Quarterly & Annual Financial Results

Veranda Learning Delivers First Full-Year Profit Since Listing; FY26 Revenue Rises 35% to ₹482 Crore

NSE

veranda

BSE

543514

Veranda Learning Solutions Limited reported strong FY26 performance with consolidated revenue growing 35% YoY to ₹482 crore and EBITDA surging 135% to ₹204 crore. The company achieved its first full-year PAT-positive performance since listing, reporting PAT of ₹129.7 crore versus a loss of ₹251.6 crore in FY25. Growth was driven by Commerce Test Prep, Government Test Prep and improving enrollment momentum across business segments.

PRICE-SENSITIVE TRIGGER

Event: Audited Q4 FY26 and FY26 Financial Results

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company reported record profitability improvement, strong enrollment growth, margin expansion, and completion of shareholder approval for its proposed commerce business demerger, strengthening strategic focus across education verticals.

Key Metrics:

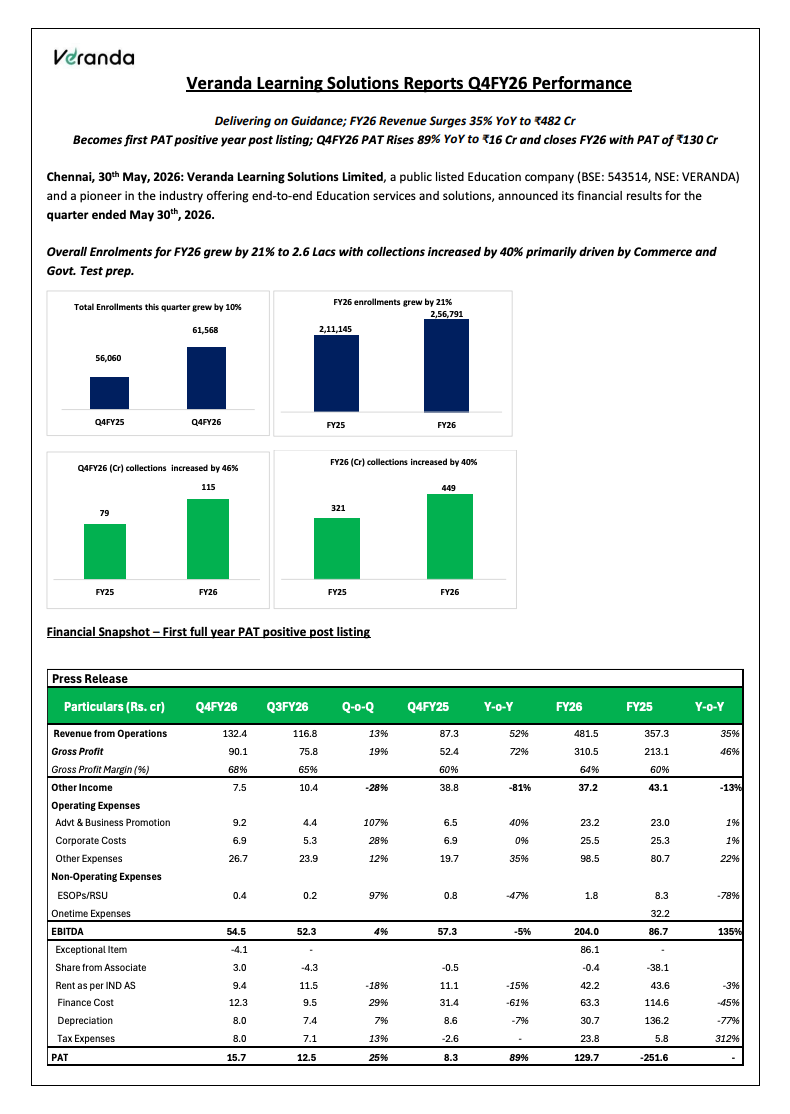

- FY26 Revenue from Operations: ₹481.5 crore (+35% YoY)

- FY26 Gross Profit: ₹310.5 crore (+46% YoY)

