Credit Rating Upgrade

Muthoot Microfin Receives CRISIL Rating Upgrade to AA-/Stable; Commercial Paper Rating Reaffirmed at A1+

NSE

muthootmf

BSE

544055

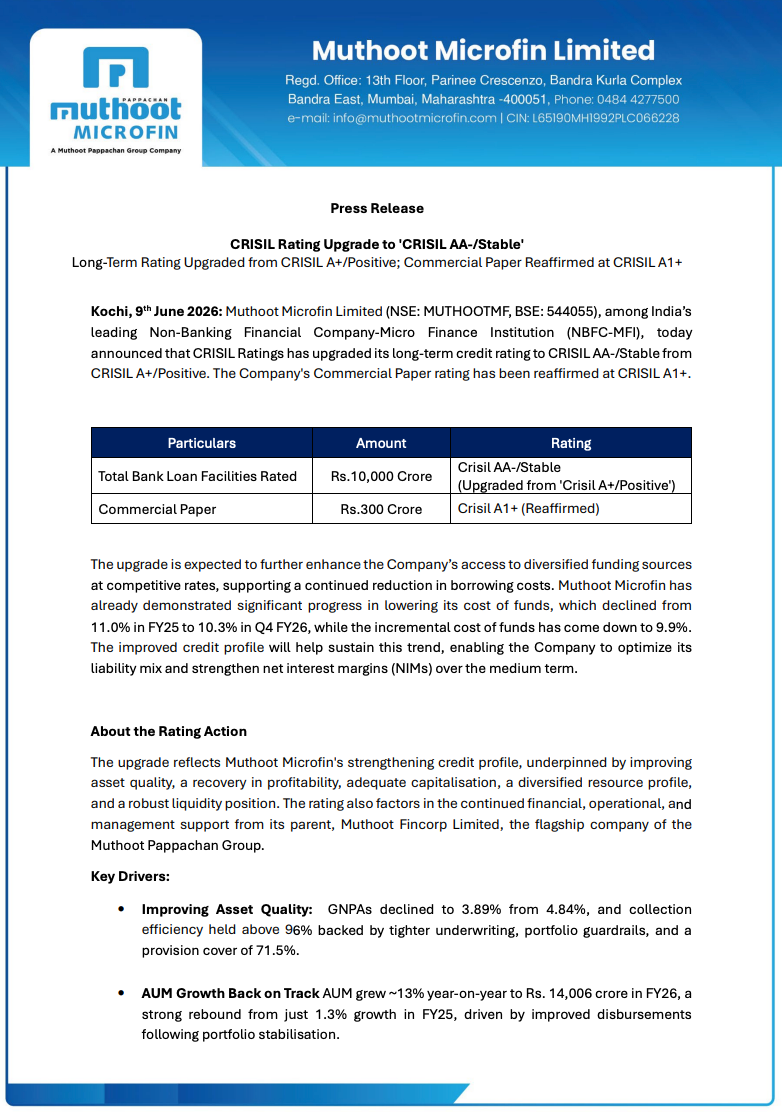

Muthoot Microfin Limited has received a credit rating upgrade from CRISIL Ratings, with its long-term bank facilities rating upgraded to CRISIL AA-/Stable from CRISIL A+/Positive. The company’s Commercial Paper rating has been reaffirmed at CRISIL A1+. The upgrade reflects improving asset quality, recovery in profitability, strong capitalization, diversified funding profile, and continued support from the Muthoot Pappachan Group.

PRICE-SENSITIVE TRIGGER

Event: CRISIL rating upgrade for long-term bank loan facilities.

Type: Credit Rating Upgrade

Impact: Positive

Immediate Effect: The upgraded rating is expected to improve funding access, reduce borrowing costs, broaden lender participation, and support margin expansion through a lower cost of funds.

