Quarterly Financial Results

Xpro India Reports Q4 FY26 Results; PAT Rises 25.2% YoY While Revenue Declines 15.1%

NSE

xproindia

BSE

590013

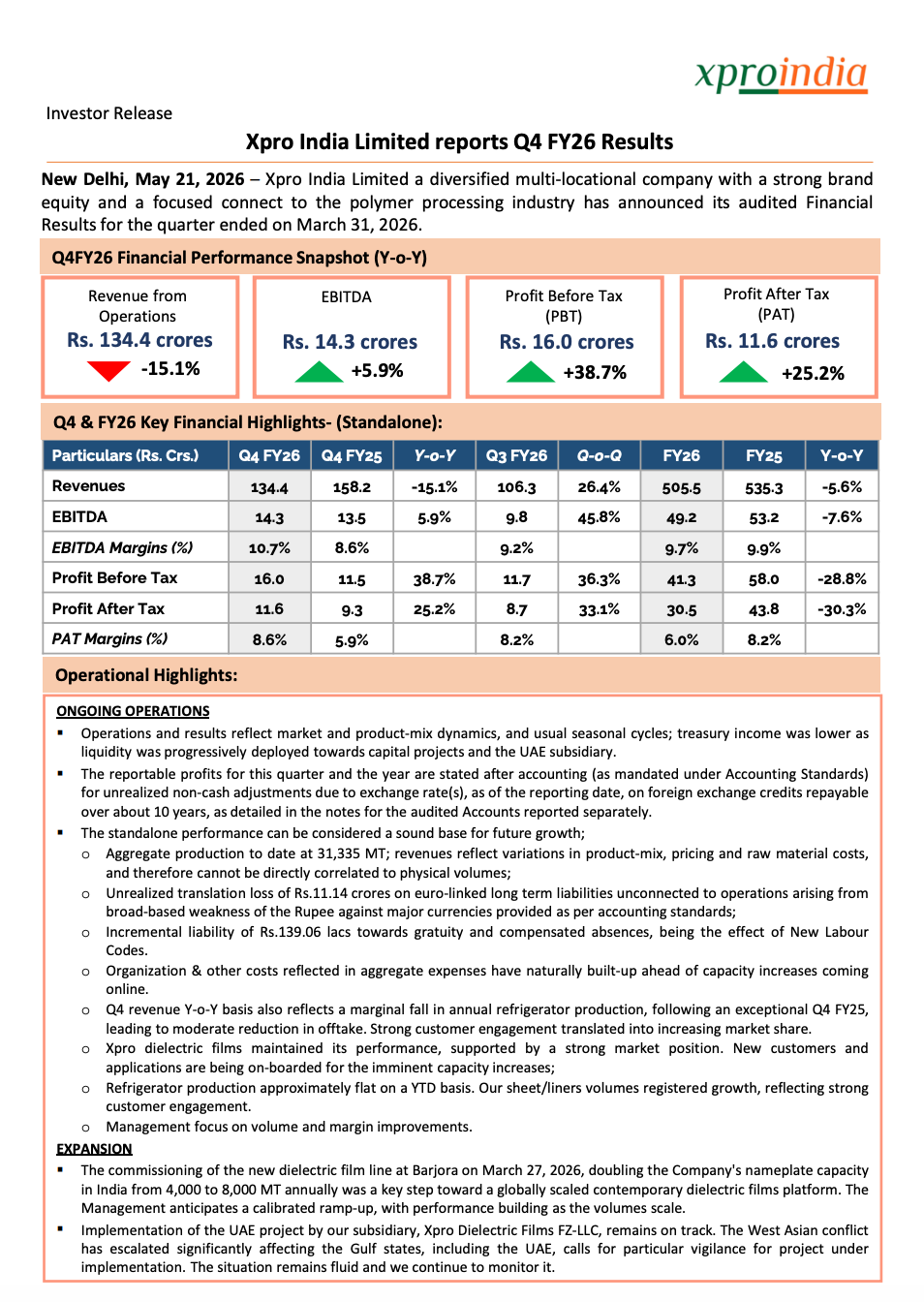

Xpro India Limited announced its audited standalone financial results for Q4 and FY26. The company reported Q4 FY26 revenue from operations of ₹134.4 crore, down 15.1% YoY, while PAT increased 25.2% YoY to ₹11.6 crore. EBITDA rose 5.9% YoY to ₹14.3 crore with EBITDA margin improving to 10.7%.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 Audited Financial Results Announcement

Type: Quarterly Financial Results

Impact: Neutral

Immediate Effect: The company reported improved profitability and margins despite lower revenues, supported by operational efficiencies, better product mix, and strong dielectric films business performance.

