Quarterly Financial Results

Fedbank Financial Services Reports Strong Q1 FY27 Performance with 52.5% Growth in Profit After Tax

NSE

fedfina

BSE

544027

Fedbank Financial Services Limited (Fedfina) announced strong financial and operational performance for Q1 FY27, driven by robust growth in its lending business. The company reported Net Interest Income (NII) growth of 38.7% YoY, Operating Profit growth of 49.9% YoY, and Profit After Tax (PAT) growth of 52.5% YoY to ₹114.4 crore. Assets Under Management (AUM) crossed ₹21,000 crore, while asset quality improved with lower Gross and Net NPAs.

PRICE-SENSITIVE TRIGGER

Event: Announcement of financial and operational results for the quarter ended June 30, 2026 (Q1 FY27).

Type: Quarterly Financial Results

Impact: Positive

Immediate Effect: The company delivered healthy earnings growth, continued expansion in its loan book, and improved profitability while maintaining strong asset quality, reflecting sustained momentum in its secured retail lending business.

Financials:

Key Metrics:

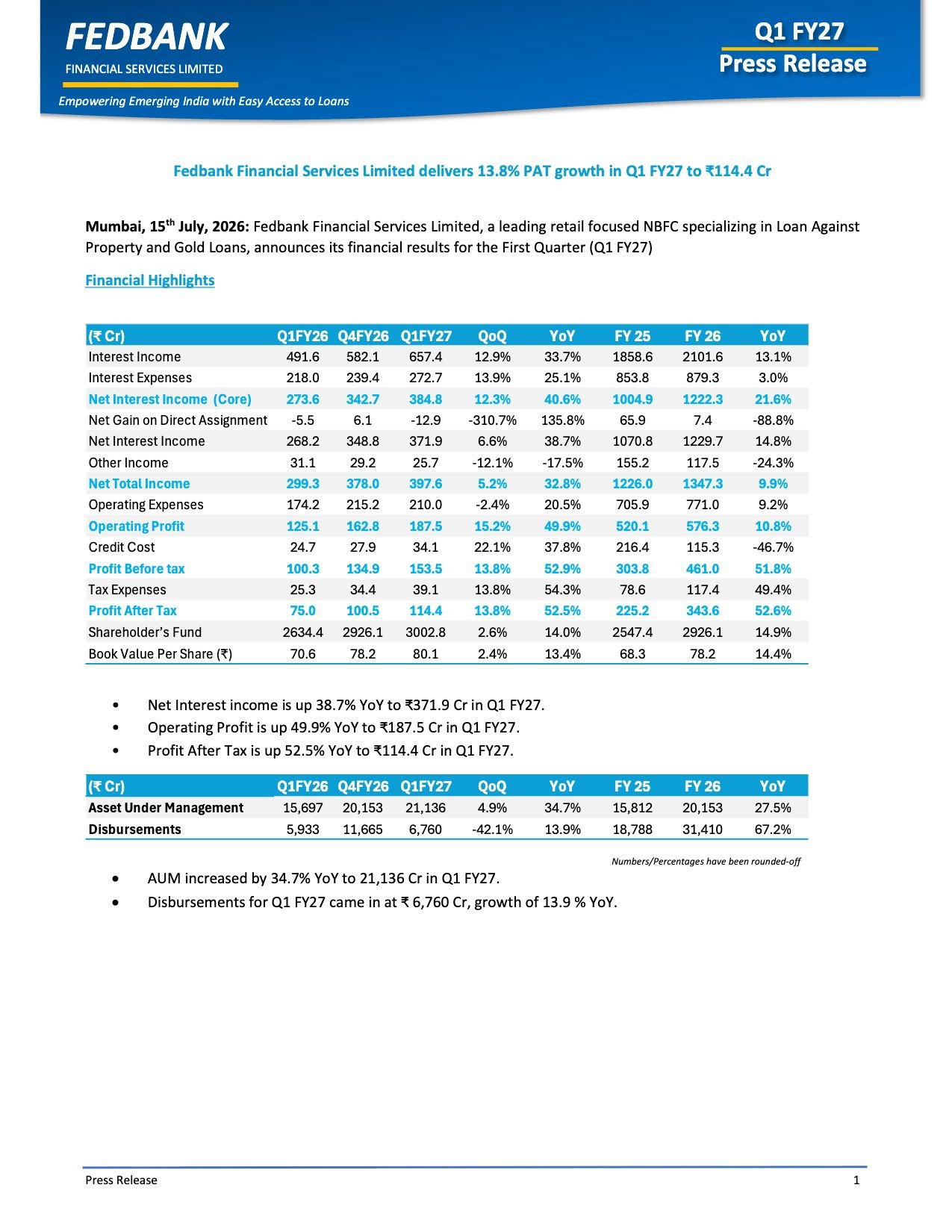

- Interest Income: ₹657.4 Cr (↑33.7% YoY)

