Financial Results

Everest Kanto Cylinder Reports Strong FY26 Profit Growth; PAT Rises 50.1% Despite Flat Revenue

NSE

ekc

BSE

532684

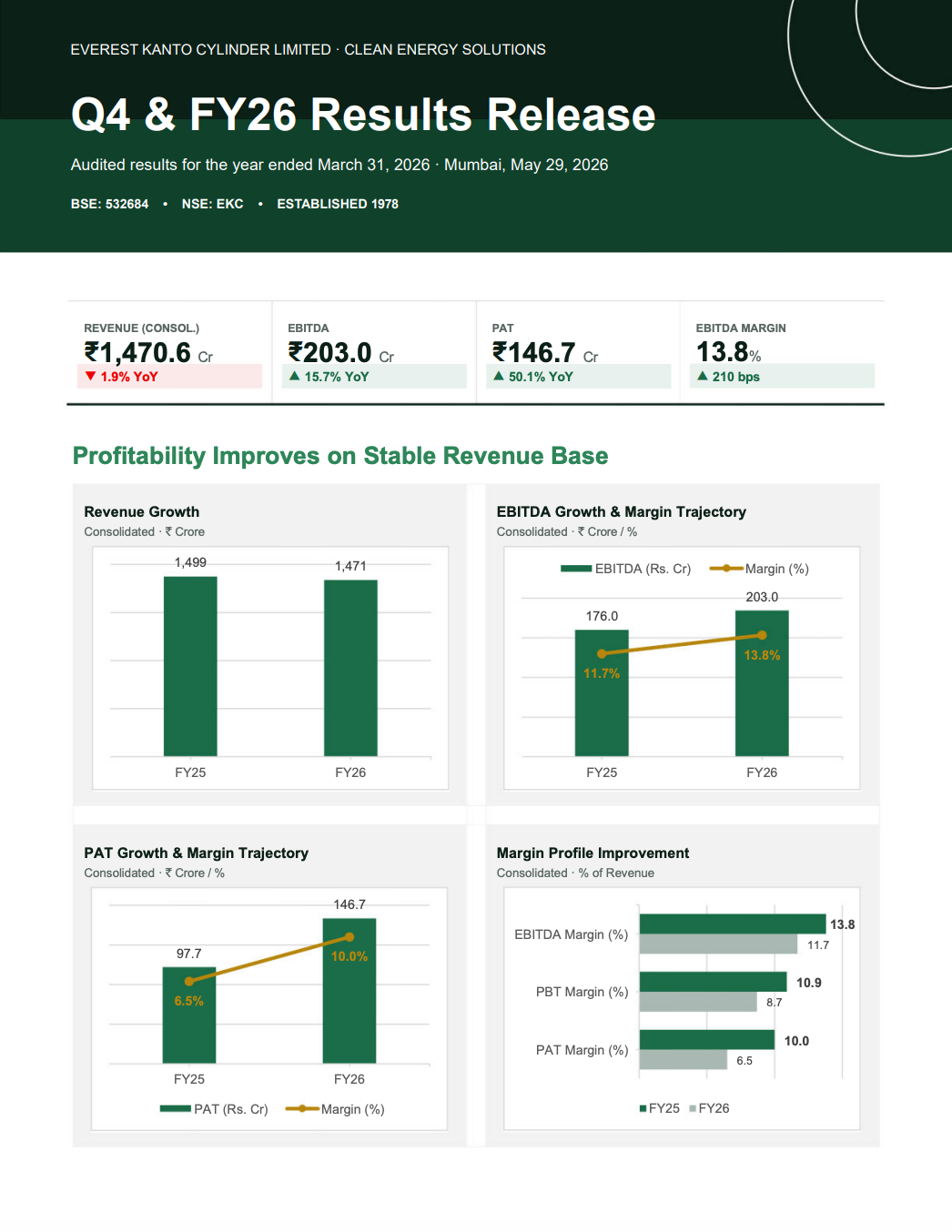

Everest Kanto Cylinder Limited (EKC) reported improved profitability in FY26 despite a marginal decline in revenue. Consolidated EBITDA grew 15.7% to ₹203.0 crore, while PAT surged 50.1% to ₹146.7 crore, driven by margin expansion, improved product mix, operational efficiencies, and growing traction in high-value segments such as semiconductors, defence, CNG infrastructure, and clean energy applications.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Audited Financial Results Announcement

Type: Financial Results

Impact: Positive

Immediate Effect: The company delivered significant improvement in profitability and margins, while continuing capacity expansion through the operationalization of the Mundra facility and progress toward commissioning its Egypt manufacturing plant.

