Quarterly Financial Results

Manaksia Coated Metals Reports Strong Q1 FY27 Results with 162% QoQ PAT Growth and Record EBITDA per Ton

NSE

manakcoat

BSE

539046

Manaksia Coated Metals & Industries Limited reported a strong operational performance for Q1 FY27, with revenue crossing ₹263 crore, EBITDA rising nearly 86% QoQ, and PAT surging over 162% QoQ. The company also achieved its highest-ever EBITDA per ton, supported by improved realizations, higher value-added product contribution, and resilient export demand.

PRICE-SENSITIVE TRIGGER

Event: Announcement of Q1 FY27 Consolidated Financial Results.

Type: Quarterly Financial Results

Impact: Positive

Immediate Effect: Strong sequential growth in profitability and operating efficiency reflects improving execution, higher realizations, and continued momentum in value-added products despite elevated raw material costs.

Financials:

Metrics:

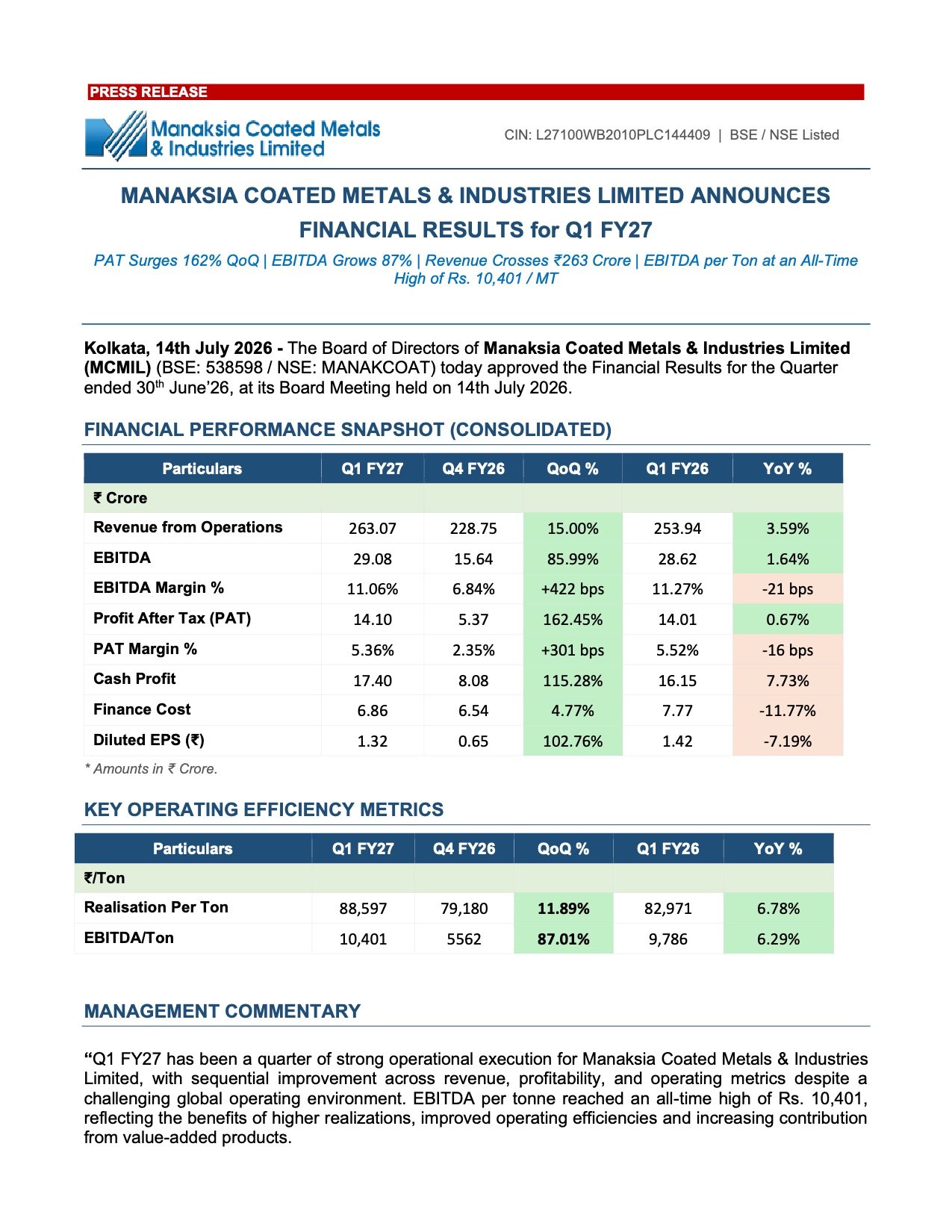

- Revenue: ₹263.07 crore (+15.00% QoQ | +3.59% YoY)

