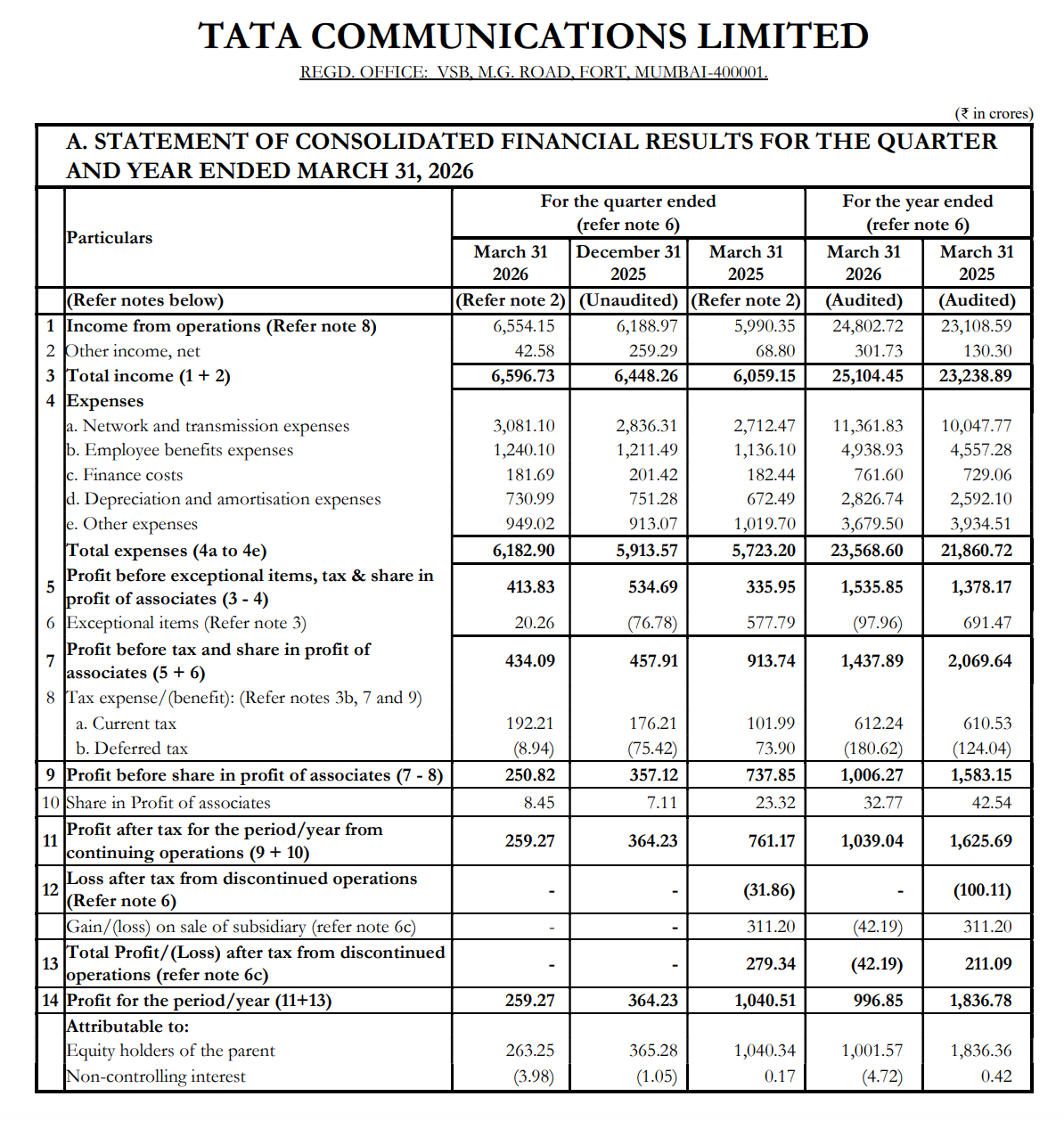

Quarter Ended: March 2026

Tata Communications Ltd – Q4 FY26 Results Analysis

NSE

tatacomm

BSE

500483

Tata Communications delivered steady revenue growth, but profitability declined sequentially due to higher costs and absence of strong exceptional gains.

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹6,596.73 Crores

- QoQ Change: +2.30%

- YoY Change: +8.87%

- Previous Quarter (Q3 FY26): ₹6,448.26 Crores

- Previous Year (Q4 FY25): ₹6,059.15 Crores

- Total Income (Q4 FY26): ₹6,596.73 Crores

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹259.27 Crores

- QoQ Change: -28.81%

- YoY Change: -75.08%

- Previous Quarter (Q3 FY26): ₹364.23 Crores

- Previous Year (Q4 FY25): ₹1,040.51 Crores

- PAT (Q4 FY26): ₹259.27 Crores

- QoQ Performance

- Revenue Trend: Stable Growth

- Profit Trend: Sharp Decline

Margin Analysis

Key Drivers:

- Increase in network & transmission costs

- Higher employee expenses

- Decline in exceptional income vs last year

Key Signal: Margins are under pressure, especially at net profit level

Segment performance

Segment: Data Services

- Revenue: ₹5,704.61 Crores

Insights:

- Core revenue driver

- Consistent growth

Segment: Voice Solutions

- Revenue: ₹387.56 Crores

Insights:

- Declining/low growth segment

- Smaller contribution

Segment: Digital / Transformation Services

- Revenue: ₹225.72 Crores

Insights:

- Emerging growth segment

- Strategic focus area

Segment insight

Tata Communications operates a digital infrastructure and data services business, with strong reliance on data services.

Characteristics:

- High share of enterprise clients

- Transition toward digital & cloud services

- Declining legacy voice business

Earning quality check

Drivers:

- Core operating revenue growth

- High cost base

- Impact of exceptional items YoY

Interpretation:

- Earnings are operational but currently under pressure due to cost structure and normalization of one-off gains

balance sheet Analysis

- Total Assets: ₹28,403.94 Crores

- Total Liabilities: ₹24,752.84 Crores

Insight:

- Leverage remains relatively high, but supported by stable operating cash flows

key risks

- High cost structure impacting margins

- Declining legacy voice segment

- Competition in data & cloud services

- Debt and financing costs

management strategy signals

- Expansion in data services

- Growth in digital & cloud segment

- Cost optimization

- Transition away from legacy voice

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹6,596.73 Crore | +2.30% | +8.87% |

| PBT | ₹434.09 Crore | -5.20% | -52.50% |

| PAT | ₹259.27 Crore | -28.81% | -75.08% |

Tata Communications continues to show steady revenue growth, but profitability is under significant pressure due to rising costs and normalization of exceptional gains

Official Exchange Filing: Tata Communications Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED