Quarterly & Annual Financial Results

Antony Waste Marks Silver Jubilee Year with Maiden Dividend, ₹18,000 Crore Order Book and 15% Growth in MSW Managed

NSE

awhcl

BSE

543254

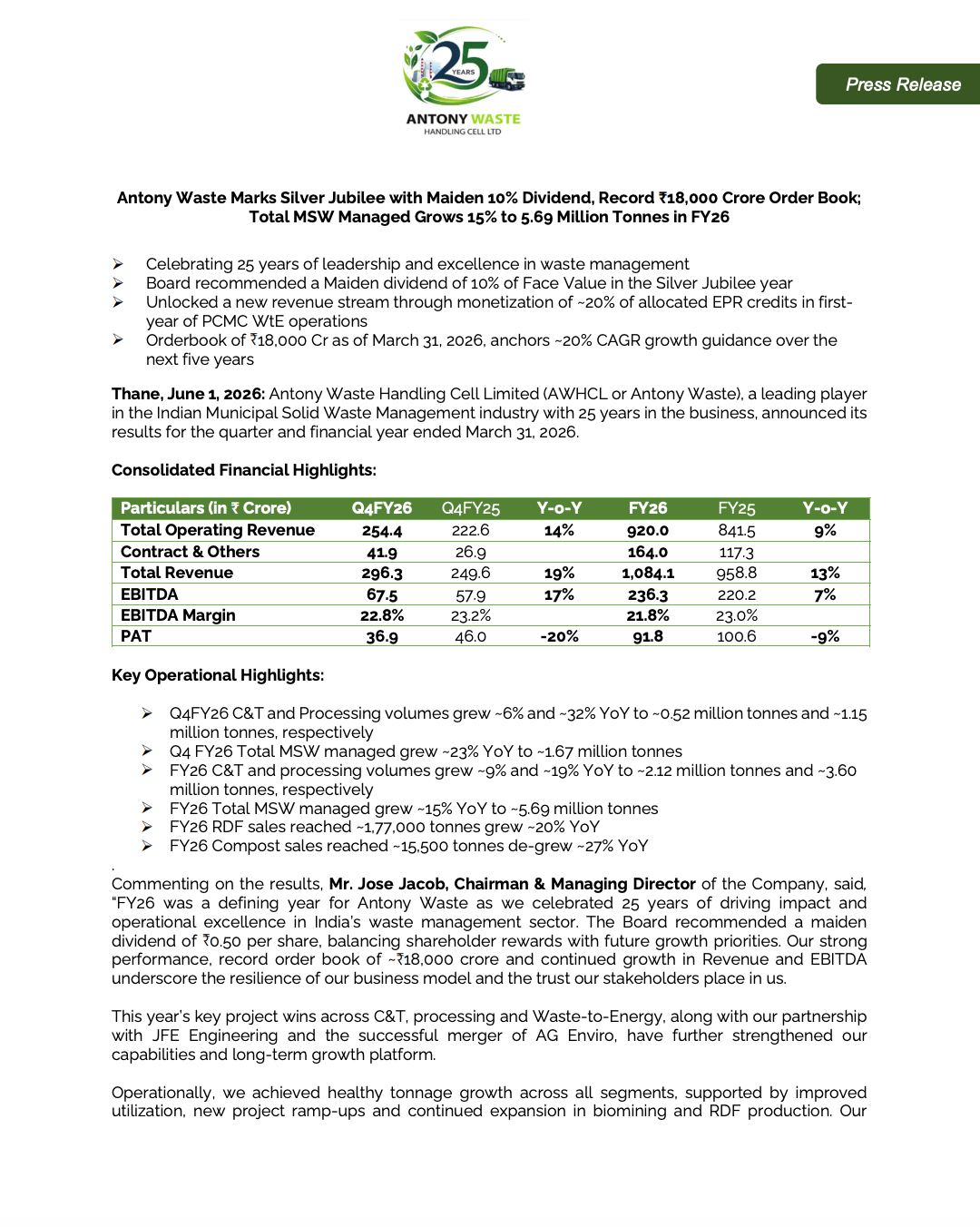

Antony Waste Handling Cell Limited reported FY26 revenue growth, healthy EBITDA expansion, and a record order book of approximately ₹18,000 crore. The company also announced its maiden dividend of 10% while total municipal solid waste (MSW) managed increased 15% YoY to 5.69 million tonnes.