Key Metrics:

- Q4 FY26 Revenue: ₹134.4 Crore

- Q4 FY25 Revenue: ₹158.2 Crore

- Revenue YoY Change: -15.1%

- FY26 Revenue: ₹505.5 Crore

- FY25 Revenue: ₹535.3 Crore

- FY26 Revenue YoY Change: -5.6%

- Q4 FY26 EBITDA: ₹14.3 Crore

- Q4 FY25 EBITDA: ₹13.5 Crore

- EBITDA YoY Growth: 5.9%

- FY26 EBITDA: ₹49.2 Crore

- FY25 EBITDA: ₹53.2 Crore

- FY26 EBITDA Margin: 9.7%

- Q4 FY26 EBITDA Margin: 10.7%

- Q4 FY26 PBT: ₹16.0 Crore

- Q4 FY25 PBT: ₹11.5 Crore

- PBT YoY Growth: 38.7%

- Q4 FY26 PAT: ₹11.6 Crore

- Q4 FY25 PAT: ₹9.3 Crore

- PAT YoY Growth: 25.2%

- FY26 PAT: ₹30.5 Crore

- FY25 PAT: ₹43.8 Crore

- FY26 PAT YoY Change: -30.3%

- Q4 FY26 PAT Margin: 8.6%

- Q4 FY25 PAT Margin: 5.9%

- FY26 PAT Margin: 6.0%

- FY25 PAT Margin: 8.2%

- FY26 RoCE: 5.7%

- FY25 RoCE: 9.3%

- FY26 RoE: 4.6%

- FY25 RoE: 7.4%

- FY26 Net Debt to Equity: -0.08x

- FY26 Equity Base: ₹715.5 Crore

- FY25 Equity Base: ₹616.9 Crore

Highlight Metric:

- Q4 FY26 PAT grew 25.2% YoY to ₹11.6 crore while EBITDA margin improved sharply to 10.7%.

What Happened ?

Xpro India Limited announced its audited standalone Q4 and FY26 financial results.

For Q4 FY26:

- Revenue declined 15.1% YoY to ₹134.4 crore.

- EBITDA increased 5.9% YoY to ₹14.3 crore.

- Profit Before Tax (PBT) rose 38.7% YoY to ₹16 crore.

- Profit After Tax (PAT) increased 25.2% YoY to ₹11.6 crore.

- EBITDA margin improved to 10.7% from 8.6% last year.

- PAT margin improved to 8.6% from 5.9%.

For FY26:

- Revenue declined 5.6% YoY to ₹505.5 crore.

- EBITDA declined 7.6% YoY to ₹49.2 crore.

- PAT declined 30.3% YoY to ₹30.5 crore.

- Return on Capital Employed (RoCE) reduced to 5.7%.

- Return on Equity (RoE) declined to 4.6%.

The company stated that performance was influenced by product mix dynamics, treasury deployment toward capital projects, unrealized forex translation losses, and costs related to upcoming capacity expansions.

Xpro also highlighted strong traction in its dielectric films business and commissioning of the new dielectric film line at Barjora, which doubled annual capacity from 4,000 MT to 8,000 MT.

Key Details

Operational Performance & Expansion Highlights:

- Aggregate production till date:

- 31,335 MT.

- Q4 revenue decline was partly due to:

- Lower refrigerator production after an exceptional FY25 quarter.

- Dielectric films business:

- Maintained strong performance and customer onboarding.

- New dielectric film line:

- Commissioned at Barjora on March 27, 2026.

- Dielectric films capacity expansion:

- Increased from 4,000 MT annually to 8,000 MT annually.

- Management expects:

- Gradual ramp-up and performance scaling from new capacities.

- Refrigerator production:

- Approximately flat on YTD basis.

- Sheet/liners volumes:

- Registered growth due to strong customer engagement.

- Treasury deployment:

- Liquidity progressively deployed toward:

- Capital projects.

- UAE subsidiary expansion.

- Liquidity progressively deployed toward:

- Additional cost impacts:

- Unrealized forex translation losses.

- Gratuity and employee compensation provisions.

- Organizational costs linked to capacity expansion.

- UAE project:

- Remains on track despite geopolitical risks in the Gulf region.

- Company focus:

- Volume growth.

- Margin improvement.

- Capacity utilization optimization.

Note:

- Management highlighted that current standalone performance should form the base for future growth as new capacities begin scaling and customer onboarding improves across dielectric films and polymer processing businesses.

Risk Analysis

Summary:

- Although margins improved during Q4, the company remains exposed to demand cyclicality, forex fluctuations, raw material volatility, and risks related to capacity expansion ramp-up.

Key Risks:

- Revenue decline indicates ongoing demand and product-mix pressure.

- PAT for FY26 declined significantly despite operational improvements.

- Unrealized forex losses affected profitability.

- Raw material price volatility may impact margins.

- UAE expansion project faces geopolitical uncertainty.

- New capacity utilization ramp-up may take longer than expected.

- Refrigeration industry demand softness could impact future growth.

- Rising employee and organizational costs may pressure earnings.

Worst Case Scenario:

- If demand recovery remains weak and newly commissioned capacities fail to scale efficiently, profitability and return ratios may remain under pressure over the medium term.

Risk Level: Medium

Company Commentary

- Management stated that operational performance reflects market and product-mix dynamics along with seasonal trends.

- The company highlighted strong customer engagement in dielectric films and sheet/liners businesses.

- Xpro India stated that the Barjora dielectric film expansion is a major long-term growth driver.

- Management emphasized focus on volume growth and margin improvement.

- The company confirmed that the UAE project implementation remains on track despite geopolitical developments.

- Management reiterated confidence in future scaling opportunities through ongoing capacity additions.

Official Exchange Filing: Xpro India Limited