- EBITDA: ₹29.08 crore (+85.99% QoQ | +1.64% YoY)

- EBITDA Margin: 11.06% (+422 bps QoQ | -21 bps YoY)

- Profit After Tax (PAT): ₹14.10 crore (+162.45% QoQ | +0.67% YoY)

- PAT Margin: 5.36% (+301 bps QoQ | -16 bps YoY)

- Cash Profit: ₹17.40 crore (+115.28% QoQ | +7.73% YoY)

- Finance Cost: ₹6.86 crore (+4.77% QoQ | -11.77% YoY)

- Diluted EPS: ₹1.32 (+102.76% QoQ | -7.19% YoY)

- Realisation per Ton: ₹88,597 (+11.89% QoQ | +6.78% YoY)

- EBITDA per Ton: ₹10,401 (+87.01% QoQ | +6.29% YoY) — Record High

- Production – Galvanized/Alu-Zinc: 27,941 MT (+8% QoQ)

- Production – Pre-Painted Steel: 20,510 MT (+4% QoQ)

- Pre-Painted Steel Share: 74% of total sales

- Exports Contribution: 65% of total sales volume

- Export Revenue Growth: +13% QoQ | +20% YoY

- Export Sales of Pre-Painted Steel: +25% YoY

Highlight:

- EBITDA per ton reached an all-time high of ₹10,401 per MT, reflecting higher realizations, operational efficiencies, and a richer value-added product mix.

What Happened ?

Manaksia Coated Metals & Industries Limited announced its consolidated financial results for the quarter ended June 30, 2026, delivering strong sequential growth across revenue, EBITDA, and profitability.

The company benefited from improved product realizations, increasing contribution from value-added products, resilient export demand, and operational efficiencies. Despite elevated prices of aluminium, zinc, paints, freight, and fuel, the company successfully passed on most input cost increases to customers while maintaining uninterrupted production.

key details

Operational Performance and Strategic Progress:

- Revenue increased to ₹263.07 crore, supported by improved realizations and stable demand.

- EBITDA nearly doubled sequentially, while PAT increased more than 162% QoQ.

- EBITDA per ton reached a company record of ₹10,401 per MT.

- Aluminium-Zinc coating line achieved approximately 62% capacity utilisation, with customer acceptance improving in domestic and export markets.

- Export business remained strong, contributing 65% of total sales volume.

- The company expanded exports into Latvia, Brazil, Jamaica and Somalia, strengthening its international presence.

- The second colour coating line remains on track for commercialisation in Q2 FY27, increasing colour coating capacity from 86,000 TPA to 236,000 TPA.

- The 7 MW captive solar power project is progressing as planned and is expected to reduce energy costs while improving sustainability.

- Salesforce CRM implementation is underway to improve customer visibility, order tracking and demand forecasting.

Note:

- Management expects improving Alu-Zinc utilisation, commissioning of expansion projects, premiumisation, and export growth to support long-term earnings growth.

Risk Analysis

Summary:

- Although operating performance improved significantly, the company continues to face cost pressures from raw materials and global supply-chain disruptions. Future earnings will depend on successful commissioning of expansion projects, export demand, and sustained pricing power.

Key Risks:

- Aluminium, zinc and paint prices remain at multi-year highs.

- Freight and fuel costs continue to be affected by geopolitical developments.

- Commercial success depends on faster utilisation of the expanded Alu-Zinc capacity.

- Timely commissioning of the second colour coating line and solar project remains important.

- Export demand could be affected by global economic conditions.

Worst Case:

- Persistent commodity inflation, weaker export demand, or delays in strategic expansion projects could pressure margins and slow earnings growth.

Risk Level: Medium

Company Commentary

- Q1 FY27 demonstrated strong operational execution despite a challenging global environment.

- EBITDA per ton reached a record high due to better realizations, operating efficiencies and higher value-added product contribution.

- Customer acceptance for upgraded Alu-Zinc products continues to improve in both domestic and export markets.

- The second colour coating line remains on schedule for commercialisation in Q2 FY27.

- The company expects sustained growth supported by exports, premiumisation, capacity expansion and operational excellence.

Official Exchange Filing: Manaksia Coated Metals & Industries Limited