PRICE-SENSITIVE TRIGGER

Event: FY26 Financial Results and Maiden Dividend Announcement

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: The company delivered revenue and EBITDA growth, declared its first-ever dividend, strengthened long-term revenue visibility through an ₹18,000 crore order book, and expanded operational volumes across waste collection, processing, RDF production and waste-to-energy operations.

Key Metrics:

- Q4 FY26 Total Operating Revenue: ₹254.4 crore (+14% YoY)

- Q4 FY26 Total Revenue: ₹296.3 crore (+19% YoY)

- Q4 FY26 EBITDA: ₹67.5 crore (+17% YoY)

- Q4 FY26 EBITDA Margin: 22.8%

- Q4 FY26 PAT: ₹36.9 crore (-20% YoY)

- FY26 Total Operating Revenue: ₹920.0 crore (+9% YoY)

- FY26 Total Revenue: ₹1,084.1 crore (+13% YoY)

- FY26 EBITDA: ₹236.3 crore (+7% YoY)

- FY26 EBITDA Margin: 21.8%

- FY26 PAT: ₹91.8 crore (-9% YoY)

Highlight:

- Antony Waste closed FY26 with a record order book of approximately ₹18,000 crore, providing strong long-term revenue visibility and supporting management’s ~20% CAGR growth outlook over the next five years.

What Happened ?

Antony Waste announced its audited FY26 financial results while celebrating its Silver Jubilee year of operations.

The company delivered growth in revenue, EBITDA and operational volumes across municipal solid waste collection, transportation, processing and waste-to-energy operations. The Board recommended a maiden dividend of 10% of face value and highlighted a record order book of approximately ₹18,000 crore.

Additionally, the company unlocked a new revenue stream through monetization of Extended Producer Responsibility (EPR) credits generated from the PCMC Waste-to-Energy project.

Key Details

Operational Growth, Order Book Expansion and New Revenue Streams:

- Maiden dividend of 10% of face value recommended by the Board.

- Record order book reached approximately ₹18,000 crore as of March 31, 2026.

- Management indicated the order book supports approximately 20% CAGR growth visibility over the next five years.

- Total MSW managed increased 15% YoY to approximately 5.69 million tonnes in FY26.

- FY26 collection & transportation volumes grew approximately 9% YoY to 2.12 million tonnes.

- FY26 processing volumes increased approximately 19% YoY to 3.60 million tonnes.

- Q4 FY26 total MSW managed rose approximately 23% YoY to 1.67 million tonnes.

- RDF sales reached approximately 1.77 lakh tonnes, up 20% YoY.

- Compost sales reached approximately 15,500 tonnes.

- New revenue stream created through monetization of around 20% allocated EPR credits during the first year of PCMC Waste-to-Energy operations.

- The company strengthened capabilities through project wins across collection & transportation, processing and waste-to-energy segments.

- Integration of AG Enviro further enhanced operational capabilities.

- Partnership with JFE Engineering continues to support waste-to-energy initiatives.

Note:

- An expanding order pipeline across waste collection, processing, RDF production, biomining and waste-to-energy projects provides long-term visibility and supports future growth plans.

Risk Analysis

Summary:

- Despite strong operational growth and a record order book, profitability remains exposed to project execution, regulatory changes, waste processing economics and waste-to-energy project ramp-up risks.

Key Risks:

- FY26 PAT declined 9% despite revenue growth, indicating margin pressure below EBITDA level.

- Q4 PAT declined 20% YoY.

- Waste-to-energy projects remain subject to operational and regulatory execution risks.

- Revenue realization depends on successful execution of large municipal contracts.

- Compost and by-product monetization can remain volatile.

- Delays in project implementation could affect order book conversion timelines.

Worst Case Scenario:

- Project execution delays, lower waste processing utilization, slower monetization of EPR credits or operational challenges in waste-to-energy facilities could reduce profitability and delay conversion of the order book into revenue.

Risk Level: Medium

Company Commentary

- Management described FY26 as a defining year coinciding with the company’s Silver Jubilee celebration.

- The Board recommended the company’s maiden dividend while maintaining focus on future growth investments.

- The company highlighted the resilience of its business model supported by revenue and EBITDA growth.

- Management emphasized the significance of the ₹18,000 crore order book and strong project pipeline.

- Growth was supported by improved utilization levels, project ramp-ups and expansion in biomining and RDF production.

- Strategic wins across collection & transportation, processing and waste-to-energy segments strengthened long-term growth prospects.

- The successful merger of AG Enviro further enhanced the company’s operational platform and capabilities.

Official Exchange Filing: Antony Waste Handling Cell Limited