Key Metrics:

- Long-Term Bank Facilities Rated: ₹10,000 crore

- New Rating: CRISIL AA-/Stable

- Previous Rating: CRISIL A+/Positive

- Commercial Paper Limit: ₹300 crore

- Commercial Paper Rating: CRISIL A1+ (Reaffirmed)

- FY26 PAT: ~₹170 crore

- FY25 PAT: Loss of ~₹222 crore

- Gross Loan Portfolio (GLP): ₹14,005.6 crore

- FY26 AUM: ~₹14,006 crore

- AUM Growth: ~13% YoY

- GNPA Ratio: 3.89%

- Previous GNPA Ratio: 4.84%

- Collection Efficiency: Above 96%

- Provision Coverage Ratio: 71.5%

- Cost of Funds (FY25): 11.0%

- Cost of Funds (Q4 FY26): 10.3%

- Incremental Cost of Funds: 9.9%

- Net Worth: ₹2,854 crore

- Capital Adequacy Ratio (CRAR): 23.9%

- Gearing Ratio: 3.3x

Highlight:

- CRISIL upgraded Muthoot Microfin’s ₹10,000 crore long-term bank facilities rating to CRISIL AA-/Stable, reflecting a significant strengthening in credit profile and profitability recovery.

What Happened ?

Muthoot Microfin announced that CRISIL Ratings has upgraded its long-term credit rating to CRISIL AA-/Stable from CRISIL A+/Positive. Simultaneously, the company’s Commercial Paper rating of ₹300 crore has been reaffirmed at CRISIL A1+.

According to the company, the rating action reflects strengthening asset quality, recovery in profitability, adequate capitalization, diversified resource profile, healthy liquidity position, and ongoing support from its parent, Muthoot Fincorp Limited.

The upgrade comes after a strong financial turnaround in FY26, during which the company reported profit recovery, improvement in portfolio quality, and continued growth in assets under management.

Key Details

Rating Upgrade & Business Performance:

- CRISIL upgraded the long-term rating from CRISIL A+/Positive to CRISIL AA-/Stable.

- Commercial Paper rating of ₹300 crore was reaffirmed at CRISIL A1+.

- FY26 profit recovered to approximately ₹170 crore from a loss of about ₹222 crore in FY25.

- Gross NPA improved to 3.89% from 4.84%.

- Collection efficiency remained above 96%.

- AUM increased approximately 13% year-on-year to ₹14,006 crore.

- Net worth stood at ₹2,854 crore as of March 31, 2026.

- Capital adequacy remained strong at 23.9%.

- Borrowing costs reduced from 11.0% in FY25 to 10.3% in Q4 FY26.

- Incremental funding cost declined further to 9.9%.

Strategic Implications:

- Improved rating expands access to diversified funding sources.

- Enhances ability to raise funds at more competitive rates.

- Supports reduction in overall borrowing costs.

- Strengthens net interest margins through lower funding expenses.

- Improves confidence among lenders, investors and institutional stakeholders.

Note:

- Management indicated that the rating upgrade supports the company’s Vision 2030 objective of achieving ₹30,000 crore AUM, generating ROA above 5%, and positively impacting 10 million households.

Risk Analysis

Summary:

- Although the rating upgrade improves funding flexibility, the microfinance sector continues to face credit cycle, collection efficiency, regulatory, and rural income-related risks.

Key Risks:

- Asset quality improvements must be sustained across economic cycles.

- Microfinance portfolios remain exposed to regional disruptions and borrower stress.

- Maintaining collection efficiency above current levels is critical.

- Competitive pressure could impact future margin expansion.

- Growth acceleration must be balanced with prudent underwriting standards.

Worst Case Scenario:

- A deterioration in collection performance or asset quality could reverse profitability gains and place pressure on future credit ratings.

Risk Level: Medium

Company Commentary

- Chairman Thomas Muthoot stated that the upgrade reflects stakeholder confidence in the company’s resilient business model, governance standards, diversification, and disciplined execution.

- Management highlighted that the company is among the few NBFC-MFIs receiving a positive rating action during the current period.

- CEO Sadaf Sayeed described the upgrade as a significant milestone reflecting operational strength, financial discipline, and consistent execution.

- The company expects the stronger rating profile to widen lender participation and improve funding competitiveness.

- Management reaffirmed its commitment toward financial inclusion, underserved women borrowers, and long-term sustainable growth.

- Vision 2030 targets include ₹30,000 crore AUM, ROA above 5%, and positive impact on 10 million households.

Official Exchange Filing: Muthoot Microfin Limited