Quarterly Financial Results

JSW Steel Q1 FY27 Results: Revenue Rises 19% YoY, EBITDA Crosses ₹9,300 Crore on Strong Domestic Operations

NSE

jswsteel

BSE

500228

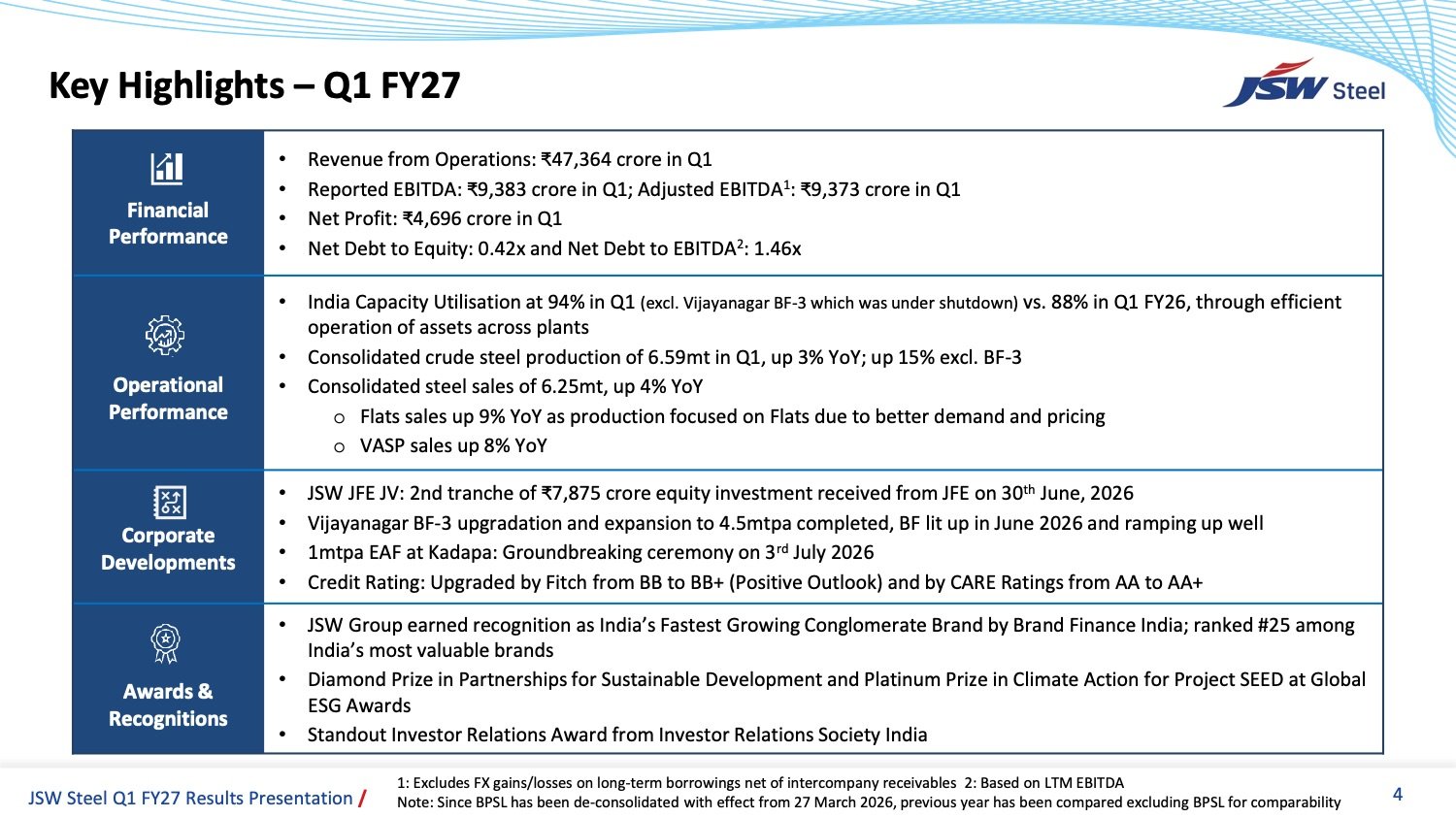

- JSW Steel reported a strong start to FY27 with consolidated revenue from operations of ₹47,364 crore and net profit of ₹4,696 crore.

- Higher steel realizations, improved sales volumes, robust Indian operations, and better performance from international businesses supported earnings during the quarter.

- The company also completed key capacity expansion projects and maintained healthy leverage metrics.

PRICE-SENSITIVE TRIGGER

Event: JSW Steel announced its financial results for the first quarter ended June 30, 2026 (Q1 FY27).

Type: Quarterly Financial Results

Impact: Positive

Immediate Effect: The company delivered higher revenue, EBITDA and net profit on a year-on-year basis while improving capacity utilization and maintaining a healthy balance sheet, reflecting continued operational strength.

financials:

Key Metrics:

- Revenue from Operations: ₹47,364 crore

- Reported EBITDA: ₹9,383 crore

- Adjusted EBITDA: ₹9,373 crore

- Profit Before Tax: ₹6,160 crore

- Profit After Tax (PAT): ₹4,696 crore

- Diluted EPS: ₹19.02

- Net Debt to Equity: 0.42x

- Net Debt to EBITDA: 1.46x

- Consolidated Crude Steel Production: 6.59 million tonnes

- Consolidated Steel Sales: 6.25 million tonnes

Financial Performance Highlights:

- Revenue from operations increased approximately 19% YoY, supported by stronger steel realizations and higher sales volumes.

