Quarterly Financial Results

Tatva Chintan Pharma Chem Q1 FY27 Results: Revenue Jumps 43% YoY, PAT Surges 140% as Margins Improve

NSE

tatva

BSE

543321

- Tatva Chintan Pharma Chem Limited reported a strong performance for the quarter ended June 30, 2026.

- Revenue from operations increased 43% YoY to ₹1,671 million, while EBITDA rose 86% and Profit After Tax (PAT) surged 140% year-on-year.

- The quarter was supported by improved operating leverage, better profitability, and healthy growth across the company’s specialty chemical portfolio.

PRICE-SENSITIVE TRIGGER

Event: Investor Presentation for Q1 FY27 Financial Results

Type: Quarterly Financial Results

Impact: Positive

Immediate Effect: The company delivered strong revenue growth along with significant expansion in EBITDA and PAT, reflecting improved operating efficiency and stronger profitability during the quarter.

financials:

Key Metrics:

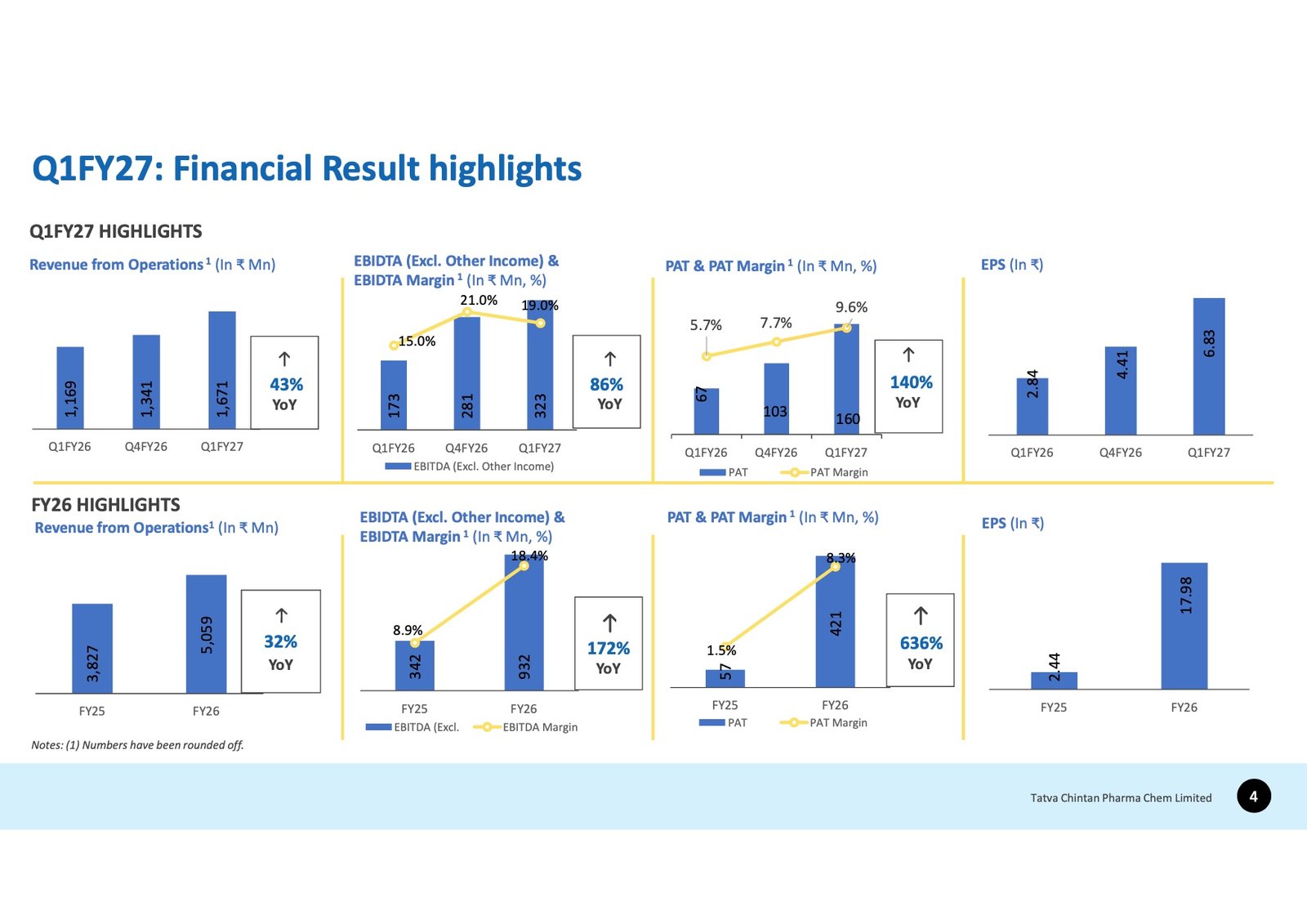

- Revenue from Operations: ₹1,671 million (+43% YoY, +25% QoQ)

- Total Income: ₹1,698 million (+44% YoY, +27% QoQ)

- EBITDA (Excluding Other Income): ₹323 million (+86% YoY, +15% QoQ)

- EBITDA Margin: 19% (vs 15% in Q1 FY26)

- Profit Before Tax (PBT): ₹211 million (+132% YoY, +27% QoQ)

- Profit After Tax (PAT): ₹160 million (+140% YoY, +55% QoQ)

- PAT Margin: 10% (vs 6% in Q1 FY26)

- EPS: ₹6.83 (vs ₹2.84 in Q1 FY26)

Highlight:

- PAT increased 140% YoY to ₹160 million, supported by a 43% rise in revenue and improved EBITDA margin of 19%.

What Happened ?

Tatva Chintan Pharma Chem reported a robust start to FY27 with strong double-digit growth across all major profitability parameters. Revenue growth was accompanied by improved operating leverage, resulting in higher EBITDA and PAT margins.

The company’s specialty chemical portfolio continued to support earnings growth, while higher operating efficiency translated into meaningful margin expansion compared with the corresponding quarter of the previous year.

key details

Quarterly Financial Performance:

- Revenue from operations grew 43% YoY to ₹1,671 million.

- EBITDA increased 86% YoY to ₹323 million.

- EBITDA margin improved to 19%, compared with 15% in Q1 FY26.

- Profit Before Tax rose 132% YoY to ₹211 million.

- Profit After Tax climbed 140% YoY to ₹160 million.