Key Metrics:

Consolidated FY26:

- Revenue from Operations: ₹1,470.6 crore (↓1.9% YoY)

- EBITDA: ₹203.0 crore (↑15.7% YoY)

- EBITDA Margin: 13.8% (↑210 bps YoY)

- Profit Before Tax: ₹159.9 crore (↑22.6% YoY)

- PBT Margin: 10.9% (↑217 bps YoY)

- PAT: ₹146.7 crore (↑50.1% YoY)

- PAT Margin: 10.0% (↑346 bps YoY)

Consolidated Q4 FY26:

- Revenue from Operations: ₹358.2 crore (↓15.1% YoY)

- EBITDA: ₹39.6 crore (↑4.5% YoY)

- EBITDA Margin: 11.1% (↑208 bps YoY)

- PBT: ₹21.2 crore (↓17.4% YoY)

- PAT: ₹45.7 crore (↑244.4% YoY)

- PAT Margin: 12.8% (↑961 bps YoY)

Highlight:

- FY26 PAT increased 50.1% YoY to ₹146.7 crore while EBITDA margin expanded by 210 bps to 13.8%, demonstrating strong profitability improvement despite largely stable revenue.

What Happened ?

Everest Kanto Cylinder announced its audited FY26 results, reporting stable revenue and significantly improved profitability. Margin expansion across both consolidated and standalone operations was driven by operational efficiencies, improved product mix, and increasing contribution from higher-value applications.

The company also highlighted key strategic developments including commencement of operations at its new Mundra facility, progress toward commissioning its Egypt plant, and continued expansion in clean energy, industrial gas, semiconductor, defence, and CNG infrastructure segments.

Key Details

FY26 Operational and Strategic Developments:

- Mundra greenfield manufacturing facility commenced operations during FY26.

- Egypt manufacturing facility is nearing commissioning and expected to begin operations shortly.

- Board recommended a dividend of ₹0.70 per share on face value of ₹2, subject to shareholder approval.

- India operations continued witnessing healthy demand from CNG and industrial gas applications.

- US business maintained momentum supported by a healthy order pipeline.

- Semiconductor and defence sectors emerged as promising high-margin growth opportunities.

- Growing adoption of hydrogen and biogas applications is expanding clean energy opportunities.

- Continued network expansion in CNG infrastructure supported cylinder demand.

- EKC now operates:

- 6 manufacturing facilities globally

- Capacity exceeding 1.8 million cylinders annually

- More than 20 million cylinders in service

- 47 years of operating history

- Manufacturing footprint spans:

- Tarapur, India

- Kandla SEZ, India

- Mundra, India

- Jebel Ali, UAE

- Pittsburgh, USA

- Egypt (near commissioning)

Note:

- Management believes expanded manufacturing capabilities and a broader global footprint position the company to capitalize on long-term opportunities across mobility, industrial gases, and clean energy markets.

Risk Analysis

Summary:

- While profitability improved materially during FY26, revenue growth remained subdued. Future performance depends on successful commissioning of new facilities, demand sustainability in industrial and clean energy segments, and execution across international operations.

Key Risks:

- Consolidated revenue declined 1.9% YoY despite profit growth.

- Q4 revenue declined 15.1% YoY, indicating near-term volume challenges.

- Egypt facility commissioning timelines remain important for growth expectations.

- Demand in industrial gas and clean energy markets may fluctuate based on economic activity.

- Export and international operations remain exposed to global market conditions and currency movements.

- Margin expansion may moderate if input costs rise or product mix shifts unfavorably.

Worst Case Scenario:

- If industrial demand weakens and newly commissioned facilities experience slower ramp-up, revenue growth could remain muted despite expanded manufacturing capacity.

Risk Level: Medium

Company Commentary

- Management reported strong FY26 performance marked by improved profitability and margin expansion.

- Demand remained healthy across CNG and industrial gas applications in India.

- The US business continued to benefit from a robust order pipeline.

- The company is seeing increasing traction in semiconductor and defence applications.

- EKC expects enhanced manufacturing capabilities to support future growth across mobility, industrial, and clean energy sectors.

- Management believes operational excellence, innovation, and customer engagement will remain key growth drivers going forward.

Official Exchange Filing: Everest Kanto Cylinder Limited