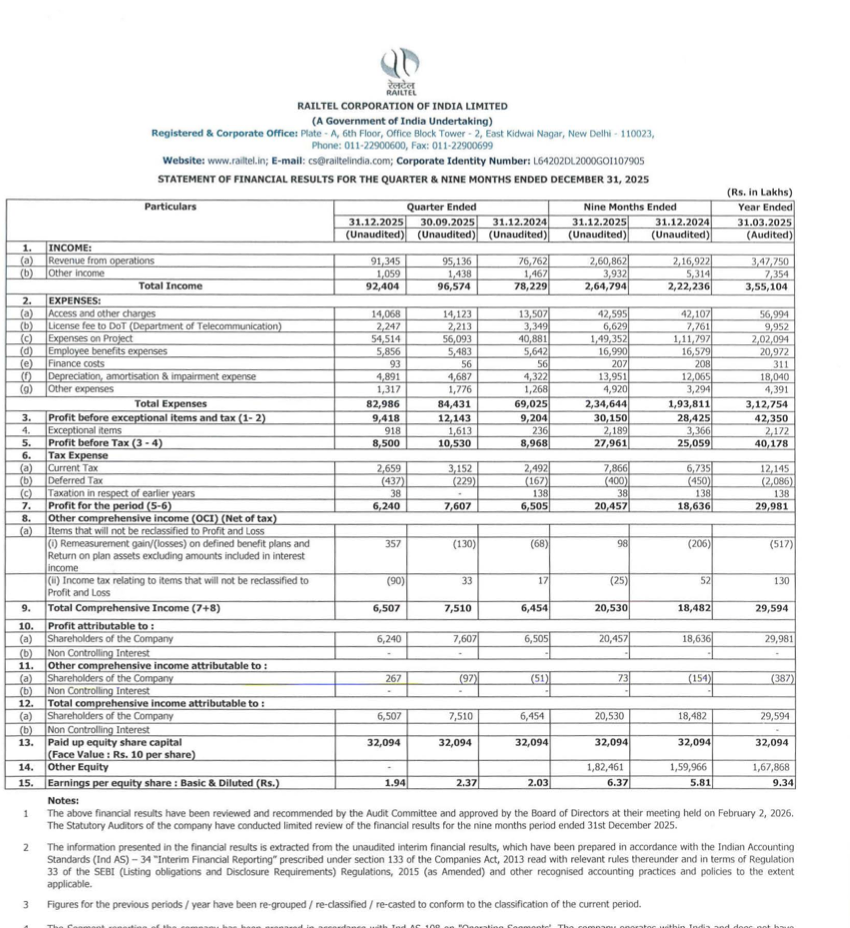

Quarter Ended: December 2025

RailTel Corporation Q3 FY26 Results Analysis

NSE

RAILTEL

BSE

543265

RailTel Corporation reported a strong revenue growth in Q3 FY26, but profitability declined, indicating margin pressure and weakening earnings quality.

key financial highlights

- Revenue from Operations: ₹91,345 lakh

- +19% YoY growth (₹76,762 lakh)

- Profit After Tax (PAT): ₹6,240 lakh

- -4% YoY decline (₹6,505 lakh)

- QoQ Performance:

- Revenue: Slight decline

- Profit: Sharp decline

Conclusion: Strong top-line, weak bottom-line

margin analysis (critical insight)

Despite revenue growth, profitability declined due to:

- Increase in project-related expenses

- Rising employee and operational costs

- Decline in operating leverage

Key Signal: Revenue growth is coming at the cost of margins

Segment-wise performance

Telecom Services

- Revenue: ₹34,954 lakh

- Higher margin, stable business

Project Work Services

- Revenue: ₹56,391 lakh

- Major contributor to growth

- Lower margin, execution-heavy

Segment insight

RailTel is shifting towards project-based revenue, which is:

- Lower margin

- Working capital intensive

- Execution dependent

Earning quality check

- Growth driven by project business

- Likely lower cash conversion

- Risk of delayed payments

Interpretation: Earnings quality appears moderate to weak

balance sheet analysis

- Total Assets: Increased to ₹5,00,521 lakh

- Total Liabilities: Also increased significantly

Indicates: Business expansion, Higher financial obligations

key risks identified

- Margin compression

- Profit decline (QoQ & YoY)

- Dependence on government projects

- Increasing cost structure

- Working capital pressure

management strategy (inferred)

- Focus on scaling revenue via projects

- Less focus on margin expansion

Company is currently in a growth phase, not efficiency phase

Financial Metrics

| Particular | In ₹ Crore | Q.O.Q (%) | Y.O.Y(%) |

|---|---|---|---|

| Total Income | 4433.90 | -14.7 | 14.8 |

| PBT | 358.89 | -61.8 | 41.2 |

| PAT | 260 | -65.1 | 32.9 |

| EPS | 0.74 | -66.2 | 32.1 |

RailTel delivered strong revenue growth, but declining margins and profits make this a weak-quality earnings quarter for investors.

Quarterly Performance Context

FISCAL YEAR

2024-2025

AUDIT STATUS

REVIEWED