- PAT margin expanded to 10%, compared with 6% a year earlier.

- Quarterly EPS increased to ₹6.83 from ₹2.84 in Q1 FY26.

Note:

- The quarter reflects broad-based improvement in profitability alongside healthy revenue growth.

Operational Highlgihts:

- Pharma & Agrochemical Intermediates (PASC): 35% of Q1 FY27 operating revenue.

- Structure Directing Agents (SDA): 34%.

- Phase Transfer Catalysts (PTC): 26%.

- Electrolyte Salts (ESS): 4%.

- Others: 1%.

Compared with FY26, the company witnessed a relatively higher contribution from PASC while SDA’s share moderated, indicating a slight shift in revenue mix during the quarter.

Business Overview:

Tatva Chintan operates as an integrated specialty chemical manufacturer with manufacturing facilities at Ankleshwar and Dahej SEZ in Gujarat. The company serves customers across more than 25 countries and exports account for a significant share of its revenue.

Its key product categories include:

- Phase Transfer Catalysts (PTC)

- Structure Directing Agents (SDA)

- Electrolyte Salts (ESS)

- Pharma & Agrochemical Intermediates (PASC)

The company also maintains an in-house DSIR-recognized R&D facility focused on specialty chemical innovation.

Risk Analysis

Summary:

- While quarterly performance remained strong, sustaining growth will depend on demand across global specialty chemical markets, product mix, export demand, and margin stability.

Key Risks:

- Dependence on international specialty chemical demand.

- Changes in product mix may influence margins.

- Raw material cost fluctuations.

- Global economic and industrial demand uncertainty.

- Foreign exchange movements impacting export realizations.

Worst Case:

- Weak export demand or pressure on specialty chemical pricing could moderate revenue growth and profitability in future quarters.

Risk Level: Medium

Company Commentary

- Strong revenue growth supported higher profitability.

- EBITDA margin improved through better operating leverage.

- PAT more than doubled year-on-year.

- Product portfolio remained diversified across specialty chemical segments.

- Business continues to benefit from its integrated manufacturing capabilities and export presence.

Official Exchange Filing: Tatva Chintan Pharma Chem Limited