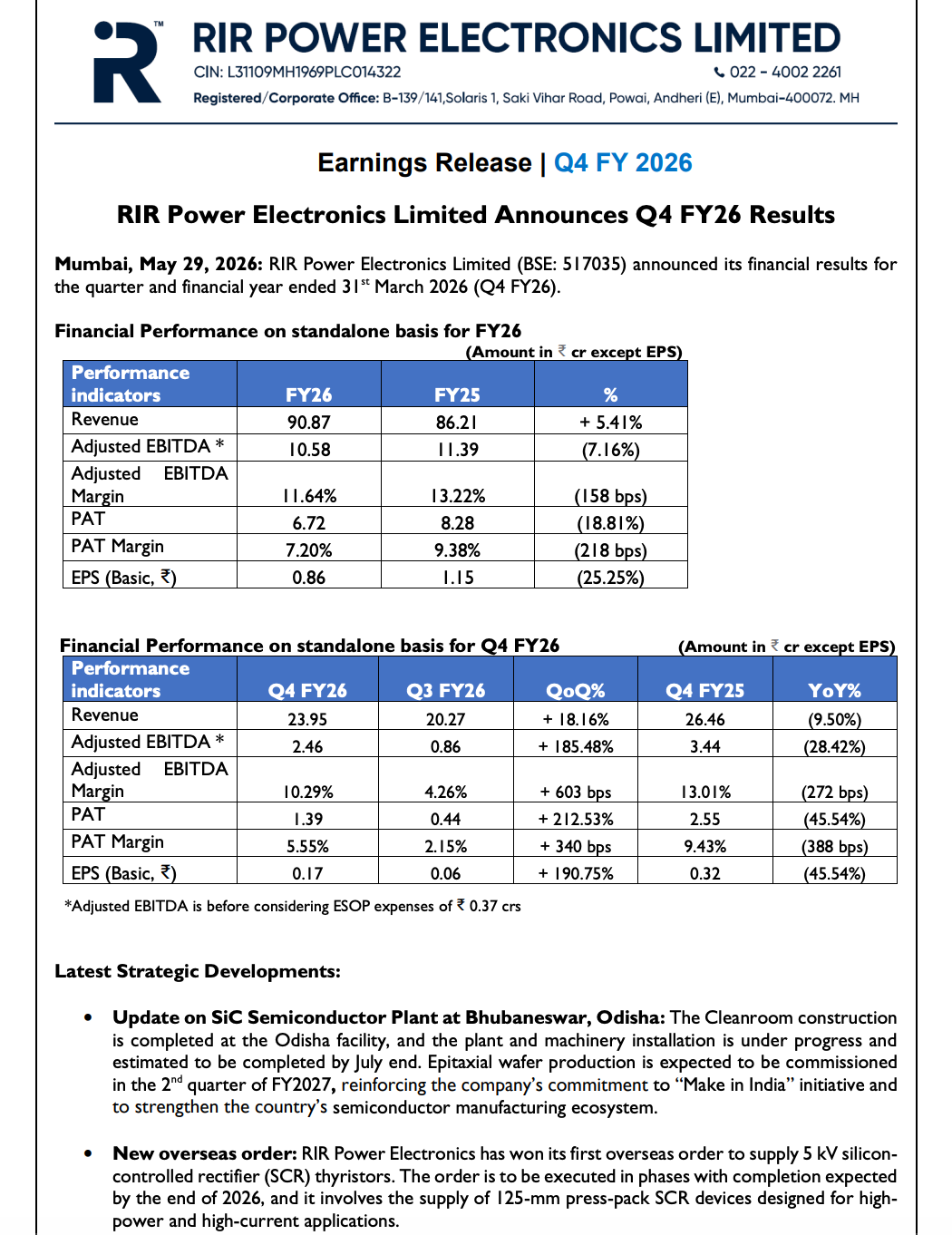

- Revenue: ₹90.87 crore (+5.41% YoY)

- Adjusted EBITDA: ₹10.58 crore (-7.16% YoY)

- Adjusted EBITDA Margin: 11.64% (down 158 bps YoY)

- PAT: ₹6.72 crore (-18.81% YoY)

- PAT Margin: 7.20% (down 218 bps YoY)

- EPS: ₹0.86 (-25.25% YoY)

Q4 FY26 Performance:

- Revenue: ₹23.95 crore (+18.16% QoQ, -9.50% YoY)

- Adjusted EBITDA: ₹2.46 crore (+185.48% QoQ, -28.42% YoY)

- Adjusted EBITDA Margin: 10.29% (+603 bps QoQ, -272 bps YoY)

- PAT: ₹1.39 crore (+212.53% QoQ, -45.54% YoY)

- PAT Margin: 5.55% (+340 bps QoQ, -388 bps YoY)

- EPS: ₹0.17 (+190.75% QoQ, -45.54% YoY)

Business Indicators:

- Order Backlog: Approximately ₹17 crore

- ESOP Expense Adjustment: ₹0.37 crore considered for adjusted EBITDA

Highlight:

- While FY26 profitability moderated, RIR Power Electronics achieved revenue growth, maintained a ₹17 crore order backlog, secured its first overseas order, and advanced its semiconductor manufacturing roadmap.

What Happened ?

RIR Power Electronics Limited announced its Q4 FY26 and FY26 results, reporting standalone revenue of ₹90.87 crore for FY26, an increase of 5.41% over FY25.

Profitability was impacted during the year, with adjusted EBITDA declining 7.16% YoY and PAT falling 18.81% YoY. However, Q4 FY26 showed a strong sequential recovery, with EBITDA increasing 185.48% QoQ and PAT rising more than threefold compared with Q3 FY26.

Beyond financial performance, the company reported meaningful strategic developments. Construction of the cleanroom at its Silicon Carbide (SiC) semiconductor facility in Odisha has been completed, while plant and machinery installation is underway. Epitaxial wafer production is expected to be commissioned during Q2 FY27.

The company also secured its first overseas order for 5 kV silicon-controlled rectifier (SCR) thyristors and announced development of a 25 kV–120 kA capacitor discharge vertically integrated semiconductor switch aimed at high-energy pulse power applications.

Management highlighted that the company enters FY27 with an order backlog of approximately ₹17 crore, providing revenue visibility for upcoming quarters.

Key Details

Operational & Strategic Developments:

- FY26 revenue increased to ₹90.87 crore.

- Company ended FY26 with order backlog of approximately ₹17 crore.

- Cleanroom construction completed at Odisha SiC semiconductor facility.

- Plant and machinery installation is currently underway.

- Epitaxial wafer production expected to commence in Q2 FY27.

- First overseas order received for 5 kV SCR thyristors.

- Overseas order execution expected to be completed by the end of 2026.

- Company developed a 25 kV–120 kA capacitor discharge semiconductor switch.

- Technology targets defence systems, medical equipment, pulse power systems and directed energy applications.

- Focus remains on semiconductor manufacturing, energy electronics and high-power device innovation.

- Strategic initiatives support India’s semiconductor and advanced electronics ecosystem.

Note:

- FY26 was characterized by continued investment in semiconductor capabilities and advanced power electronics technologies, positioning the company for future growth beyond its traditional product portfolio.

Risk Analysis

Summary:

- The company is investing in emerging semiconductor and high-power electronics opportunities, but commercialization timelines, execution risks, and profitability recovery remain key monitoring factors.

Key Risks:

- Semiconductor manufacturing projects involve execution and commissioning risks.

- New technology commercialization may require extended customer qualification cycles.

- Profitability remains below prior-year levels despite revenue growth.

- High-power electronics demand can be influenced by capital expenditure cycles.

- Overseas order execution introduces operational and customer acceptance risks.

- Margin recovery remains dependent on operating leverage and product mix improvement.

Worst Case Scenario:

- If semiconductor commissioning timelines are delayed or commercialization of new technologies takes longer than expected, expected growth and profitability improvement may be deferred.

Risk Level: Medium

Company Commentary

- Management described FY26 as a transformative year focused on scale, efficiency and customer relationships.

- The company highlighted development of the 25 kV–120 kA capacitor discharge semiconductor switch as a major innovation milestone.

- Management remains focused on execution excellence, technological innovation and profitable growth in FY27.

- The company stated that its ₹17 crore order backlog provides revenue visibility for upcoming quarters.

- Leadership believes the company is well positioned to participate in India’s semiconductor ambitions.

- Management remains focused on converting backlog into sustainable cash flows and shareholder value.

Official Exchange Filing: RIR Power Electronics Limited