- Reported EBITDA improved to ₹9,383 crore, reflecting better operating leverage.

- Profit after tax more than doubled year-on-year to ₹4,696 crore.

- Finance costs declined due to lower debt levels and reduced borrowing costs.

- Lower effective tax rate further supported profitability during the quarter.

Highlight:

- Strong operating profitability remained the key driver of earnings during Q1 FY27.

What Happened ?

JSW Steel delivered a strong operational and financial performance during Q1 FY27 despite the temporary shutdown of Blast Furnace-3 at Vijayanagar during part of the quarter.

Higher domestic steel prices, better product mix, improved capacity utilization and higher sales volumes helped the company report significant growth in revenue and profitability. International operations also contributed positively as both the US and Italy businesses recorded better EBITDA performance compared to earlier periods.

The company continued executing its long-term expansion strategy, including the commissioning of the upgraded Vijayanagar blast furnace and commencement of development work for its Kadapa electric arc furnace project.

key details

Financial Performance:

- Consolidated revenue reached ₹47,364 crore, driven by higher steel realizations and increased sales volumes.

- Reported EBITDA stood at ₹9,383 crore, while adjusted EBITDA remained at ₹9,373 crore.

- Profit after tax increased to ₹4,696 crore, reflecting improved operating margins and lower finance costs.

- Profit before tax rose to ₹6,160 crore.

- Interest expenses declined as the company benefited from lower debt and reduced borrowing costs.

- Tax expenses remained lower due to a favorable tax profile at JSW Vijayanagar Metallics Limited.

Note:

- Financial performance reflects stronger realizations, disciplined cost management and improved operating efficiency across major businesses.

Operational Performance:

- Consolidated crude steel production increased to 6.59 million tonnes, up 3% YoY.

- Consolidated steel sales rose to 6.25 million tonnes, up 4% YoY.

- Indian operations achieved 94% capacity utilization, excluding the temporarily shut Vijayanagar BF-3.

- Flat steel sales increased 9% YoY, supported by better market demand.

- Value-added and special products (VASP) sales grew 8% YoY.

- Indian operations remained the primary contributor to overall earnings during the quarter.

Note:

- Higher utilization levels and a stronger product mix helped offset the temporary impact of planned maintenance activities during the quarter.

Capacity Expansion & Growth Projects:

- The company commissioned the upgraded Blast Furnace-3 at Vijayanagar, increasing annual crude steel capacity.

- Development work continued on the Kadapa Integrated Steel Plant, which will be based on Electric Arc Furnace (EAF) technology.

- Expansion projects remain aligned with JSW Steel’s long-term strategy to increase domestic production capacity while improving operating efficiency.

- Ongoing investments are focused on strengthening downstream capabilities and supporting future demand growth.

- Capacity additions are expected to improve product mix, operational flexibility and long-term earnings potential.

Note:

- Capacity expansion remains one of the company’s primary long-term growth drivers and is expected to support higher production volumes over the coming years.

International Operations:

- JSW Steel USA (Ohio) reported improved EBITDA during the quarter.

- Piombino Steel, Italy also delivered better operating performance.

- International businesses benefited from improved operational efficiencies and better market conditions.

- Overseas operations continued contributing positively to consolidated profitability.

Note:

- Improved international performance provided additional support to consolidated earnings alongside strong domestic operations.

Balance Sheet & Cash Flow:

- Net Debt to Equity remained healthy at 0.42x.

- Net Debt to EBITDA stood at 1.46x, reflecting a comfortable leverage profile.

- Lower borrowing costs contributed to reduced finance expenses.

- Strong operating cash generation supported ongoing capital expenditure and expansion projects.

- The company maintained financial flexibility while continuing its growth investments.

Note:

- Healthy leverage metrics provide adequate financial capacity to execute the company’s expansion roadmap.

Risk Analysis

Summary:

- While Q1 FY27 performance remained strong, the steel industry continues to face risks from raw material prices, global demand fluctuations, import competition and macroeconomic uncertainties. Execution risks related to expansion projects also remain relevant.

Key Risks:

- Volatility in coking coal and iron ore prices.

- Global steel demand and pricing uncertainties.

- Import pressure from low-cost steel producers.

- Delays in commissioning or ramp-up of expansion projects.

- Changes in government policies affecting the steel sector.

- Currency fluctuations impacting international operations.

Worst Case:

- A prolonged decline in steel prices combined with rising raw material costs could compress margins and delay earnings growth despite higher production capacity.

Risk Level: Medium

Company Commentary

- Management highlighted that Q1 FY27 performance was supported by higher realizations, improved product mix and strong operational execution.

- The company remains focused on expanding steelmaking capacity while maintaining capital discipline.

- Ongoing investments in Vijayanagar and Kadapa are expected to strengthen long-term growth.

- Management reiterated its commitment to operational excellence, cost optimization and sustainable value creation for shareholders.

- International businesses are expected to continue improving operational performance.

Official Exchange Filing: JSW Steel Limited