- FY26 Gross Margin: 64% vs 60% FY25

- FY26 EBITDA: ₹204.0 crore (+135% YoY)

- FY26 EBITDA Margin: 42.4% vs 24.3% FY25

- FY26 PAT: ₹129.7 crore vs loss of ₹251.6 crore FY25

- Q4 FY26 Revenue: ₹132.4 crore (+52% YoY)

- Q4 FY26 EBITDA: ₹54.5 crore

- Q4 FY26 PAT: ₹15.7 crore (+89% YoY)

- FY26 Enrollments: 2.57 lakh (+21% YoY)

- FY26 Collections: ₹449 crore (+40% YoY)

Highlight:

- Veranda delivered its first full-year PAT-positive performance since listing, reporting FY26 PAT of ₹129.7 crore while EBITDA more than doubled to ₹204 crore.

What Happened ?

Veranda Learning Solutions reported a strong FY26 performance driven by healthy enrollment growth, expansion of course offerings, improved operational efficiency and disciplined cost management.

The company achieved substantial profitability improvement, supported by higher revenue contribution from Commerce Test Prep and Government Test Prep segments. Gross margins expanded to 64%, while EBITDA margins improved significantly to 42.4%.

During FY26, Veranda expanded its educational ecosystem through new commerce virtual programs, offline geographic expansion, and new government test preparation offerings. The company also progressed its corporate restructuring journey by receiving the first NCLT approval for the proposed commerce business demerger, with final approval expected by mid-July 2026.

Key Details

Business Performance and Strategic Initiatives:

- FY26 enrollments increased 21% YoY to approximately 2.57 lakh students.

- FY26 collections grew 40% YoY to ₹449 crore.

- Q4 FY26 collections increased 46% YoY to ₹115 crore.

- Commerce Virtuals for Classes 11 and 12 were launched, enabling pan-India digital delivery.

- Offline expansion into new geographies focused on Tier-2 and Tier-3 cities.

- New Government Test Prep programs launched, including Group II offline offerings, Junior IAS and subscription-based learning products.

- Commerce Test Prep revenue increased 70% YoY in FY26.

- Academic segment revenue increased 16% YoY in FY26.

- Government Test Prep EBITDA grew 32% YoY during FY26.

- Shareholders approved the proposed commerce business demerger through EGM resolution.

- First NCLT approval for the commerce demerger has been received.

- Management expects final NCLT approval by mid-July 2026.

Note:

- Post demerger, management is targeting 3–4x revenue growth in the commerce segment over the next 3–4 years and aims to build a ₹1,000+ crore commerce business by FY30.

Risk Analysis

Summary:

- Despite strong financial improvement, future growth depends on successful execution of expansion plans, completion of the proposed demerger, scaling of offline centers, and continued enrollment growth across key educational segments.

Key Risks:

- Final NCLT approval for the commerce demerger is still pending.

- Offline expansion into new states requires sustained execution and capital allocation.

- Education demand remains influenced by competitive intensity and student acquisition costs.

- Government Test Prep revenues may fluctuate depending on examination schedules.

- Scaling new commerce colleges and K-12 managed school initiatives carries execution risk.

- Geographic diversification into North and West India requires brand-building investments.

Worst Case Scenario:

- Delays in demerger approval, slower enrollment growth, or underperformance of new expansion initiatives could reduce revenue growth and margin improvement expectations.

Risk Level: Medium

Company Commentary

- FY26 revenue grew 35% YoY to ₹482 crore.

- Q4 FY26 revenue increased 52% YoY to ₹132 crore.

- FY26 marked the first full-year PAT-positive performance since listing.

- EBITDA margins improved significantly through disciplined cost management.

- Commerce, Government Test Prep and Academic segments continued to demonstrate healthy traction.

- The company expects completion of the commerce business demerger by mid-July 2026.

- Post demerger, management intends to pursue aggressive product and geographic expansion.

- Focus areas include faculty expansion, admissions growth, university partnerships and operational efficiency improvements.

Official Exchange Filing: Veranda Learning Solutions Limited