- Interest Expense: ₹272.7 Cr (↑25.1% YoY)

- Net Interest Income (Core): ₹384.8 Cr (↑40.6% YoY)

- Net Interest Income: ₹371.9 Cr (↑38.7% YoY)

- Net Total Income: ₹397.6 Cr (↑32.8% YoY)

- Operating Profit: ₹187.5 Cr (↑49.9% YoY)

- Profit Before Tax (PBT): ₹153.5 Cr (↑52.9% YoY)

- Profit After Tax (PAT): ₹114.4 Cr (↑52.5% YoY)

- Assets Under Management (AUM): ₹21,136 Cr (↑34.7% YoY)

- Disbursements: ₹6,760 Cr (↑13.9% YoY)

- Book Value Per Share: ₹80.1 (↑13.4% YoY)

- Gross NPA: 1.6% (improved from 2.0% YoY)

- Net NPA: 1.0% (improved from 1.2% YoY)

- Return on Average Assets (ROAA): 2.6%

- Return on Average Equity (ROAE): 15.4%

- Cost-to-Income Ratio: 52.8%

Highlight:

- Profit After Tax increased 52.5% YoY to ₹114.4 crore, supported by 38.7% growth in Net Interest Income and a 34.7% increase in Assets Under Management.

What Happened ?

Fedbank Financial Services continued its strong growth trajectory during Q1 FY27, led by expansion in its core lending businesses—Loan Against Property (LAP) and Gold Loans. Higher loan growth translated into stronger Net Interest Income and operating profit, while disciplined cost management and improving asset quality supported earnings growth.

The company also maintained healthy capital levels and continued expanding its nationwide retail franchise.

key details

Strong Lending Growth:

- Assets Under Management (AUM) increased to ₹21,136 crore, registering 34.7% YoY growth.

- Quarterly disbursements reached ₹6,760 crore, up 13.9% YoY.

- Interest Income grew 33.7% YoY to ₹657.4 crore.

- Core Net Interest Income increased 40.6% YoY to ₹384.8 crore.

Note:

- Loan growth remained the primary driver of revenue expansion.

Profitability Improvement:

- Net Interest Income grew 38.7% YoY.

- Net Total Income rose 32.8% YoY.

- Operating Profit increased 49.9% YoY.

- Profit Before Tax rose 52.9% YoY.

- Profit After Tax climbed 52.5% YoY to ₹114.4 crore.

Note:

- Strong operating leverage resulted in profitability growing faster than revenue.

Asset Quality Improved:

Fedfina continued strengthening its credit profile.

- Gross NPA declined to 1.6% from 2.0% a year earlier.

- Net NPA improved to 1.0%.

- Credit Cost remained low at 0.8%.

- Gross Stage III assets improved by 32 basis points QoQ.

- Net Stage III assets improved by 31 basis points QoQ.

Note:

- Improving asset quality supports sustainable long-term earnings.

Operational Expansion:

- Branch network remained at 757 branches across 17 states and union territories.

- Employee strength increased to 5,376, representing 12.1% YoY growth.

Return Ratios:

The company reported continued improvement in profitability metrics.

- Return on Average Assets (ROAA): 2.6%

- Return on Average Equity (ROAE): 15.4%

- Cost-to-Income Ratio improved to 52.8% from 58.2% in Q1 FY26.

Risk Analysis

Summary:

- Although business growth remains strong, the NBFC sector remains sensitive to interest rate movements, funding costs, regulatory changes, and macroeconomic conditions affecting borrowers.

Key Risks:

- Rising funding costs may compress Net Interest Margins.

- Credit quality could weaken if economic conditions deteriorate.

- Regulatory changes impacting NBFCs.

- Competition within secured retail lending.

Worst Case:

- Higher credit losses or slowing loan growth could reduce profitability despite current momentum.

Risk Level: Medium

Company Commentary

- Strong growth across Net Interest Income, Operating Profit and PAT.

- Continued expansion of Assets Under Management.

- Improvement in asset quality with lower Gross and Net NPAs.

- Stable credit costs and improving operating efficiency.

- Continued focus on collateralized retail lending across India.

Official Exchange Filing: Fedbank Financial Services Limited